Restoring stability in the banking sector

Asjadul Kibria | Sunday, 23 November 2025

The financial sector in Bangladesh is at a crossroads now amid the interim government's hectic efforts towards widespread redressal of irregularities, which has been long overdue. The task is challenging, and there is no quick fix for the problems created, deliberately or otherwise, by the previous autocratic government to facilitate plundering by its cronies. The result is a gradual erosion of the financial sector's strength and stability, increase in loan defaults, and weakening of several private commercial banks. Though signals of the financial sector's increased vulnerability were evident during the last few years of the now-ousted regime of Sheikh Hasina, regulators were unable to intervene effectively. In fact, the regulatory bodies became a part of the problem, as they were headed by unscrupulous and partisan officials devoted to serving crony capitalists. Control, tacit or otherwise, exercised by the autocratic regime also made it difficult for the media to publicise a series of irregularities in the sector. Nevertheless, some media had persistently tried to reveal the gross irregularities defying the pressure from the autocratic regime.

After the fall of the Hasina regime on August 5 last year in the face of a student-led mass uprising that claimed the lives of at least 1,400 people, the Yunus-led interim government has taken a number of steps to address the vulnerabilities of the financial sector. During the ousted regime of Sheikh Hasina, loan defaulters received undue concessions and bank board directors got tenure extension. All these meant to enable the ruling-party cronies to loot the banks. These two factors made the overall financial sector more vulnerable. Data manipulation, backed by the past autocratic regime, also hid many real issues of the financial sector and provided a misleading picture.

The Bank Company Act 1991 put a restriction on the tenure of private bank directors for six years, which was removed in 2003. In 2013, under pressure from the International Monetary Fund (IMF), the act was amended to reinstate a six-year cap on a director's tenure, coupled with allowing two members of a family on the board. In 2018, the act was amended further to extend the director's tenure to nine years and the number of family members increased to four. In this process, the cronies of the autocratic regime tightened their grip, undermining the good governance in the banks. Five years later, in an aggressive move to expand the irregularities in the banks and allow massive-scale embezzlement, the act was further amended. Under the 2023 amendment, the director's tenure was extended to 12 years. Moreover, directors already on the boards were also allowed to continue for another 12 years. In this process, directors who were on the boards before 2013 also got an opportunity to hold the positions for a consecutive 20 years until 2035. The number of family members on board increased to five, including family affiliates.

As an effort to remove these distortions, the central bank has recently decided to cut the number of directors from a single family and their affiliates on bank boards from five to two. It also decided to restrict the continuation of a director's term on the board from 12 to six years. The draft amendment of the bank company act includes provisions which would be helpful to restore good governance in the banks by reducing family dominance.

The supporters of the ousted regime are trying to spread misinformation about the instability of the country's financial sector to mislead the people. They are, however, totally silent on how the ousted regime gradually distorted the financial sector and made the banks vulnerable.

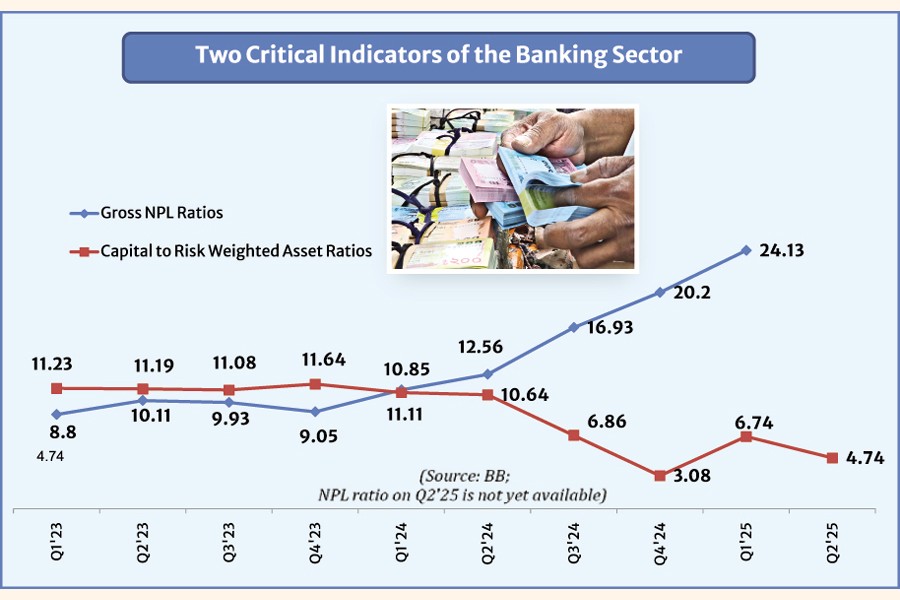

Central bank statistics showed that the banking sector-wide Capital to Risk-Weighted Assets Ratio (CRAR) declined to 10.64 in June 2024 from 11.64 in December 2023. It further declined to 3.08 per cent in December 2024 and increased slightly to 4.47 per cent in June this year. So, the aggregate regulatory capital of the banking sector amounted to Tk 839.46 billion at the end of FY25, reflecting a shortfall relative to the stipulated minimum requirement of Tk 1,917.09 billion. Nevertheless, the positive thing is that most banks remained compliant with regulatory capital requirements. The Quarterly Financial Stability Assessment Report (April-June 2025), released by the central bank this month, showed that out of 61 banks, 39 maintained CRAR at or above 10 per cent of the regulatory minimum requirement. The downside is that 22 banks with CRAR below 10 per cent held more than two-fifths of the banking sector's total assets and around half of the total liabilities at the end of June this year. It means the banking sector is still vulnerable.

The sharp rise in non-performing loans (NPL) in the banking sector is another serious concern that also makes the financial sector vulnerable. The gross NPL ratio of the banking sector was 8.80 per cent at the end of FY23 which increased to 12.56 at the end of FY24 and further jumped to 24.13 per cent at the end of March this year. As a result, a large amount of capital is locked in NPLs limiting availability of funds for investment in vital sectors. Bangladesh Bank itself asserted: ""The banking sector is currently at a critical juncture, with ballooning NPLs, sluggish credit growth, and capital inadequacy. Good governance and structural reforms remain the priorities in addressing these challenges."" (P-25, Bangladesh Bank Quarterly, April - June, 2025).

A number of factors are behind the rise of NPLs after the July mass uprising. Earlier, banks were forced to conceal some NPLs under political pressure, coupled with some tricky measures. No such things exist now, and real pictures of NPLs are emerging. And, big cronies of the ousted regime are on the run and not repaying the due loans as their business and commerce are also disrupted heavily. The revaluation of the assets of five recently merged banks also contributed to an increase in NPLs by Tk 700 billion alone. Four of these banks were taken over by a big crony who siphond large sums through various irregularities.

To streamline NPLs, the central bank issued a master circular in November last year that tightened classification rules. The rules, effective from April this year, will further enhance NPLs. Thus, the country's financial stability would also be shaken. Nevertheless, what is more important is to get an overall picture of the financial sector's vulnerabilities. Otherwise, it will not be possible to fix the sector and make it stronger in the long run. That's why the alarming but accurate data on the financial stability is a must.

asjadulk@gmail.com