Quandary on public finance management

Fahmida Khatun, Mustafizur Rahman, Khondaker Golam Moazzem, Towfiqul Islam Khan, Muntaseer Kamal, and Syed Yusuf Saadat | Wednesday, 5 June 2024

Commenting on the country’ public finance situation has become problematic due to the unavailability of timely data. As of May 2024, the Ministry of Finance (MoF) data is available only until January 2024. As is known, the MoF provides the most comprehensive and better-quality data concerning public finance in Bangladesh. Although alternative and more timely sources such as the National Board of Revenue (NBR), Implementation Monitoring and Evaluation Division (IMED), and Bangladesh Bank can be utilised, their data is fragmented and often lacks accuracy and congruency. The present analyses utilise all these sources but might be constrained in some cases due to data limitations.

REVENUE MOBILISATION: According to MoF data, total revenue collection recorded a 13.3 per cent growth during the July-January period of FY2024. This is a considerable improvement from the corresponding figure of FY2023 (-2.0 per cent). Despite this, a whopping 63.2 per cent growth will be required during the remainder of FY2024 if the annual target is to be achieved – a highly unlikely prospect. The total revenue growth during July-January FY2024 was primarily driven by improved performances in income tax and VAT collection as well as by significant increases in government earnings from dividends and profit.

As per NBR data, tax collection by NBR grew by 15.6 per cent during the July-April period of FY2024. This is a significant increase from the corresponding figure for July-April FY2023, which stood at 7.1 per cent. The growth achieved in the ongoing FY2024 was driven primarily by the collection of VAT and supplementary duty (SD) at the local level and income tax. Perhaps the persistently high price level in the economy is driving the improvement of VAT and SD collection at the local level. On the other hand, the underwhelming performance of indirect taxes collected at the import level, despite the substantial depreciation of the Bangladeshi Taka, can be attributed to the import-related restrictions imposed through government regulatory measures. Given these dynamics, whether the revenue-related conditionalities set by the International Monetary Fund (IMF) can be met remains a critical question.

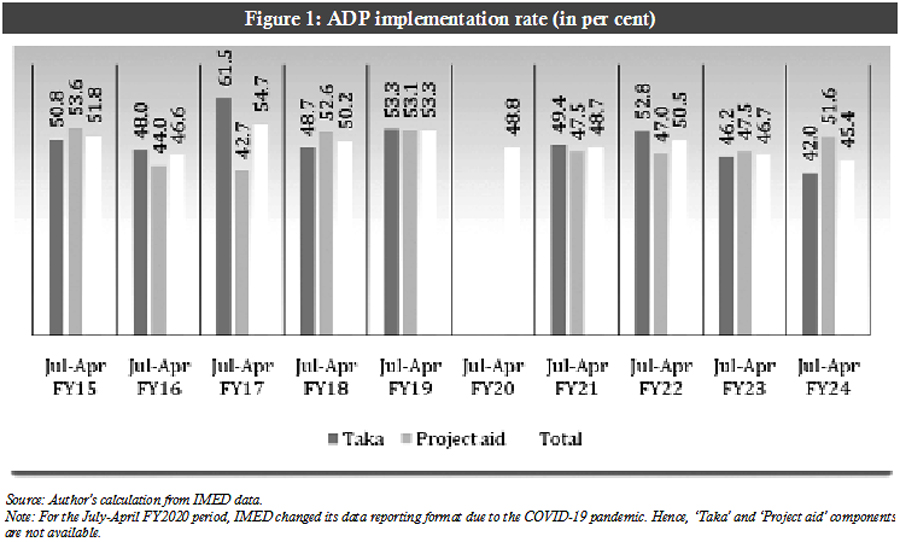

PUBLIC EXPENDITURE: In general, a restrained approach in terms of public expenditure was observed during the first seven months of FY2024. As MoF data shows, overall budget utilisation was 32.4 per cent during July-January of FY2024. The corresponding figure for FY2023 was also the same. The Annual Development Programme (ADP) implementation rate was on the lower side – with 20.0 per cent of the allocated amount spent during July-January FY2024 (the corresponding figure for FY2023 was 16.3 per cent). According to World Bank (2024), import-related difficulties originating from the ongoing foreign currency crisis and reprioritisation of projects have contributed to this.

The government has taken some initiatives to reduce its subsidy burden in line with the IMF prescription. These include the reduction of export subsidies to several sectors, increasing electricity prices, and adopting a periodic formula-based price adjustment mechanism for petroleum products. The pricing mechanism for petroleum products was introduced in March 2024, which is expected to reduce subsidy requirements as a result of changes in international fuel prices. The government also issued a series of special bonds, at below-market interest rates, to clear arrears to fertiliser suppliers and independent power producers. These bonds, purchased by the domestic banks, will be eligible for Bangladesh Bank’s repo facilities and will be taken into account for meeting the statutory liquidity ratio criteria. This can be perceived as deficit monetisation and could counteract the central bank’s contractionary monetary policy stance.

According to IMED data, the ADP implementation rate against the original budget allocation reached 45.4 per cent during July-April of FY2024 – the lowest in the last ten years (Figure-1).

