Risks of e-Banking in Bangladesh: A critical perspective

M. Nazmul Khan | Monday, 31 July 2017

If we are ever asked "Why e-Banking?" by someone, we would probably be able to come up with more than one benefits that electronic banking yields in our day to day lives. It is changing the way we conduct our financial affairs fundamentally. Convenience and control are the wants of today's busy users, and that's exactly what e-Banking offers.

The other reality of our lives is the fact that there are no unmixed blessings. For all its tremendous benefits, e-Banking has its own share of hazards as well. There are several dimensions to risk in this particular form of financial service delivery platform, which I am going to discuss. But first, let us delve into the features that make e-Banking so exciting.

The most significant advantage of e-Banking comes from doing away with slower, more traditional methods. This is accomplished by consolidating the relationships a bank has with its clientele into a more centralised architecture with a common digital interface. That requires keeping track of all the data belonging to the entire client base centrally.

It is this consolidation that improves upon older branch network model of banking where each branch serves a geographic niche as a relatively self-sufficient entity in terms of service. In the e-Banking model, all the users are served from the same platform which allows them access to control their respective accounts remotely. It saves time, cost, and manpower, allows for greater customer satisfaction, and above all, it helps profitability.

In the days of paper based transactions, smaller volume, personal acquaintance of client and banker as well as tested and tried methods of verification provided easier control over banking transactions. But when customers are allowed remote access to their accounts through a digital platform, many of the traditional risk controls are obsolete. Digitisation has forced a complete rethinking of how to detect and prevent banking frauds.

Operational risks in e-banking can be traced back to three sources: outsider fraud, unscrupulous banker, and unaware customer.

If information is power, then with the opportunity to exploit vulnerable service platforms with massive clientele databases, the fraudster of today is more powerful than ever. With each advance in technology, a whole array of attempts to breach security mechanisms are showing up. In countries with a brief history of digitisation, like ours, the vulnerability is always much greater. Coping with a new way of doing business can be tough at times.

The recent hack-heist of Bangladesh Bank has highlighted what can go wrong when new technologies are left exposed because the likelihood of security events were deemed miniscule. It has dented confidence of the populace and made the central bank look weak as an institution, particularly because BB is looked up as the guardian of the banking industry.

The second source of problems, the bankers themselves, arises because the people who manage e-banking platforms directly are detached from the clients personally. Like an efficient bureaucracy, this whole operation is consolidated in a small number of locations with customers having no direct access to people who are maintaining the infrastructure.

The presence of this connection has been an important factor in inhibiting the older generation of bankers from engaging in taking advantage of the trust of their clients. But that is not an operative force in e-Banking, where the people managing it and people using it are further apart. The removal of a psychological barrier makes the system riskier. If a banker decides to go rogue, as occasionally some do, the consequences can be damming.

But all the while when we are talking about threats from the supply side, the role of demand side in failing to manage risks cannot be overstated. Each banks targets a specified profile of customers, not all of them are capable of handling an online facility with efficacy.

A multi-national bank with globally proven security arrangement and sophisticated clientele are more likely to withstand country specific risks better. If an aspiring local bank -- with a clientele that is more accustomed to traditional methods and less tech savvy -- chooses to introduce an e-banking platform or even a mobile banking channel first must make sure that their clients are aware of the potential and hitherto unseen threats.

Clients segments with less exposure to technological sophistication of the modern age that are not quite vigilant in preventing compromise of the security of their own accounts by disclosing passwords casually or leaving deposits without much monitoring are more likely to be targeted by frauds and unscrupulous acquaintances.

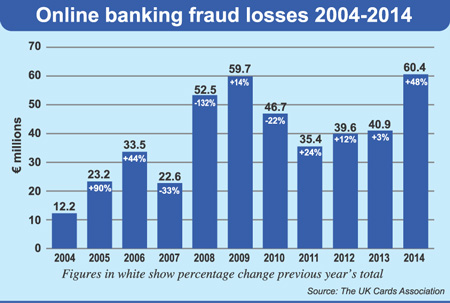

Globally & domestically, the most common e-banking fraud is ATM (automated teller machine) fraud, with skimming devices installed in ATM Booths stealing client information to copy legitimate cards and using these to purchase merchandise the value of which are charged to the original card.

The most rattling instance of the detection of such fraud was not long ago; only a year earlier, Eastern Bank Limited, one of the market leaders in card category was hit with a foreign linked fraud operation, which quickly unraveled thanks to the prompt and effective response of all involved. Such instances are on the rise globally:

So far, I have only shed light on operational risks; but this new channel can bring devastation to a bank or even the industry if handled with half-hearted acceptance. Procuring the right systems, hiring the right people, and implementing a holistic control framework all goes hand in hand; the result is successful mitigation of a strategic risk.

Many banks have management who are still coming to grasp with the beneficial potential of the e-Banking channel, but are yet unsure about how to implement one in their own institution. Yielding to competitive pressure or the fear of seeming to lag behind in embracing innovations, they may take a bite larger than what they can chew.

In a branch environment, operational failures can easily be depicted as having more to do with control failure in a specific location, but the reputational risk of a mess up in e-Banking platform will become a blemish for the entire bank, or even the industry as a whole. Full centralisation of service operations implies branches act as sales hub only, and that means newer recruits in the bank will become specialised only in their own fields.

The only role left for branch people to play in this model will be that of salespeople, and in most cases they will be as clueless as to the inner workings of the giant machine as the clients themselves. The people who can be the best guides, technical experts running the e-banking platforms, will be too far away to be useful informationally. Unless the internal communication & troubleshooting system is robust enough, that can bring along disaster.

The history of e-Banking in our country is still too brief for us to take solace in the absence of any major catastrophes till date. Although a few incidents of credit card & ATM frauds have been detected and prosecuted in the last year, so far no major breach in the security of customer information in the commercial banking industry has been reported. This does not mean that we are secure; it simply means that there is still time for us to take it seriously.

In the end, the cutting edge of a sword cuts both ways; a little bit of carefulness can go a long way in making sure and our banking system which is battered by slow growth and lowering interest rates, non-performing loans, and scandals one after another is not seized by another misfortune while we wait complacently.

In the end, e-Banking here can either become a masterpiece in innovation, or a case study in manmade disaster, the choice lies with the industry and policy circle. The benefits of e-banking is large, and the potentials enormous. Even with all these grim admonitions, we cannot possibly overstate the positive role it can play in modern lives. The only thing that can complement the benefits is a robust sense of responsibility on part of all stakeholders to make it a success in Bangladesh, something which is never a too much to ask for.

M. Nazmul Khan, nazmul_khan@outlook.com, Treasury Analyst, ACI Limited