RCEP agreement may boost foreign investment in the time of pandemic

Tuesday, 17 November 2020

[As 15 nations on Sunday signed the Regional Comprehensive Economic Partnership (RCEP) agreement, one of the world's largest trade and investment pacts, United Nations Conference on Trade and Development (UNCTAD) published an especial issue of its Investment Trend Monitor. It argued that RCEP could give a significant boost to foreign direct investment (FDI) in the region. The Financial Express (FE) publishes slightly reduced version of the report in two parts. The first part appears here today.]

The Regional Comprehensive Economic Partnership (RCEP) initiative was launched in November 2012 and the negotiations of the Agreement started in May 2013. The RCEP Agreement, signed on 15 November 2020 is a major undertaking involving 15 countries, including the ten member states of ASEAN (Association of South-East Asian Nations), plus Australia, China, Japan, the Republic of Korea and New Zealand. ASEAN members are: Brunei, Burma (Myanmar), Cambodia, Timor-Leste, Indonesia, Laos, Malaysia, the Philippines, Singapore, Thailand and Vietnam.

RCEP is a broad integration agreement aimed at strengthening flows of trade, investment and services, as well promoting development cooperation across signatory states. It includes liberalisation, facilitation, promotion and cooperation measures.

RCEP is coming into effect at a time of great global economic and political uncertainty. This adds significantly to the importance of RCEP for member countries, as well as for third-country trade and investment partners. The agreement could help revive post-COVID economic growth, boost intra-regional trade and investment links at a time of global trade tensions, and provide a framework for further regional cooperation.

RCEP is coming into effect at a time of great global economic and political uncertainty. This adds significantly to the importance of RCEP for member countries, as well as for third-country trade and investment partners. The agreement could help revive post-COVID economic growth, boost intra-regional trade and investment links at a time of global trade tensions, and provide a framework for further regional cooperation.

This Invest Trend Monitor of the United Nations Conference on Trade and Development (UNCTAD) provides an overview of the current state of foreign direct investment (FDI) in the region and assesses the potential contribution that the RCEP agreement could make to investment flows. It focuses on implications for development, regional value chains, and post-COVID recovery prospects.

HIGHLY RELEVANT FOR CROSS-BORDER INVESTMENT: The RCEP Agreement builds on existing commitments on market access and disciplines for trade and investment and strengthens them in some areas. It provides a framework for further commitments to be negotiated in future.

The RCEP initiative ties together many overlapping issues covered in different free trade agreements (FTAs) and bilateral investment treaties (BITs) among countries in the region. It builds on elements of other agreements such as the ASEAN-China FTA, ASEAN-Australia-New Zealand FTA, ASEAN-Japan FTA, and the ASEAN-Republic of Korea FTA. Negotiations have been complex in part because there are as many as 27 existing FTAs and 44 BITs between RCEP countries. With the exception of Japan, all RCEP members including ASEAN as a group have FTAs with one another, all with varying provisions and rules and disciplines governing trade, investment and services.

RCEP will have important implications for FDI and value chain development within and outside the group. The RCEP Agreement contains measures in key areas such as market access, economic cooperation, and rules and disciplines (table-1). The specific provisions on investment could enhance investment opportunities in the long term, but the provisions related to trade in goods and services, intellectual property and e-commerce will do more to increase flows of investment in the short term by facilitating the exchange of goods and services, and by lowering transaction costs for business.

