Rationalising corporate tax policy

Ferdaus Ara Begum | Sunday, 20 April 2014

Revenue generation from taxable income is necessary for mobilisation and equitable distribution of domestic resources, wealth and for provision of public goods. A fair, effective and efficient tax system requires a commitment to address inappropriate tax practices, tax evasions and ensure a transparent and accountable tax regime. Bangladesh has a population of 160 million of which only 2.4 million or only 1.25 per cent of them are paying any income taxes. If the tax net is increased, burden on those who are willing to pay taxes could be reduced.

The corporate income tax (CIT), which is expected to be paid by the private sector of the country, is considered to be cumbersome and burdensome. Considering high cost of doing business and uneven business structure in Bangladesh, the CIT rate structure is exorbitantly high compared to similarly-placed countries. The Investment Policy Review prepared by the UNCTAD (2013) presented a comparative picture of general corporate income tax rates for 2012, showing the upper limit of CIT in Bangladesh at 45 per cent, while it is 30 per cent in Cambodia, 17 per cent in Singapore and 30 per cent in Philippines.

On the other hand, the tax administration authority, the National Board of Revenue (NBR) has also been suffering from anomalies such as shortage of required manpower, infrastructural and logistics requirements to address the present needs of the country so that tax avoidance within the private sector could be reduced. The present structure of CIT has raised questions as to whether it is a contributing factor to tax avoidance/evasion or whether reduction or re-structuring of the tax slabs could lead to widening of the tax net.

The NBR annual report defines income tax as a direct tax whereas import, export, customs duties, Value Added Tax (VAT), supplementary duty and turnover tax are all indirect taxes. The income tax is a progressive tax and among all the direct taxes, is one of the main sources of revenue of the government. "The more a taxpayer earns, the more he should pay'' is the basic principle of charging income tax which aims at ensuring equity and social justice (NBR. http://www.nbr-bd.org/IncomeTax/income_tax_at_a_glance_2012-13.pdf).

An individual as well as a company in Bangladesh pays income tax according to the provisions of 'The Income Tax Ordinance and Income Tax Rules 1984' and the complementary Finance Acts of each year. Among direct taxes, CIT is one of the main sources of revenue that contributed 31.45 per cent of the total revenue in 2012-13.

Business Initiative Leading Development (BUILD), a private sector-led public-private dialogue platform, undertook a research study to understand how tax regime in Bangladesh can be improved to create an attractive, equitable and competitive tax regime. It was aimed at harmonising incongruities in tax structure for the private sector (both domestic and foreign).

Specific objective of the study was to identify what constitutes an attractive, equitable and competitive tax regime from the perspective of the private sector that included analysis of the impact of uncompetitive CIT in the economy. Hence, taxation policies regarding CIT embody great significance because unattractive and uncompetitive tax policy could have adverse impact on businesses and the economy of the country.

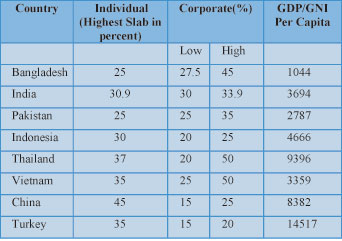

As per information from KPMG (http://www.kpmg.com/global/en/services/tax/tax-tools-and-esources/pages/tax-rates-online.aspx) on a comparative scenario of CIT in 2013, the Asian average of individual tax is 28.24 per cent against corporate average of 22.49 per cent, EU average is 37.85 per cent and for individual it is 22.85 per cent, African average is 29.11 per cent for individual and 28.57 per cent for corporate, and finally the global average is 31.91 per cent for individual and for corporate it is 24.08 per cent. It is of course presumed that those who have high per capita GDP can afford high individual income tax, and corporate rates of tax in these countries are relatively low, while the scenario is different in those countries where per capita GDP is low like India and Pakistan. Composition of GDP (gross domestic product) matters most for calculating differences of individual and corporate tax rates. Country comparison can be seen as follows: (http://www.theodora.com/wfbcurrent/bangladesh/bangladesh_economy.html)

A study among the SAARC member-countries also revealed that average CIT in Bangladesh is the highest at 45 per cent whereas Pakistan stands second with 35 per cent and India, which is one of the major economic powerhouses of the region, is at third with 33.9 per cent. Empirical studies showed that competitive CIT attracts more Foreign Direct Investment (FDI) and a reduction in CIT usually increases revenue collection in an economy. It is apparent from various FDI statistics that among the least developed countries (LDCs), CIT is one of the highest in our country and it could be one of the reasons for Bangladesh not being able to attract more FDI.