The slow utilisation of the ‘Taka’ component (i.e., the part of ADP that is financed by domestic resources) is the primary reason behind the overall slow implementation. On a positive note, within the components of ADP, project aid utilisation breached the 50 per cent mark after five years. This is commendable, given the ongoing foreign currency situation.

Among the top ten ministries/divisions that account for 70.2 per cent of the ADP allocation for FY2024, the ADP implementation of six was below the average level. These include the Road Transport and Highways Division, Secondary and Higher Education Division, Health Services Division, Ministry of Primary and Mass Education, Ministry of Water Transport, and Bridges Division. It appears that the trend of poor ADP implementation in the education and health sectors has continued in FY2024.

DEFICIT AND ITS FINANCING: As per MoF data, during the July-January period of FY2024, the budget deficit increased only marginally compared to the corresponding period of FY2023 – by Tk. 730 crore. However, significant shifts were observed in the composition of deficit financing. In the first seven months of FY2024, deficit financing was primarily reliant on foreign borrowing. The scenario was converse during the corresponding period of FY2023. Within the domestic sources, high dependency on scheduled banks for deficit financing was observed. In this connection, it must be noted that there is a considerable risk of increased government borrowing crowding out private investment, given the current tight liquidity situation in the market. A combination of tighter control over National Savings Certificates (NSC) issuance and less competitive interest rates resulted in net NSC sales by the government remaining negative in the first seven months of FY2024.

FIVE KEY PRINCIPLES: In view of the discussion so far, five key principles have been identified that should be taken into consideration for public finance management in the upcoming FY2025.

Enhancing fiscal space. Any attempt to enhance the fiscal space should focus on generating more resources as well as sealing the leakages. In the upcoming FY2025 budget, efforts to widen the tax base must be prioritised as part of the former. To this end, initiatives such as taxing the digital economy and digitalising the taxation system need to be given due attention. Analysing current tax exemptions in-depth with thorough data analysis needs to be a top priority for the government. There are also frontier issues that need to be addressed immediately, such as the meaningful taxation of wealth and property, and the growing digital economy. As part of sealing the leakages, curbing illicit financial flows (IFF) must be high on government’s agenda. At the same time, highest effort should be given to limit tax evasion and tax avoidance.

Prioritising expenditure. The framework for public expenditure in FY2025 needs to account for the ongoing rise in the price of essentials. The current austerity measures must be maintained in a way that their impact on the social safety net, health and education sectors, agriculture, and small and medium enterprises (SMEs) becomes less burdensome. Also, prior government directives to curtail “unnecessary and luxury” public expenditure (which includes purchase of government vehicles and international travel) should be continued. Exit plans will need to be formulated in the cases of fiscal incentives towards exports and remittances. If a market-based exchange rate regime is eventually put into place, the resultant depreciation should be able to cover the fiscal incentives currently being provided.

Prioritising foreign financing. Considering the declining foreign exchange reserve situation, the government should prioritise implementing all foreign-funded ADP projects. The government should give higher priority to implementing projects that are very close to their completion (about 90-95 per cent completion rate in June 2024). Availability of financing from foreign sources hinge upon ADP design and implementation capacities of the government agencies. Thus, rapid improvement in these aspects have become an exigency. In the case of availing budget supports, policy reform ends up being the determining factor. Thus, the government will need to become more accommodative in this regard.

Ensuring good governance. The political economy dynamics of Bangladesh have frequently impeded substantial reforms, even while the stakeholders have acknowledged their need. For example, political economy factors have played a significant role in the postponement, cancellation, and reversal of revenue mobilisation-related reforms, such as the preparation and implementation of the new Act on VAT, income tax, customs, related automation as well as tax administration reforms. In addition, the government must review public expenditure, especially in light of the hefty price tag of public investment projects and devise a strategy to ensure value for public money. It goes without saying that good governance and political buy-in from the highest level is a prerequisite in this regard.

Protecting the interests of vulnerable and disadvantaged groups. While enhancement of fiscal space and prioritisation of public expenditure ought to the centre stage in the public finance framework for FY2025, the associated economy-wide implications and equity concerns should not be undermined. Supporting the vulnerable and disadvantaged groups should be the central focus of fiscal management in FY2025. Design of both revenue and expenditure related measures need to take this into cognisance.

Dr Fahmida Khatun, Executive Director, Centre for Policy Dialogue (CPD); Professor Mustafizur Rahman, Distinguished Fellow, CPD; Dr Khondaker Golam Moazzem, Research Director, CPD; Towfiqul Islam Khan, Senior Research Fellow, CPD; Muntaseer Kamal, Research Fellow, CPD; and Syed Yusuf Saadat, Research Fellow, CPD. fahmidak.cpd@gmail.com; moazzem@cpd.org.bd; towfiq@cpd.org.bd.

[The paper is also contributed by Abu Saleh Md Shamim Alam Shibly, and Helen Mashiyat Preoty, and Foqoruddin Al Kabir, Senior Research Associates; Mashfiq Ahasan Hridoy, Research Associate; Jebunnesa, Faisal Quaiyyum, Anika Tasnim Arpita, Ibnat Hasan Sarara Jafrin, Sadab Rahman Chowdhury, and Ms Faiza Tanaz Ahsan, Programme Associates, CPD.]