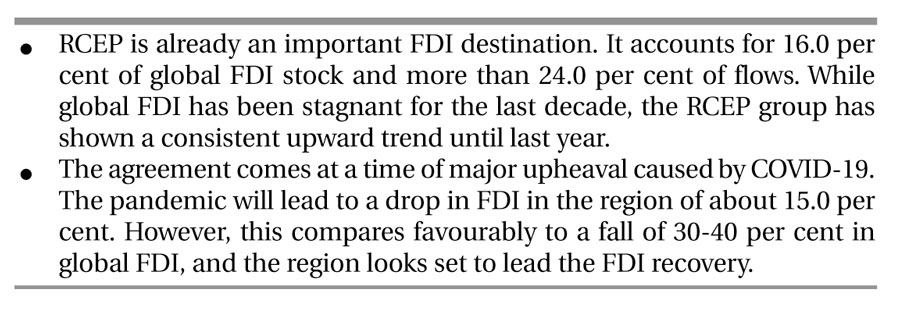

WORLD'S LARGEST TRADE AND INVESTMENT BLOCK BY SOME MEASURES: By some measures RCEP will create the world's largest trade bloc, with 30.0 per cent of world population, Gross Domestic Product (GDP) and goods exports. RCEP is 4.5 times the population covered by the Comprehensive and Progressive Agreement of the Trans-Pacific Partnership (CPATPP). The members of the Trans-Pacific Partnership grouping are Australia, Brunei Darussalam, Canada, Chile, Japan, Malaysia, Mexico, New Zealand, Peru, Singapore and Viet Nam. It is also more than five times that of the European Union (EU). By 2030, RCEP is projected to add about 0.2 percentage points to GDP growth in the region. It is also expected to boost exports of the members by over 10.0 per cent by 2025.

RCEP is a highly diverse group of economies. The members differ markedly in terms of their level of development and per capita incomes, economic structure and resource endowments. Three members -- Cambodia, Lao People's Democratic Republic and Myanmar -- are among the least developed countries (LDCs); China, Indonesia, Malaysia and Thailand are middle-income countries; and Australia, Japan, the Republic of Korea, New Zealand and Singapore are high-income economies. Several are rich in natural resources, including Australia, Indonesia, Lao People's Democratic Republic and Myanmar. The lower income countries still have a high agricultural contribution to GDP, while several high-income members are services economies and high-tech manufacturing hubs.

The region is a manufacturing powerhouse. The group accounts for nearly 50.0 per cent of global manufacturing output. About 50 per cent of global automotive and as much as 70% of electronics production are done in RCEP. The share of manufacturing in GDP is relatively high across most RCEP members, including the CLMV countries (Cambodia, Lao People's Democratic Republic, Myanmar and Viet Nam), which have rapidly increased (mostly low-tech) manufacturing output over the last decade, including with the help of FDI.

The diversity among RCEP members represents a significant challenge for integration efforts but presents even greater opportunities. It enhances the attractiveness of the group as a whole for investment, with complementary locational advantages among the members. And it provides catch-up development opportunities for the lower income economies that are as yet less integrated in trade and investment networks. Among the members, the share of exports in GDP ranges from less than 10.0 per cent to more than one third, and FDI stock ranges from less than 5.0 per cent to a multiple of GDP.

While the promotion of intra-regional trade and investment is a key objective for any economic partnership, the RCEP group is hugely important as a trade and investment block for the rest of the world. About 70.0 per cent of FDI inflows in RCEP are from non-RCEP economies. Extra-RCEP trade (exports and imports) is significant, and RCEP is also a major source of investment to the rest of the world.

GVCS IN RCEP: Most RCEP countries are highly integrated in global value chains (GVCs). The group accounts for 26.0 per cent of world GVC trade volume (including goods and services) and trade in intermediate goods is rapidly growing both within RCEP and with non-RCEP countries. The volume of GVC trade of RCEP countries increased by 34.0 per cent between 2010 and 2018.

Intra-regional value chain trade is growing even faster. GVC trade among RCEP members amounted to $1.5 trillion in 2017. This represents a growth of 50.0 per cent over the 2010 level. The potential for RCEP to support further intra-regional value chain growth could be especially important in light of the expected shifts in regional trade and investment patterns as a result of the trade tensions affecting China as well as post-COVID supply chain diversification and resilience-seeking investment trends.

