Stock markets and economic growth performance

Mirza Azizul Islam | Wednesday, 25 June 2014

The recent developments in the stock markets of Bangladesh have given rise to considerable divergence of views about its role in economic development, more specifically economic growth, of the country. Some policy makers have termed the market as "wicked" and gambling casino. On the other hand, officials of the exchanges have been trying hard to project the markets as a potentially major contributor to investment and hence to growth. In this backdrop, the objectives of this article are to (i) provide a brief overview of a priori arguments which lend support to the view that stock markets promote economic growth and related concerns, (ii) give an assessment of the present state of development, (iii) analyse the causes of the recent crash and (iv) provide some suggestions regarding how the stock markets can be revived so as to play their potential role as a contributor to investment and growth.

A PRIORI ARGUMENTS AND EVIDENCE

Potentially positive impact on growth: (i) A developed stock market may yield higher returns on savings. The preferences of savers may shift away from holding their savings in the form of cash or fixed income-yielding assets compared to which higher returns can be usually obtained from stocks. Thus the stock markets create an opportunity for the savers to diversify their portfolio and associated higher returns may encourage higher level of savings.

ii) Irrespective of the level, stock markets enable greater mobilisation of savings for investment. These supplement other institutional arrangements to mobilise savings such as banks.

(iii) Stock markets lower the cost of raising finance capital for investment. This can increase the level of investment and adoption as well as development of improved technologies to accelerate growth.

(iv) Stock markets permit substitution of equity finance for debt finances. The vulnerability of firms to fluctuations in earnings and interest rates is thus reduced with beneficial impact on investment.

(v) The intensity of adverse selection effect sometimes associated with financing by banks can be reduced by stock markets. If the prevailing interest rates are high, safe borrowers are discouraged from seeking credit. On the other hand, the banks may be tempted to finance projects which promise potentially high returns but are fraught with higher risks. The resultant defaults in some cases may encourage banks to shun new borrowers.

(vi) The stock holders have the incentive to acquire information about the operational efficiency of the firms the stocks of which they have bought. If necessary, they can also effect changes in management leading to better corporate governance and improved use of resources.

(vii) Regulatory requirements of listed companies generally encourage adoption of improved accounting and reporting standards. These can lead to greater transparency and efficiency.

(viii) Finally, stock markets can attract foreign investment which can help bridge the well-known dual constraints faced by developing countries, namely, saving-investment gap and foreign exchange gap.

Contrary views: (i) A higher return on savings does not necessarily guarantee higher savings. "The level of savings is subject to two countervailing effects. The decision of the household on how much to save depends on its preference with regard to present versus future consumption. The higher return induces the household to give up present consumption for higher consumption in the future: the household's members save more. This is called the substitution effect. However, the higher return on savings implies that the household needs to save less to obtain the same level of future consumption as before. In a sense, the higher rate makes the household wealthier, so it wants to consume more today. This is called the income effect, which leads to lower saving rate. Empirical studies have not provided a conclusive answer as to which effect dominates; that may vary across the population" (Catalyst Institute, undated, p.6)

(ii) There is a "free rider" problem. With many investors in a company very few may be willing to incur the cost of acquiring information relating to the operational efficiency of the company. The problem of information asymmetry between the managers and the shareholders may not be thus addressed and the supposed benefits of the improved corporate governance not realised.

(iii) In presence of the above scenario, investment decisions in the stock market may be influenced by movements in the prices. Pricing inefficiency may lead to a high degree of volatility resulting in speculative bubble and eventual bust with irrational change in market sentiment.

(iv) The bust may cause fall in other asset prices, create problems for banks with exposure to stock market, generate negative effects on confidence and thereby reduce consumption and investment and hence growth.

(v) An economic system based on equity system may discourage longer-form, somewhat riskier investment as firms become preoccupied with short-term financial returns for shareholders (Feldman and Kumar, 1995).

EMPIRICAL EVIDENCE

The above discussion suggests that the impact of stock market on growth in the final analysis is essentially an empirical question. There have been many studies which examine the link between the developments of the financial sector generally and economic growth. But studies which investigate the relationship between the development stock market specifically and growth are rather few.

