Should the central bank control interest rate?

Md Jamal Hossain | Tuesday, 4 March 2014

The traditional outlook has been that the central bank should control the interest rate whenever the necessary and proper situation arises. This necessary and proper situation is not very clear-cut also. What do people actually mean when they ask for intervention in the interest rate charged by commercial banks and demand to decrease the same? This kind of demand and reasoning are utterly confusing because the central bank is a single entity and it can't by any means control the interest rate locating and determining what the appropriate rate should be. To locate the proper interest rate that would not disturb market and would restore the equilibrium, the central bank would have to possess the omnipotent power possessing every kind of information under its command. But this is hardly the case and the central bank is just a single entity among thousands and millions of entities operating in the market that also possess variety of information that the central bank doesn't have at all. In this respect, the central bank has to probe each and every entity to gather the all information and in doing that central bank would jeopardise its useful existence.

More than five decades ago, Frederic Hayek raised this view in an extraordinary article (The Use of Knowledge in Society -1944). In that article Hayek argued that: "The peculiar character of the problem of a rational economic order is determined precisely by the fact that the Knowledge of the circumstances of which we must make use never exists in concentrated or integrated from but solely as the dispersed bits of incomplete and frequently contradictory knowledge which all the separate individuals possess. The economic problem of society is thus not merely a problem of how to allocate given resources …. It is rather a problem of how to secure the best use of resources known to any members of society…. Or to put it briefly, it is a problem of the utilisation of knowledge not given to anyone in its totality."

If we closely analyse Hayek's statement, we find two critical things: (a) Knowledge never exists in concentrated and integrated form but in dispersed bits. (b) Dispersed bits of knowledge are not possessed by any entity in totality but by every entity.

If Hayek's statement carries any significant meaning, it carries perfectly the message for centralised control of economic problems and matters. Hence, a critical message for central bank as well. Hayek's statement shows how much justified it is to say that the central bank should control the interest rate. In fact, interest rate is not a single rate but a composition of diverse rates to which each entity is subject to. Each rate carries a different information and signal of different circumstances and different economic knowledge. If the central bank were to control the interest rate, then it would have to be an omnipotent institution knowing all the information which is totally impossible. In this short exposition, we will show the following things. (1) Every time the central bank fixes the interest rate, it is more likely that the central bank will find that its rate either falls below the equilibrium rate or stands above the equilibrium rate. And that creates the troubles for the economy. Here by the term, fixing interest rate, we mean a direct control on the interest rate, for example, direct slashing of interest rate. (2) Whether the difference between the interest rate fixed by the central bank and the real equilibrium rate will be zero is a pure chance and this chance has no predictable aspect. (3) If the central bank were to control interest rate, the only way it can do so without disturbing market equilibrium much is through applying the qualitative slashing of interest rate not the quantitative slashing of interest rate.

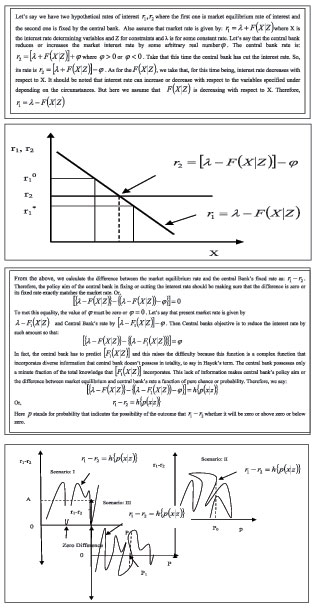

CENTRAL BANK AND INTEREST RATE: If we take it for granted that the central bank doesn't possess all the information that is necessary to fix the interest rate so that it should match the market equilibrium rate, then we can give answer to our first point that every time the central bank fixes the interest rate, it either falls below or stands above the equilibrium rate. To show that, we can imagine a situation in which a pure market equilibrium rate is given - in fact it is not given but can be conceived - and a rate fixed by the central bank is also given. We also think that market equilibrium rate of interest is determined by some factors given some constraints. In other words, we can say as follows:

Now we can show the above two rates in the following graphical manner:

In the above figure, market rate (r1) and central bank's rate (r2) are measured off in the vertical axis and the variable X on the horizontal axis. The graph shows that the central bank's rate r2 either falls below the market equilibrium rate r10 or stands above the market equilibrium rate r1*. The central bank's fixed rate is shown by the heavy horizontal black line in the above graph. If this is the case, that means if central bank's rate doesn't match with the equilibrium rate, market equilibrium will be unnecessarily disturbed by central banks arbitrary fixing of the interest rate. The rate fixed by central bank is an arbitrary rate because it doesn't incorporate all the necessary information that a pure market rate or r1 contains. Now the relevant question is: why doesn't central bank's rate fixed rate match the market equilibrium rate? Rephrasing the question once again, we ask: Is it possible to derive any predictable content that central Bank's fixed interest rate will match the market rate? Let's us get the answer.

