Socially responsible investment: Sustainability concerns

Muhammad Abdul Mazid | Sunday, 24 November 2019

![]() Socially responsible investment (SRI) is an umbrella term to describe an investment process which takes environmental, social, governance (ESG) or ethical considerations into account. SRI is not a new concept and has gone by many names throughout the years: Values-based investing; Ethical investing; Green investing; ESG investing; and most recently, sustainable and responsible impact investing.

Socially responsible investment (SRI) is an umbrella term to describe an investment process which takes environmental, social, governance (ESG) or ethical considerations into account. SRI is not a new concept and has gone by many names throughout the years: Values-based investing; Ethical investing; Green investing; ESG investing; and most recently, sustainable and responsible impact investing.

SRI tends to mimic the political and social climate of the time. More than 175 years ago, Karl Marx (1818-1883), a political theorist, commended an SRI-aligned positive initiative for ethical conduct in workplace relations, production, and environment. The growth of SRI emanated in the 1990s from a combination of legislative compulsion and pressure from actual and future beneficiaries. As awareness has grown in recent years over global warming and climate change, SRI has trended toward companies that positively impact the environment by reducing emissions or investing in sustainable or clean energy sources.

Common themes for socially responsible investments include avoiding investment in companies that produce or sell addictive substances (such as alcohol, gambling and tobacco) and seeking out companies engaged in social justice, environmental sustainability and alternative energy/clean technology efforts.

Social responsibility is the idea that businesses should balance profit-making activities with activities that benefit society; it involves developing businesses with a positive relationship with the society in which they operate. The International Organisation for Standardisation (ISO) emphasises that the relationship with the society and environment in which businesses operate is “a critical factor in their ability to continue to operate effectively. It is also increasingly being used as a measure of their overall performance.” There as two inherent goals of SRI: social impact and financial gain. The two do not necessarily go hand in hand; that an investment touts itself as socially responsible doesn’t mean that it will provide investors with a good return. An investor must still assess the financial outlook of the investment.

Rising demand for SRI

Societies now feel passionate about a range of issues such as effects of climate change, use of sweatshops, production of weapons of mass destruction, effective use of natural resources, a rapidly growing and ageing population or corporate, environmental and social practices of companies. The recent global financial crisis made more investors aware of the importance of good corporate ethics, governance and environmental issues while examining the future worth of any investment.

While responsible investment was once considered a fad, today it is a very mainstream investment style with responsible investors coming from all walks of life and across all ages. There are many varied and universal reasons why someone may be motivated to invest responsibly: (a) Interest in social issues, or membership to community, environmental, political or human rights organisations; (b) A scientific background or passion for new energy technologies as a way to solve problems of climate change; (c) Belonging to a faith-based or other spiritual organisation; (d) Simple enjoyment of being close to nature, and wanting to ensure its preservation.

Religious investing

SRI is often chosen according to stated religious beliefs, for example Judaism, Christianity, or followers of Islam. In fact, the history of SRI goes back to the ethical precepts embodied in Jewish law. Quakers and other religious orders starting in the 18th century refused to invest in “sinful” industries such as distilleries and weaponry. The first SRI mutual fund was Pax World Funds, a $1 billion fund created in 1971 by Luther Tyson and Jack Corbett, both of whom worked for the United Methodist Church. In 2004, faith-based organisations filed 129 resolutions, while socially responsible funds filed 56 resolutions.

Islamic social scientists believe the Zakatis are compatible with principles of economic and social equity. Muslim socialists have found their roots in anti-imperialism. Muslim socialist leaders believe in derivation of legitimacy from the public. Zakat promotes a more equitable redistribution of wealth and fosters a sense of solidarity amongst members of the community. Zakat is meant for discouraging hoarding of capital and stimulating investment. Because the individual must pay Zakat on the net wealth; so wealthy Muslims are compelled to invest in profitable ventures, or otherwise see their wealth slowly erode. Furthermore, means of production such as equipment, factories and tools are exempt from Zakat, which further provides incentive to invest wealth in productive businesses.

