Risk based pricing: a safeguard for the banking industry

Nahid Ul Hasan | Saturday, 18 January 2025

Risk-based pricing is gaining growing attention in today's business world full of risk imbalance. As all customer groups do not mirror the same look on a business scale, all cannot share the same cost burden alike. It has been around for many years and has been recommended by many credit risk managers as a way for businesses to compensate for the risk of different customer segments. The theory is relatively simple. With fixed pricing, the cost of risk is evenly distributed among customer segments despite the fact that certain segments have high risk and others lower risk. This situation results in the lower-risk customers "paying" more than their risk -- essentially being overcharged -- while the higher-risk customers pay less than their risk.

In our present market perspectives, different interest rates and loan terms are offered to different borrowers, based on their credit worthiness. To substantiate credit worthiness, risk-based pricing focuses on factors such as a borrower's credit rating through External Credit Assessment Institutions (ECAI's), Audited Financial Statement, Risk Weighted Asset (RWA), Capital Charge, Cost of Capital/ Return on Equity (ROE) and Income depending on the type of loan. It does not consider factors which are irrelevant such as race, colour, national origin, religion, gender, marital status or age.

The continuous forward movement of classified loans in our economy is deeply skewed towards particular strata of high risk borrowers while the price burden is equally spread over the good ones. Had there been a good measure to price the credit risks, bank's losses from impaired assets could have been less or at least good borrowers would have been rewarded by a significant price comfort. Here comes the relevance of risk based pricing before lending any type of investment to secure depositor's money as well as stakeholder's safe return.

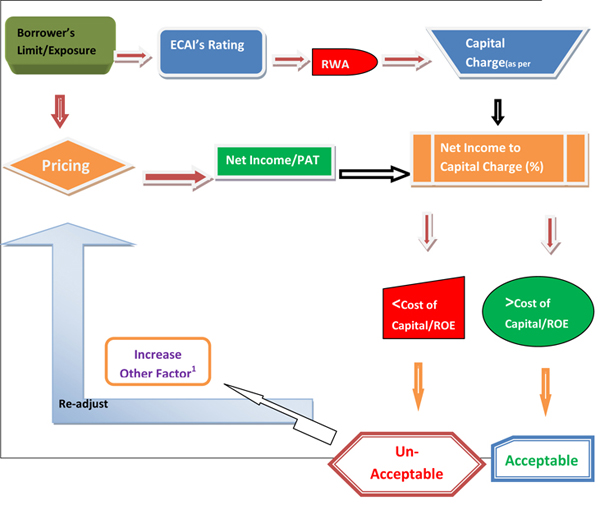

In this regard, this scribe has developed the 'Risk Based Pricing Model' considering credit risk to identify the credit risk and to assess the proper lending rate/pricing customer-wise.

The model shows how a borrower's Risk Based Pricing is followed through Net Income [Profit after Tax (PAT)], Risk Weighted Asset (RWA), Capital Charge, Net Income to Capital Charge ratio. If Net Income to Capital Charge ratio is greater than the Cost of Capital/Return on Equity (ROE), the pricing will be acceptable, otherwise the pricing will be un-acceptable or need to be re-adjusted to the pricing or increase the other factors like fee-based income, cash collateral, cash margin that would reduce the capital charge of the client and increase the Net Income to Capital Charge ratio.

User of the model has to decide ROE/Cost of Capital first. To assess your borrower through the model, you have to consider the borrower's ECAI's rating, Customer's Limit/Exposure, proposed pricing/margin, Cash Collateral, Cost of Deposit, Overhead Cost, Provision and Fees & Other Income (if any). The following flowchart describes a detailed picture of the model:

The model gives you the appropriate pricing to lend money for sustainable return.

Risk-based pricing allows lenders to charge higher interest rates to borrowers who seem less likely to repay their loans in full and on time or having higher Risk Weighted Asset (RWA) to charge higher capital, and lower interest rates to borrowers who seem more likely to repay their loans in full and in a timely manner or having lower RWA to charge lower capital. For example, if your ECAI's credit rating category shows that your long term rating is not good, you might be charged higher interest rate than someone who has good long term credit rating.

Exceptions:

i. If the risk distribution (risk score) is skewed to the left, the quantity effect might exceed the price effect and therefore the risk-based pricing strategy might be unprofitable. Alternatively, if the quantity of bad exceeds the quantity of goods in the market, the risk-based pricing strategy might be unprofitable, too.

ii. By differentiating the interest rates charged to each identified risk group, lenders may inadvertently worsen the average level of risk of their portfolio as a whole.

iii. If the lender has insufficient information to reliably distinguish low risk from high, it might be convenient to set a flat interest rate strategy rather than using a customised pricing strategy.

PROMOTING CREDIT CONSCIOUSNESS AND DISCIPLINE: Several reports and case studies of World Bank have shown that a risk-based pricing environment based on credit information data improves loan performance by reducing delinquency rates and contains non-performing assets. Credit penetration is achieved by significantly identifying "good borrowers" (low credit risk) that otherwise would have been misidentified as "bad borrowers" (high credit risks) and, therefore, may not have been provided credit at optimal terms and conditions. At the same time, high-risk borrowers are no longer subsidised by lower-risk borrowers. Risk-based pricing of loans could be a major motivating factor for borrowers to ensure they maintain a healthy credit history and a high credit score.

Rewarding the good has been an age-old practice. If a borrower has been paying back his/her loans on time, he/she is a good borrower. And if the aforementioned adage is followed, he/she could expect to be rewarded with a lower rate of interest the next time he/she applies for a loan. This practice of rewarding good borrower is yet to gain acceptance by the country's lending institutions.

To ensure that good borrowers are rewarded for their financial discipline, my own observations is that all credit institutions and banks in the country should adopt risk-based pricing to lend money for sustainable credit growth, prevent the continuous forward movement of classified loans, build strong capital base and provisions, secure depositor's money as well as stakeholder's safe return.

As per widely accepted global rules, a country poorly credit rated by Moody's or S&P and Fitch bears the burden of rising cost of business in terms of trade cost, correspondent relationship, foreign guarantee, various credit lines etc., while a better rated country reaps the fruits of lower business cost. In rhyme with this kind global practice, the Risk Based Pricing Model as developed and followed by the all banks among the industry will be a step forward to bring justice and equilibrium in our credit culture. This will help the banks not only reward the good customers while identifying the bad, but also prevent both continued credit loss and subsidised credit expenses facing the banking industry in recent time.

Nahid Ul Hasan is Deputy CRO, Dhaka Bank PlC. nahidulhasan380@gmail.com