Profit-rate cut of govt savings tools to yield mixed results

FE Report | Tuesday, 12 May 2015

The decision taken by the government to cut yield rates of its savings instruments will help lower the cost of doing business.

But the move will hurt the interests of small savers, pension holders and insolvent families.

An unprecedented surge in the sales of the instruments in recent months, according to sources, has also forced the government to review the rates of profit.

Finance Minister AMA Muhith announced Sunday that the government has decided to cut the rate of profits allowed against all types of saving certificates by one to two per cent. Many newspapers carried reports in their Monday's issues that rate of profit in the case of five-year Bangladesh Savings Certificate had been reduced to 11.26 from 13.19 percent. But no circular was issued in this regard until Monday.

When contacted, officials concerned at the Ministry of Finance, Internal Resources Division (IRD) and Directorate of National Savings (DNS) expressed their ignorance about the rate-cut decision.

Officials at the DNS informed the FE that they had already sent a proposal for reduction of profit rates on all types of savings tools and bonds. But no decision has arrived as yet, they said.

However, bankers, businesses, and economists have welcomed the government decision to cut yield rates of national saving certificates (NSCs) as higher yield rates, according to them, are creating obstacles to the private sector investment growth.

On the other hand, the people who are dependent on the profits coming from the same have an altogether different feeling. They said the decision to cut rate of profits if enforced will affect the life and living of limited-income people and elderly citizens, especially the pension holders.

Many of the NSC holders argued that reduction in the rates of profit will affect the interests of elderly people and the womenfolk, the majority investors in the NSCs.

Some of them said although the government has decided to reduce the yield rates of savings instruments, it has not made any announcement regarding the enhancement of the investment ceiling for the savers.

According to them, the government should raise the existing ceilings for individual investment in the NSCs as the proposed cut in the yield rates will reduce the earnings of the investors.

When contracted, a DNS official said the government has no immediate plan to raise the exiting investment ceilings.

Mentioning that presently, retired private sector employees and executives are not allowed to invest in the pensioners' savings instrument, some experts and investors pleaded for a change in the existing rules.

The government's decision to cut the yield rates of savings tools came in the wake of a surge in the government's borrowing from the source, pushing up its debt-sevicing liability, officials said.

However, the increased volume of borrowing from the savings tools helped the government to borrow less from the banking system, they mentioned.

Economists are in favour of reducing the rate of yield on saving instruments.

They are of the opinion that the existing large difference between the bank-deposit rates and the NSC yields, on the one hand, has been creating distortions in the interest rate regime in the financial sector and, on the other the public exchequer is being burdened with the payments of a substantial amount on account of profit.

Policy Research Institute Chairman Dr. Zaidi Sattar termed it an attractive mode of investment and urged the government for concentrating more on foreign aid and soft loans as the high yield bearing instruments would increase government liabilities.

"There is a competition between the yield rates and bank deposit rates. Banks cannot reduce high rates on deposits because of high rates of profit offered against saving instruments, the PRI chairman told the FE-PRI Economic Analysis Unit. He, however, said that the decision to reduce the yield rates might help reduce the deposit rates, augment private investment and spur the capital market.

According to bankers, if a retired person invests Tk 100,000 in a national saving certificate, he/she gets nearly Tk 1100 a month. On the other hand, the return will be far less from his time deposit with any commercial bank. For the big difference in yields, people prefer to invest in the NSCs.

Bankers also welcomed the decision as the high yield on NSCs very often attracts most of their clients. "There are no other saving instruments like NSCs that offer such high yield," said ABB (Association of Bankers, Bangladesh) president Ali Reza Iftekhar while talking to The Financial Express. Sales of savings certificates soared high mainly due to higher interest rates on the savings instruments and the government had to pay higher interest on such savings, also said the banker.

"It would be better if the decision was implemented earlier," said Iftekhar, also Managing Director and CEO of Eastern Bank Ltd. The banks, Iftekhar said, has already reduced the interest rate substantially. According to Iftekhar, the banks interest rate now rages between 5-6 per cent in case of savings and 8-9 per cent in case of fixed deposits. "The rate can be reduced a little bit further," said Iftekhar when asked about reducing interest rate. "But all these, you know, are market driven," he added.