Jeebika is a Livelihoods and Human Development Programme developed by the Center for Zakat Management (CZM) in Bangladesh to ensure sustainable socio-economic development of the hardcore poor. Through a baseline survey, the Zakat-deserving households are identified and grouped in grassroots organisation comprising 25-30 families. They open a joint bank account and a certain amount of Zakat money for each family is deposited to their account. Besides they are advised to form a savings fund. The group members, with a view to doing business can take interest-free investment from their joint account. After engaging in business as per Shariah rule, the members can carry the lion’s share of their profit to family and equally share a portion with other members of the group.

The project also provides other services like healthcare, safe water and sanitation facilities, child and adult education, skills development training and awareness building. Thus, all the members are engaged in establishing a friendly society.

The Jeebika Karnaphuli project was a small-scale experimental livelihoods project focused on sustainable graduation of 450 impoverished families comprising two communities on the bank of river Karnaphuli in Mohra area of Kalurghat in the eastern outskirts of Chattogram city. It was launched in February, 2011 by CZM with the financial support of leading local corporate group AK Khan that deployed its Zakat and CSR funds for the cause. Though relatively small-scale, the Jeebika Karnaphuli Mohora project has a number of features that marks it out as different from commonly known microfinance model. It may perhaps be more accurately characterised as a microfinance-plus model with an explicit and far greater emphasis on the issue of sustainability.

Beneficiaries are provided with a five-fold stake in the project: (a) Equity capital in the form of Zakat and CSR allocation for each beneficiary that forms part of a group equity held in a bank account, (b) Access to a revolving fund for micro-loans. The beneficiary group’s pooled equity capital constitutes the revolving fund. Each member has the option of applying for a micro-loan as per the family’s need with the provision for paying a service charge/interest as in the regular micro-finance model (c) Group profit accruing from the interest charged for the micro-loans which accumulate in the group bank account. This secondary income stream is earmarked for equal distribution among members of the group. (d) Social sector support covers education, health, water, sanitation and home gardening. (e) Capacity building supports are given for management, leadership and enterprise skills with the eventual goal of graduation.

Social entrepreneurship

Popularly known as Social Business, a theory developed by Nobel laureate Professor Muhammad Yunus (1940-), is the use of startup companies and other entrepreneurs to develop, fund and implement solutions to social, cultural, or environmental issues. This concept may be applied to a variety of organisations with different sizes, aims, and beliefs. For-profit entrepreneurs typically measure performance using business metrics like profit, revenues and increases in stock prices, but social entrepreneurs are either nonprofits or blend for-profit goals with generating a positive “return to society” and therefore must use different metrics. Social entrepreneurship typically attempts to further broad social, cultural, and environmental goals often associated with the voluntary sector in areas such as poverty alleviation, health care and community development.

Investing in capital markets

Social investors use several strategies to maximise financial return and attempt to maximise social good. These strategies seek to create change by shifting the cost of capital down for sustainable firms and up for the non-sustainable ones. Proponents argue that access to capital is what drives the future direction of development. Negative screening excludes certain securities from investment consideration based on social or environmental criteria. For example, many socially responsible investors screen out tobacco company investments. Despite this impressive growth, it has long been commonly perceived that SRI brings smaller returns than unrestricted investing. So-called “sin stocks”, including purveyors of tobacco, alcohol, gambling and defense contractors, were banned from portfolios on moral or ethical grounds. And shutting out entire industries hurts performance.

Negative screening excludes certain securities from investment consideration based on social or environmental criteria. For example, many socially responsible investors screen out tobacco company investments. Despite this impressive growth, it has long been commonly perceived that SRI brings smaller returns than unrestricted investing. So-called “sin stocks”, including purveyors of tobacco, alcohol, gambling and defense contractors, were banned from portfolios on moral or ethical grounds. And shutting out entire industries hurts performance.

Disinvesting is the act of removing stocks from a portfolio based on mainly ethical, non-financial objections to certain business activities of a corporation. Recently, CalSTRS (California State Teachers’ Retirement System) announced removal of more than $237 million in tobacco holdings from its investment portfolio after six months of financial analysis and deliberations.