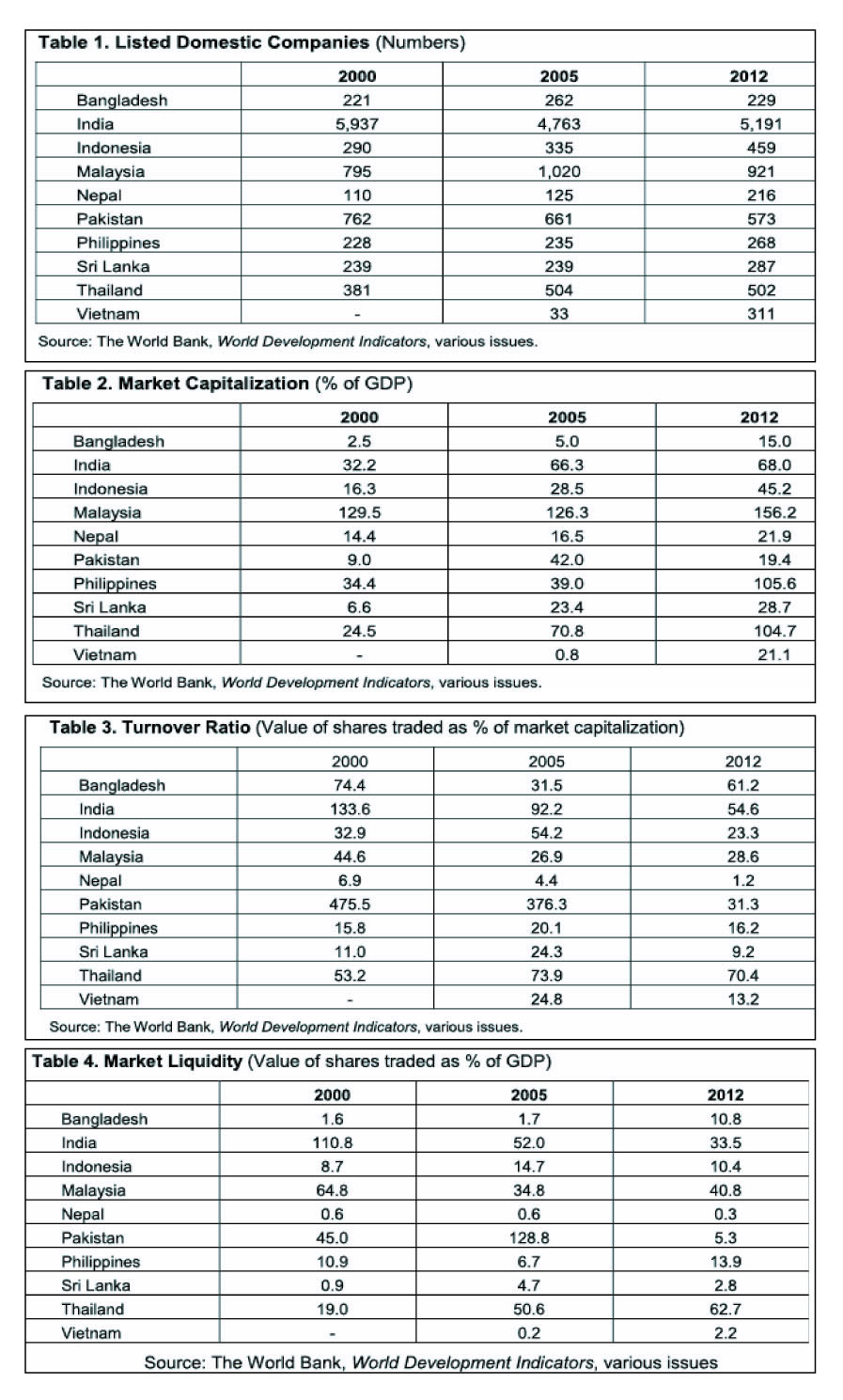

There can be various measures to assess stock market development. Those include the number of companies listed on the stock exchange (Table 1), market capitalisation as proportion of gross domestic product (GDP) (Table 2), turnover ratio i.e. Value of shares traded as proportion of market capitalisation (Table 3), and market liquidity i.e. Value of shares traded as proportion of GDP (Table 4).

Atje and Jovanovic (1993) examined a sample of forty industrial and developing countries and found that the higher the ratio of stock market trades to GDP, the higher the growth of per capita income. A significantly positive relationship between initial stock market activity and subsequent growth was found in an extensive study by Levine and Zervos (1995). This finding is supported by another study (Filer, et al,1999). These authors also find that turnover ratio Granger-causes growth, but only for high and low income countries, but not for middle income countries and that there is no evidence that a change in the number of listed companies is linked to differing rates of economic growth. Mohtadi and Agarwal (undated), based on analysis of time series and cross-section data of 21 centuries for the period 1977-1997 find that stock market development has a positive impact on growth even after controlling for lagged growth, initial level of GDP (Gross Domestic Product) , foreign direct investment, domestic investment and secondary school-level enrolment. The positive influence is exerted both by turnover ratio and market capitalisation ratio.

This article is adapted from a presentation made by Mirza Azizul Islam, former finance adviser to the last caretaker government and also a former chairman of the Securities and Exchange Commission, at the conference of Bangladesh Economists' Forum held in Dhaka on June 21 & 22, 2014