CENTRAL BANK'S FIXED RATE AS A PURE CHANCE: To get the answer to the question why central bank's fixed rate will not match the market rate or to derive the predictive content of central bank's rate to predict market rate, we can proceed as follows:

The above function that relates difference between the market rate and central bank's rate to probabilistic estimate has some critical features. First, it indicates that such difference is not a simple probability estimate but a function of the probability. Second, the probability estimate depends on the x which represents the information that each every entity bears in the economy given the constraint z. Now if we depict this function in the graphical form, we get the following fuzzy pictures:

In the above graph (Scenario: I), difference between the market rate and central bank's rate is measured off in the vertical axis and the probability on the horizontal axis. As the graph shows, there is no particular or definite shape for this function. It moves erratically. Its erratic move can be checked by checking the same value of (r1-r2) at different probability estimates. This is shown by A in the scenario I. The value A is true for different probability estimates and we can't single out a single probability estimate at which we find the unique value of A. Moreover, zero difference occurrences are very rare given the range of probability estimate. Only at two definite probability estimates, zero difference between market rate and central bank's rate results out or (r1-r2=0) in the scenario I.

To explore the fuzziness of the above function, we depict another plot of the function in the scenario II in the above figure. This shows more erratic movement compared to Scenario I. The graph shows, for example, that at some definite probability estimate called P0 in the graph above, the value of (r1-r2) is quite different. No single unique value of (r1-r2) can be attached to the definite probability estimate P0. This clearly shows how reasonably the central bank can predict market rate of interest so that difference (r1-r2) becomes zero. More interestingly, the scenario II shows no outcome at which difference between market rate and central bank's rate is zero or (r1-r2=0) at some probability estimate.

The scenario III depicts a fuzzier picture than scenario II. It shows that at the probability estimate P1 the difference between r1and r2 can be positive zero or negative. All the three scenarios show how much rare the actual outcome would be at which (r1-r2=0) and how much unpredictability is there in predicting an interest rate by the central bank at which the difference between market rate and central bank's rate is zero.

A COMPLETE FUZZY PICTURE: The above two graphical views show how much fuzziness is involved in central bank's conventional attitude towards controlling interest rate and locating a feasible rate that would not produce precipitation in market. In fact, the central bank is never tired of learning from its grave mistakes in the past and, ironically, people still want that the central bank should fix the interest rate setting some ceilings. To this we can remember a lesson from Hayek's business-cycle theory. He wrote in 1933 and showed the evil role of money in creating cycle downturn and upturn. Though people question heavily on the ability of Hayek's business-cycle theory to explain cycle downturn and upturns (for this reason one can consult the Gottfried Haberler's article titled Reflections on Hayek's Business Cycle and Nicholas Kaldor's writing on Hayek' business cycle), the lesson from Hayek's business cycle is very powerful one. The lesson is that if the channeling of money is disturbed by the manipulation of interest rate, the consequence can be very grave. This, along with the above exposition, reveals that in most of the cases the central bank will disturb the market equilibrium disturbing the channeling of money in market by its undue manipulation of the interest rate.

PRESENT HIGH LIQUIDITY PROBLEM: Now we can apply the above theoretical insight to comment on the present high liquidity problem in our country. Suggestions are coming from the different fronts that the central bank should curb the high interest rate. What do they actually mean by high interest rate? The relevant questions to ask are: Aren't the banks aware of the high liquidity at their hands? If they are, why don't they reduce the interest rate? Surely, the central bank doesn't know better than what a single commercial bank know about its dealing in the market. Now if, for example, the central bank takes the initiative to cut the interest putting some ceilings on the interest rate charged by commercial banks, then how can the central bank assure us that this rate will not disturb the market more than the previous rate? The above analysis shows that the central bank can never assure us about this. To assure us about this, the central bank would have to be such an omnipotent institution that has command over each and every piece of information in the market about the dealings of numerous entities. We wish we could have such a central bank!

The high liquidity problem can more efficiently be dealt with without disturbing market by the discretion of commercial banks, not by the central bank. If this is so, then what is the role of the central bank in the present case?

The central bank should encourage commercial banks to follow some discretionary rules that can be applied to every bank without contradicting their rational objective - the return maximisation. For this purpose, it can encourage banks to apply some discretionary banking practices such as credit rationing rule, strong and judicious credit worthiness test procedure, etc. These kinds of instruments will not disturb the normal market operation creating ups and downs. Rather they will produce a result that will be shared and enjoyed by the economy as a whole not only in terms of reduced interest rate and interest spread but also increased supply of credit while driving out bad investors, defaulters, and cheaters from market.

The contributor writes from the University of Denver, USA. jheco.du@gmail.com