T-bonds trading on bourses: Supply runs dry against high demand

BABUL BARMAN | Wednesday, 1 March 2023

Although trading of Treasury bonds began on the country's stock exchanges four months ago, transactions are yet to gain momentum mainly due to supply shortage.

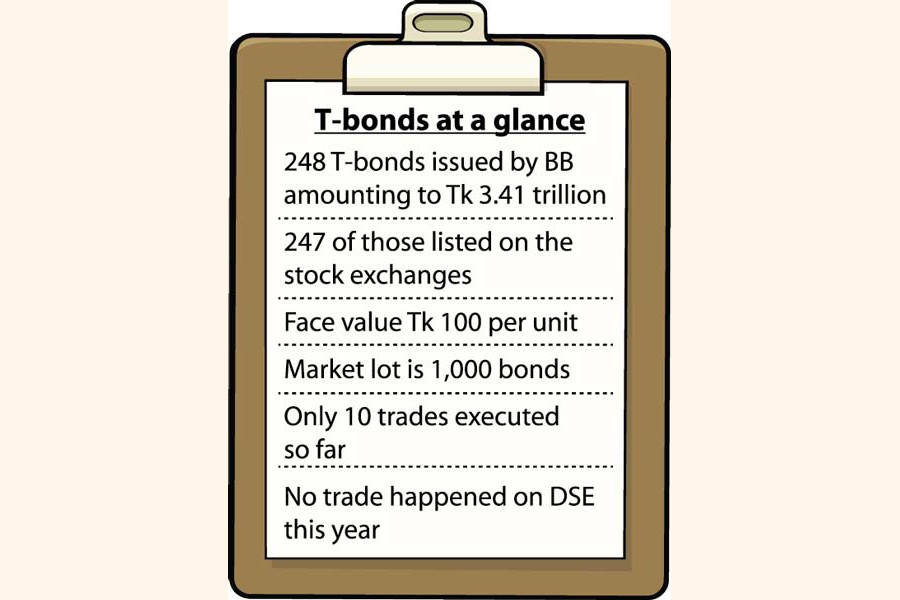

Only 10 trades amounting to Tk 5.99 million of T-bonds have taken place since the debut trading in October last year.

Treasury bonds are a good investment opportunity for safe and fixed interest income received semiannually until the maturity. The government debt securities help investors offset the risk of equity price volatility.

General investors are unable to buy T-bonds since banks and other financial institutions hold almost all of those and are reluctant to sell the bonds on the stock exchanges, market insiders say.

M Shaifur Rahman Mazumdar, managing director (Acting) of the Dhaka Stock Exchange said institutions usually purchase government securities for long term, not to sell them before maturity.

"So, a majority of the securities will ultimately be held by institutions, and only a few would be traded in the market."

Mr Mazumdar, however, added that the Dhaka bourse has been trying to persuade the institutional investors to improve supply of T-bonds to the secondary market.

T-bonds in Bangladesh

It is a debt security through which the government borrows for more than a year. The Bangladesh Bank, on behalf of the government, issues such bonds to finance the budget deficits.

There are 248 Treasury bonds now, with tenures ranging from 2 to 20 years. They pay at the coupon rate of 2-15 per cent annually against the face value of Tk 100 each bond.

The longer the tenure the higher the interest rate is.

For example, at the end of November 2022, the yield on 2-year T-bonds was 7.49 per cent while the rates were 7.81 per cent for 5-year bonds, 8.25 per cent for 10-year bonds, 8.67 per cent for 15-year bonds and 8.72 per cent for 20-year bonds.

A large number of T-bonds yield more than what bank deposits return nowadays. This makes such bonds a lucrative and safe investment tool.

The government owes over Tk 3.41 trillion to the outstanding treasury bond holders, mostly financial institutions.

Mohammad Rezaul Karim, spokesperson and executive director of the Bangladesh Securities and Exchange Commission (BSEC), said the commission is working on the supply side as the demand is already there.

"The commission is working to persuade the institutions to offload their saleable bonds on the secondary market," Mr Karim said.

What comes in the way?

Individual investors do not get access to T-bonds in the stock market since trading of these securities is still mostly happening on the central bank's platform, said Mir Ariful Islam, managing director of Sandhani Asset Management.

Regulated by the Bangladesh Bank, T-bonds exchange hands through beneficiary participant identification (BPID) accounts. Primary Dealers (PDs) place bids in auctions conducted by the BB, and other institutions purchase the bonds from PDs through secondary trading.

The T-bonds should now be available for retail investors as well after the much-hyped debut trading in the stock market last year.

But these debt securities could only be traded through BO (beneficiary owner's) accounts on the bourses. The transferring of the bond units to BO accounts is yet to become smooth as several parties are involved in here.

Recently, the securities regulator has asked market intermediaries -- merchant bankers, portfolio managers, asset managers, stock-dealers, and mutual funds -- to invest at least 1 per cent of their portfolios in listed Treasury bonds in order to diversify their portfolios and bring down risk.

Banks are reluctant to sell Treasury bonds through the stock exchanges because of the existing 2 per cent circuit breaker. Bankers argue that the institutions would feel encouraged to sell the instruments if they see good enough capital gains.

"If the price is dictated, no one will want to sell Treasury bonds. The problem is that the bank cannot set the offering price," said a Treasury head of a bank, wishing not to be named.

Dr. Suborna Barua, associate professor of the international business department at the University of Dhaka, dug deeper into the matter and explains why the stock market has failed to boost trading of T-bonds.

Usually, T-bonds are held by primary dealer (PD) banks until maturity. If the interest rates fall, the prices of the debt securities rise, prompting the investors to trade those in the secondary market for capital gains, said Mr Barua.

He suggested building a special business development team to work with market intermediaries for bonds trading in the stock market. At the same time, he said, the regulators should make certain level of investment in T-bonds mandatory for stock dealers.

While the supply side is yet to improve, the securities regulator has been ruminating about how to increase the demand.

It is in talks with the National Board of Revenue to introduce supportive tax policies.

Just like zero-coupon bonds, the income from all sorts of bonds should be free of tax for individual investors and that would help increase their appetite for bonds, said the DSE managing director.

The coupon rates sway with the demand in the market.

"Trading of T-bonds is still undergoing trial. Once the market is fully ready, trading will gain momentum," said the DSE official.

babulfexpress@gmail.com