The Finance Minister stated in his budget speech that the tax-GDP ratio in Bangladesh is only 10.7 per cent, which is one of the lowest in Asia. Compared to Bangladesh, the ratio is higher by over 14 per cent in Nepal and over 4.8 per cent in India. The Heritage Foundation's 'Index of Economic Freedom' also confirms the dismal figure of the tax-GDP ratio of Bangladesh based on last fiscal year's performance. Countries which were also on the bottom of the list were Sudan 6.5 per cent, Afghanistan 9.2 per cent and Cambodia 10.7 per cent whereas the ratios are 45.8 per cent in Sweden, 35.0 per cent in the UK and 24.8 per cent in the USA.

The CIT has been progressively lowered since the 1990s from 40/60 per cent to present level of 37.5 per cent (general CIT), application range at lower level is 27.5 per cent and upper level is 45 per cent. Despite progressively lowering of the general CIT rate, it remains relatively unattractive internationally. Moreover, gradually declining trend of revenue collection from this source has been observed. As per the Economic Review 2013, while 30 per cent of revenue has been generated from Income Tax, the share of value-added tax at import and domestic level including supplementary duty is 51 per cent of the total revenue.

Alongside the high rates of CIT, taxpayers also suffer during audits by tax officials. There is no guideline in place to protect the rights of the taxpayers during audits and report on undue harassments. Furthermore, risk-based auditing system is absent. The need for audit is left solely to the tax officials' discretion.

Furthermore, there is a disparity of tax collection between rural and urban areas. Rural or sub-urban areas are somehow excluded from the tax net and therefore, strengthening connectivity of rural tax-centres with the central tax offices is one of the primary requirements.

In addition to CIT, a tax of 0.5 per cent of gross receipts is charged on all companies, irrespective of taxable income and potential losses. This tax is credited towards CIT obligations upon final assessment, but it constitutes a non-refundable minimum tax obligation. Advance payments on CIT must also be paid quarterly, based on the previous year's tax assessment. As sources of income are taxed, capital gains and losses are accounted for separately and taxed at a general rate of 15 per cent, with the exception of capital gains from the transfer of listed shares, which are taxed at 10 per cent.

Businesses create employment and contribute more to the economy than an individual tax-payer by paying VAT and other supplementary/indirect taxes. For this reason, the CIT rate is less than the individual income tax in any other country. The maximum threshold tax for an individual is 25 per cent, whereas for a company the rate is 37.5 per cent which is not acceptable in any measure. However, in Bangladesh the relatively high CIT induces most CIT payers to submit a contrived tax return.

There are more than 500 publicly-traded companies where more than a few hundred thousands have their investments. These companies are not able to evade the tax due to transparency, accountability and social responsibility. A cut in tax will reduce the tendency to avoid tax which eventually will increase the revenue of the government and will create a level playing field for the non-publicly traded corporate houses.

One of the major objectives of the Sixth Five Year Plan is to expand the tax base and rationalise the tax system. The NBR adopted a modernisation plan 2011-2016, objectives of which are to go for business process reforms and automation to facilitate compliance and reduce administrative costs. The NBR also has a Direct Tax Code in the process for replacing the 1984 Income Tax Ordinance. The present policy discourages tax payers as the burden of tax is more on those who choose to comply with. More progressive reduction of corporate income tax rates will encourage greater compliance on the part of corporate tax payers. At the same time, automation and modernisation policies should be expedited to reduce compliance costs. An in-depth study for rationalisation of tax structure which would take care of extrapolation of sources of revenue for government exchequer, cost benefit analysis to justify reduction in CIT and cross country comparison in the light of individual income tax base could be the most rational ways to progress further.

The writer is CEO, Business Initiative Leading Development (BUILD). BUILD is a partnership organisation initiated by Dhaka Chamber of Commerce & Industry and supported by

MCCI and CCCI.

ceo@buildbd.org