Shareholder activism efforts attempt to positively influence corporate behaviour. These efforts include initiating conversations with corporate management on issues of concern, and submitting and voting proxy resolutions. These activities are undertaken with the belief that social investors, working cooperatively, can steer management on a course that will improve financial performance over time and enhance the wellbeing of stockholders, customers, employees, vendors, and communities. Recent movements have also been reported of “investor relations activism”, in which investor relations firms assist groups of shareholder activism in an organised push for change within a corporation; this is done typically by leveraging their enhanced knowledge of the corporation, its management (often via direct relationships), and the securities laws as a whole. Hedge funds are also major activist investors; while some pursue SRI goals and many simply are seeking to maximise fund returns.

Positive investing is the new generation of socially responsible investing. It involves making investments in activities and companies believed to have a positive social impact. Positive investing suggested a broad revamping of the industry’s methodology for driving change through investments. This investment approach allows investors to positively express their values on corporate behavior issues such as social justice and the environment through stock selection – without sacrificing portfolio diversification or long-term performance. Positive screening pushes the idea of sustainability, not just in the narrow environmental or humanitarian sense, but also in the sense of a company’s long-term potential to compete and succeed. In 2015, Morgan Stanley conducted a review of 10,000 funds and concluded “strong sustainability” investments outperformed weak sustainability investments, tackling the idea of a trade-off between positive impact and financial return, while the Global Impact Investing Network’s 2015 report on benchmarks and returns in impact investing in private equity and venture capital found market-rate or market-beating returns were common in impact investments.

Global context

SRI is a global phenomenon. With international scope of business itself, social investors frequently invest in companies with international operations. As international investment products and opportunities have expanded, so have international SRI products. The ranks of social investors are growing throughout developed and developing countries. In 2006, the United Nations Environment Programme launched its Principles for Responsible Investment (PRI) which provides a framework for investors to incorporate environmental, social, and governance (ESG) factors into the investment process. PRI has more than 1,500 signatories managing more than US$60 trillion of assets..

Since 1985, most of major investment organisations have launched ethical and socially responsible funds, although this has led to a great deal of discussion and debate over use of the term “ethical” investment; this is because each of the fund management organisations tends to apply a slightly different approach to running its funds.

In recent years, there has been growth in the market for high social impact investments; this is a style of investing where the businesses receiving investment have social or environmental goals as a primary purpose. UK institutions are also getting more involved in social investing through impact investing funds, with those such as Deutsche Bank and NESTA, alongside other institutions such as Big Issue Invest, which is part of The Big Issue Group.

SRI is a growing force in markets across the world. According to the US SIF Foundation, the responsible investing market in the US increased 486 per cent while the broader US market of professionally managed assets grew 376 per cent between 1995 and 2012. SRI investments are generally demand-side driven. More and more investors are looking for vehicles that are aligned with their values and priorities. In 2014, the total Assets Under Management (AUM) of the 1,278 signatories of the UN Principles for Responsible Investment (PRI), which include asset owners, investment managers and professional service partners, totaled $45 trillion. The SRI niche is not going away.

These investors want to send signals to the market economy regarding the way they want to get things done. For example, the California Public Employees’ Retirement System (CalPERS) actively encourages corporations to improve environmental responsibility, examine executive compensation, and include more women and people of colour in their boards. Investment beliefs adopted by the CalPERS board affect its organisational culture, and in turn, the organisation has intensified its own focus on sustainability. To be a sustainable, prosperous organisation, CalPERS’ long-term liabilities must also be sustainable, because some of them will be on their books for nearly 100 years.