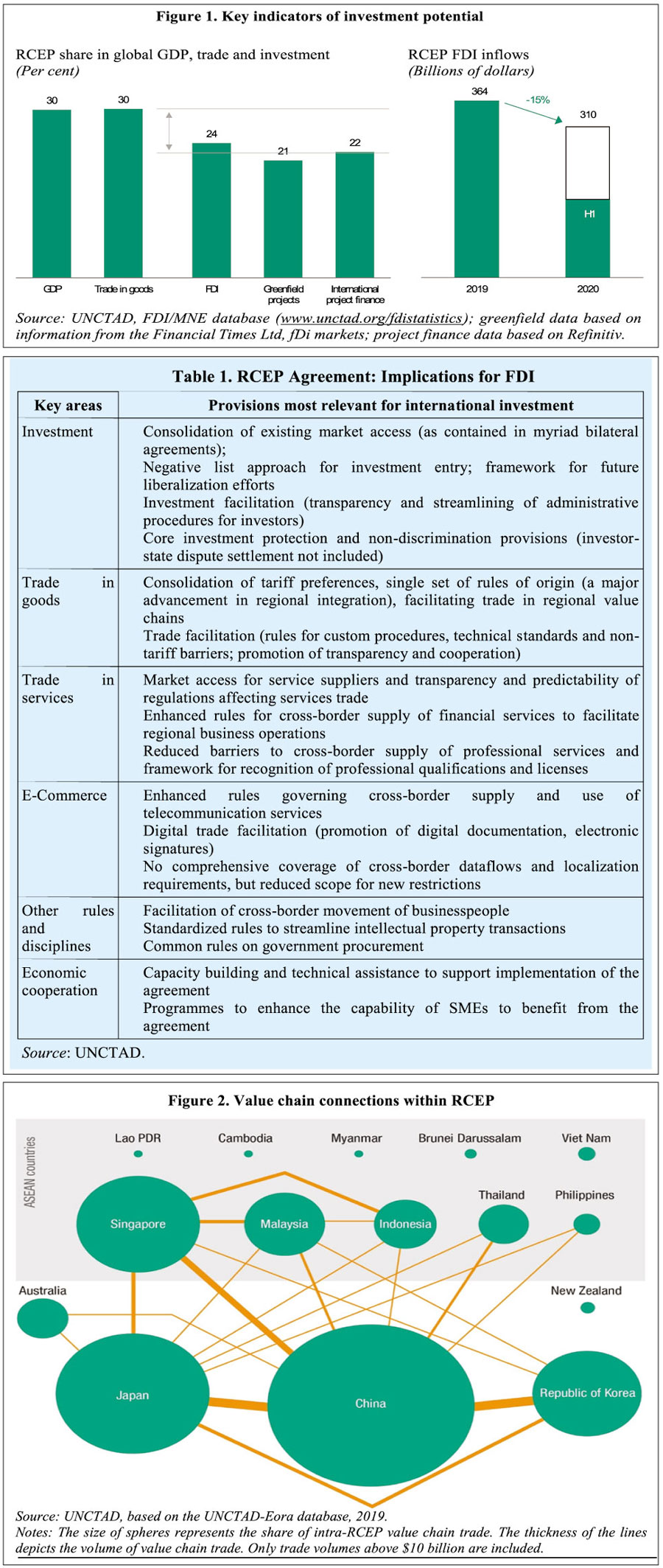

Notes: The size of spheres represents the share of intra-RCEP value chain trade. The thickness of the lines depicts the volume of value chain trade. Only trade volumes above $10 billion are included.

Value chain trade among RCEP members is centred around a few main nodes (figure-2). ASEAN as a group, China, Japan and the Republic of Korea are major GVC hubs. RCEP could be a growth opportunity for several smaller economies in the group that currently have a peripheral role in GVCs.

Five industries dominate GVC trade in RCEP, namely electrical and machinery, petroleum and chemicals, metal, textile and apparel, and transport equipment. These industries account for about 60.0 per cent of the region's total GVC trade. In electronics and machinery, RCEP members contribute 35.0 per cent of the total value added in global gross exports. This industry accounts for 24.0 per cent of total GVC trade in the world but for 37.0 per cent of the GVC trade of RCEP countries.

RCEP is an important global sourcing hub for these industries. For instance, about 47.0 per cent of Samsung Electronics (Republic of Korea) suppliers' factories accounting for 80.0 per cent transaction volume are based in other RCEP countries. Apple's (United States) supply chain involves more than 200 suppliers and about 800 factories. Some 80.0 per cent of these factories are based in RCEP (primarily in China, Japan and Republic of Korea). About 40% of the production facilities of Nissan and Toyota (Japan) are based in other RCEP countries. Volkswagen (Germany) and Ford (United States) each have more than a quarter of their global production facilities in RCEP grouping.