Metropolitan Chamber of Commerce and Industry, Dhaka (MCCI) president Syed Manzur Elahi also welcomed the decision adding that it would reduce their cost of doing business.

"We have been making this demand for long," said Manzur adding that the government now should think how to cut the rate of interest on bank loans from double digit to single one and make Bangladesh products competitive in the world market.

Bangladesh Bank's chief economist Biru Paksha Paul, at a seminar very recently also urged the government to reduce the yield as the savings scheme, he said, is no longer benefiting the intended low-income groups-instead rich people are reaping a windfall from these instruments.

"We know that pensioners, senior citizens and widows invest in savings certificates. But its high interest is now luring millionaires and diverting funds from the stock market as well," he said at the seminar, organised by the Board of Investment.

According to Centre for Policy Dialogue (CPD) Additional Director Dr Khandker Moazzem Hossain the adjustment was essential to strike a balance between various financial instruments. "The bank-deposit, NSC yields and the stock market are interlinked where the high yield of NSCs was creating a sort imbalance," said Moazzem terming the decision quite justified.

He said that the decision would help government to reduce its debt liabilities. But it may not do much in reducing bank interest where there is lot of limitations. He, however, said that it would help largely the business community to have credit facilities at low cost.

The Directorate of National Savings (DNS) has six types of savings instruments offering up to 13.45 per cent interest while returns on bank deposits now stand below 10 per cent. There are four bonds also in operation under the DNS.

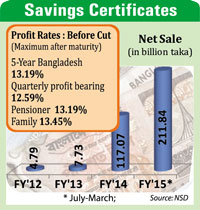

The interests on five-year family savings certificates is 13.45 per cent, pensioners certificate 13.19 per cent, Bangladesh Savings Certificate 13.19 per cent, three-year savings certificates with tri-monthly returns 12.59 per cent, postal savings and bank certificates' 13.24 per cent.

Some 25.0 million (2.50 crore) people had invested in government savings instruments since independence, according to the official figures, officials said.

Around 17,459 investors bought savings certificates though banking channel during the January-March period of the current fiscal,

However, the net sales of savings tools stood at Tk 211.84 billion during the July-March period of FY 2014-15 whereas it was Tk 74.60 billion in the corresponding period of last FY.

During the 9-month period of FY 2014-15, the government paid Tk 70.51 billion as profit compared to that of Tk 56.55 billion paid during the same period of the last fiscal, Department of National Savings (DNS) data showed.

Because of the surge in demand for the savings tools, the government has revised the target of savings tools sales to Tk 210.00 billion from the original target of Tk 90.56 billion in the current fiscal year.

The revised target of paying profit against the borrowing through the savings certificates has also been set at Tk 98.77 billion for the entire FY 2014-15.

Meanwhile, the sales of savings instruments have come down substantially Monday in various banks, and in some cases, bank authorities stopped the sale of certificates due to confusion relating to yield rate cut. When contacted an official of Agrani Bank also expressed his ignorance regarding the decision.

Bankers and business community have been demanding a cut in the yield rate of savings instruments for a long as the high yield is diverting funds from banks as well as stock markets. The finance minister also agreed to reduce the yield rate several times, but could not implement his decision as a section of policymakers have been opposing the move.

According to sources, the existing difference between the bank-deposit and NSC yields was distorting the interest regime in the financial sector and making the public exchequer with huge burden of interest payments

Although the Finance Minister earlier pledged introduction of a national pension scheme as per the election manifesto of his government, no visible progress has yet been noticed in this regard.

Speaking at a programme at the National Economic Council (NEC) in April last year, Muhith said the organised private sector would be covered under the pension schemes in future alongside the existing national pension scheme.

There are some 2.0 million government officials and employees under the national pension scheme and if it is implemented at the organised private sector, then the number would rise to 5.0 million, he mentioned.

mzrbd@yahoo.com, arafat_ara@hotmail.com