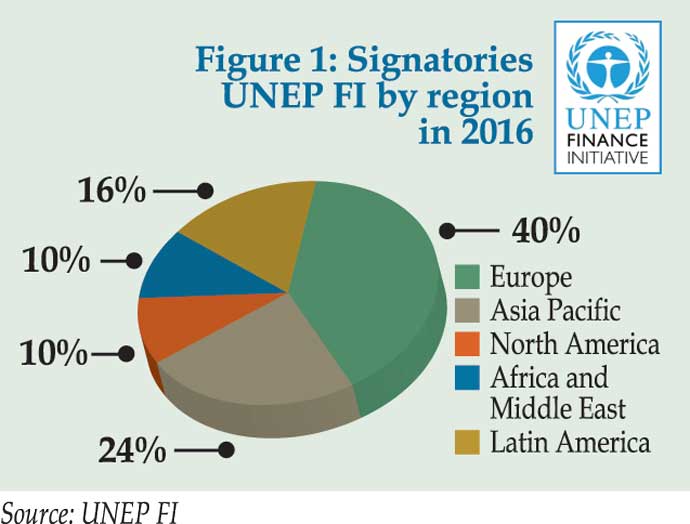

The Asian scene The value of world SRI market is estimated at $21.4 billion, from which €11.05 billion falls on the European market (Global Sustainable Investment Review GSIR, 2014). Although Europe is a global leader, similar developing markets the ones of the US, Canada and Australia, are gaining more popularity. Asian countries became a vital part of the market too. Both world economic powers like China and Japan, and also South Korea, Singapore and Malaysia are joining this global trend. Nowadays the socially responsible investment seems to be an investment direction of a modern, post-crisis international financial market.

The value of world SRI market is estimated at $21.4 billion, from which €11.05 billion falls on the European market (Global Sustainable Investment Review GSIR, 2014). Although Europe is a global leader, similar developing markets the ones of the US, Canada and Australia, are gaining more popularity. Asian countries became a vital part of the market too. Both world economic powers like China and Japan, and also South Korea, Singapore and Malaysia are joining this global trend. Nowadays the socially responsible investment seems to be an investment direction of a modern, post-crisis international financial market.

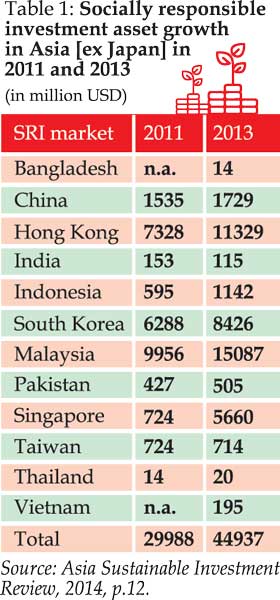

Sustainable investment assets in Asia, still comprising only a small portion of world total professionally managed assets, stand at $53 billion in 2015, an increase from the $40 billion reached at the beginning of 2012. The collected data include 12 SRI markets, such us Bangladesh, China, Hong Kong, India, Indonesia, Malaysia, Pakistan, Singapore, South Korea, Taiwan, Thailand, and Vietnam (table 1). The three largest Asian markets for socially responsible investments, by asset size, are Malaysia, Hong Kong and South Korea. The fastest growing are Indonesia and Singapore markets. According to historic maturity, the most developed market in the Asia region is Japan. Innovational products concern ESG policies like impact investing, bonds and green real estate are gaining popularity in Japan.

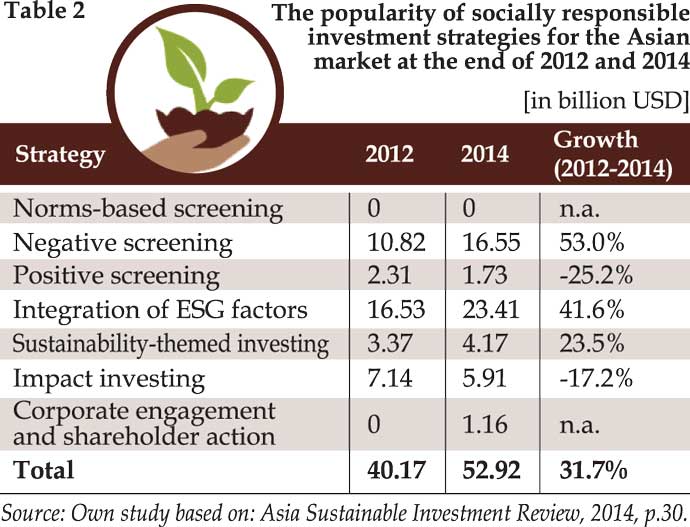

In Asia region in 2016, it is observed, the growth in the number of sustainability reporting instruments is about 75 per cent since 2013. This initiative came more often from financial market or industry regulators than governments. Increased attention applied to nonfinancial activities of companies and transparency of reports influence development of socially responsible investment market in Asia. The key participants in this market are institutional investors, asset managers, individual investors and investment banks.  The SRI fund market is strongly affected by religious attitude. Islamic funds are the major contributor to sustainable investment assets in Asia, mostly in Malaysia and Indonesia, where government policies support development of the Islamic fund market. Another important form of socially responsible investment in Asia is impact investing and community investment. This investments approach concentrate on financial and social inclusion. The capital from investors is directed to microfinance programmes.