GVC patterns in the region are closely connected to FDI patterns. The top five GVC industries in RCEP account for more than 50.0 per cent of the value of greenfield investment project announcements in the group, with the highest share in petroleum products and chemicals followed by electrical and machinery. Although transport equipment has a lower share in the group's GVC trade, 10.0 per cent of new greenfield investment project announcements in 2019 were in that industry, suggesting it could expand in the coming years.

FDI TRENDS IN RCEP: RCEP is a major global FDI destination. FDI flows to the group have increased almost every year during the last decade, against a backdrop of stagnating global FDI flows. The upward trend was mainly the result of continued strong inflows in China and the ASEAN region. RCEP accounted for 24.0 per cent of global FDI flows in 2019. Growing annual inflows brought FDI stock in the group from $2.7 trillion in 2010 to $5.7 trillion in 2019, an average growth rate of 9.0 per cent per year. Exceptionally, RCEP FDI inflows fell by 4.0 per cent in 2019, to $364 billion mainly due to a significant decline in investment in Australia (-47.0 per cent to $36 billion) from high cross-border Merger and Acquisition (M&A)-driven levels in the previous year

In 2020, FDI in the region is projected to fall by about 15.0 per cent, based on FDI data for the first six months. Cross-border M&As, greenfield and project finance data for the first three quarters of the year suggest a similar trend. As in other regions, measures to slow the spread of Covid-19 are affecting the implementation of investment projects, the economic slowdown and slump in global demand is causing firms to reassess new projects, and corporate earnings available for reinvestment are drying up. The GVC-intensity of investment in the region reinforces the trend, as supply chain stoppages in the first half of 2020 hit typical GVC industries, and the longer-term trade policy implications of the pandemic are causing uncertainty for export-oriented investors.

FDI inflows in RCEP are concentrated in five countries (China, Singapore, Australia, Indonesia and Viet Nam). These countries accounted for 84.0 per cent of FDI inflows in RCEP in the last five years (2015-2019). In terms of inward FDI stock, China, Singapore, Australia, Thailand and Republic of Korea together accounted for 82.0 per cent of existing investment in the group in 2019.

RCEP is also a major and growing source of FDI for the world. The group accounted for 36.0 per cent of global FDI outflows in 2019, up from just 17.0 per cent in 2010. The rise in outflows pushed up outward FDI stock of RCEP economies from $2.4 trillion in 2010 to $6.5 trillion in 2019 - more than twice the growth rate of global FDI outward stock in the same period. A few countries are major sources of investment. These are Japan, China, Singapore, and the Republic of Korea. The high outward investment from Japan compared to relatively limited inflows into Japan are the main reason for the net FDI outflows from RCEP, even though most RCEP members remain capital importers.

INTRA-REGIONAL INVESTMENT: Intra-regional investment accounts for just over 30.0 per cent of FDI in RCEP. It is largely driven by a few major capital-exporting countries, including China, Japan, the Republic of Korea, and Singapore. More than 32.0 per cent of Japan's, 46.0 per cent of Singapore's and 38.0 per cent of Thai investment stock abroad is in other RCEP countries. About 40.0 per cent of the $1.7 trillion cumulative FDI flows in ASEAN between 2000 and 2019 are from within ASEAN (16.0 per cent) and other RCEP countries (24.0 per cent).

Despite the significant role that intra-regional flows already play among the RCEP economies, compared to other major economic groupings such as the European Union, the United States-Mexico-Canada Agreement and the Trans Pacific Partnership the current level of intra-RCEP investment is still low. The agreement could provide further impetus to strengthen intra-regional flows.

ASEAN's integration could be a blueprint for the potential impact of RCEP on FDI patterns. ASEAN's integration efforts have led to a rapid rise in intra-ASEAN investment and FDI from the region. While intra-regional greenfield investment among RCEP members at just over 30.0 per cent in 2019 was the same as in 2010, the share of intra-regional greenfield investment in ASEAN doubled from 10.0 per cent to more than 20.0 per cent in the same period. Inflows into ASEAN from other RCEP countries kept pace with intra-ASEAN flows, suggesting the current agreement is a logical extension from an investment perspective.

[Source: www.unctad.org]