The SRI fund market is strongly affected by religious attitude. Islamic funds are the major contributor to sustainable investment assets in Asia, mostly in Malaysia and Indonesia, where government policies support development of the Islamic fund market. Another important form of socially responsible investment in Asia is impact investing and community investment. This investments approach concentrate on financial and social inclusion. The capital from investors is directed to microfinance programmes.

Microfinance offers access to capital to people of low income, who have been excluded from formal banking sources or enterprises on the early stage. Microfinance programmes provide access to credit, equity and basic banking products. The most well-known, and at the same time, most developed product is a microcredit. Microcredit provides financial capital for the poor or entrepreneurs who toil in informal, poverty-ridden sectors in developing country economies. The motherland of microcredit is Asia exactly. The best known examples coming from the Grameen Bank of Bangladesh, which was established by M Yunus.

Asia Stock Exchange is playing significant role in developing regional socially responsible investment markets. One of the targeted methods is enhancing ESG reporting by companies listed on stock exchanges. Many initiatives are taken in this field. The Shenzhen Stock Exchange (SZSE) in 2006 and the Shanghai Stock Exchange (SSE) in 2008 have introduced guidelines for listed companies. The important driver of the SRI market in Asia, therefore, will be environmental issues relating to climate change, energy and resource scarcity. In 2016, during China’s leadership of the G20, according to research results taken by Green Finance Study Group (GFSG), China summed up its needs of around $460 billion a year to finance green investment plan (G20 Green finance).

Sustainability of environmental, social & governance factors

With issues ranging from income and wealth inequality to climate change, expect these trends to only continue. Sustainability strategies continue to add financial value for companies and their shareholders.

Examples of environmental, social and governance (ESG) factors are numerous and ever-shifting. They include:

Environmental: Climate change; greenhouse gas (GHG) emissions; depletion of resources including water; waste and pollution; deforestation

Social: Working conditions including slavery and child labour; local communities including indigenous communities; conflict; health and safety; employee relations and diversity

Governance: Executive pay; bribery and corruption; political lobbying and donation; board diversity and structure; tax strategy

One more concern remains – the SRI legal and its environmental challenges and ethical investment – since SRI as this financing movement is more commonly known today, increasingly downplays ethics. Traditionally it has championed an explicit ethical agenda; these investors have addressed social or environmental concerns not for any financial reward, but for moral desire and responsibility to improve the world. The renaissance of SRI in the mainstream financial markets since the late 1990s has problematically, somehow rather, disavowed this ethical posture. Responsible investors increasingly pitch their case for taking social or environmental issues into account on business grounds, on the assumption that SRI will make them prosperous, rather than merely virtuous.

While business case SRI is becoming popular, it risks perpetuating business-as-usual and reducing the SRI movement’s capacity to leverage lasting change for environmental sustainability. Environmental problems have become the most important SRI cause today, yet it is doubtful whether present forms of SRI will make a significant difference to their resolution. Ethical investment to promote sustainability should no longer be a discretionary option for financiers, to follow only if there is a compelling business case. In a world that faces grave ecological problems, the financial sector must shoulder some of the responsibilities to shift economic activity to sustainable development. UN Sustainable Development Goal (SDG) numbers Seven, Eight, Twelve, and Thirteen have strongly advocated this paradigm shift.

Dr Muhammad Abdul Mazid is a former Secretary to the government of Bangladesh and led National Board of Revenue, Chittagong Stock Exchange and South Asian Federation of Exchanges as Chairman.

mazid.muhammad@gmail.com