The current account and depreciation

M A Taslim | Wednesday, 10 April 2019

When the current account is in the news it is unlikely to be good news. It usually attracts the attention of the media when it is in a large deficit. This is what is lately happening to the current account of the country. A surge in import in 2017-18 blew it out to nearly US$10 billion. This is more than seven times the deficit of the previous year. This fiscal year the current account is likely to be lower, but substantial at about 8.0 billion dollars. The deficits are not about to go away soon.

The current account deficit represents the magnitude of the spread between the domestic demand for foreign exchange and the supply of it, that is, the excess demand for foreign exchange, in current transactions. If the deficit is not completely offset by voluntary capital account transactions, it may impart an upward pressure on the price of the foreign currency, commonly known as the foreign exchange rate. A depreciation of the domestic currency, which implies an increase in the price of the foreign currency, helps to reduce the demand for the latter as well as increase its supply, thereby reducing the current account deficit. Hence, the occurrence of high current account deficits is frequently followed by suggestions for depreciation to reduce the deficits.

However, this relationship is neither immediate nor certain. An immediate result of a depreciation is frequently a worsening of the deficit. Trade transactions of a country like Bangladesh are contracted in foreign currency (mostly US dollar). These cannot be changed until the existing contracts expire. This means that the domestic businesses end up paying more in domestic currency for the imports. This induces them to reduce imports, but only with a time lag.

The exporters receive higher prices for their products. But export volume is much less than the volume of imports. Consequently the higher receipts for exports do not compensate for the higher payments for imports. Thus the deficit may widen initially. After a while imports tend to decline and exports increase thereby improving the trade balance provided the import and export elasticities are right. The worsening of the trade balance after a depreciation of the domestic currency and improving gradually thereafter is stylised as the J-curve effect in trade economics.

A large credit entry in our balance of payments is secondary income which comprises mostly workers' remittances. There does not seem to be a stable relationship between remittances and the exchange rate, it seems to be related more to the number of people working overseas and the incomes earned. Thus the impact of a depreciation on the current account will be determined largely by its impact on the trade balance, which may be subject to the J-curve effect.

Nearly nine-tenths of our imports comprise producer goods such as raw materials, intermediate goods and capital machinery. Thus an increase in the taka costs of these imported goods immediately raises the production costs of almost all goods and services. Furthermore, Bangladesh being a small open economy, the domestic prices of all tradable goods are linked to the international prices through the Law of One Price. Any depreciation will lead to a proportionate increase in the price of tradable goods quickly because of this link. The price of non-tradable goods will also respond to the extent their cost of production increases because some of their inputs are imported goods. There seems to be little doubt that the prices will rise soon after a depreciation of the taka.

The development aspirations of a developing country like Bangladesh often imply that its import needs far exceed export earnings and other receipts. Since most of the imports comprise essential goods (food, oil and inputs in production), it is difficult to reduce usage greatly when their prices rise after a depreciation. These countries produce a very limited range of goods that can be exported, and their productive capacity is also limited. Thus, depreciation may not increase the volume of exports greatly.

Domestic producers often operate through buying houses which have disproportionate market power over them. The benefits of depreciation do not always accrue fully to them as the buying houses may reduce the foreign exchange prices of the goods after a depreciation. For these reasons depreciation has limited power to substantially improve the current account. Often it worsens the situation. This can be illustrated with the history of the exchange rate and the current account of the country. Since most of the foreign transactions are done through US dollar, the taka-dollar exchange rate can be regarded as the appropriate exchange rate. Between 1973-74 and 1989-90 the taka-dollar exchange rate depreciated more than 400 per cent, and yet the balance of payments worsened nearly 1000 per cent. Between 1995-96 and 2000-01 the exchange rate declined by 32 per cent, but the deficit widened by 53 per cent. The only period when the expected relationship held was the period 2001-02 to 2015-16. The currency depreciated gradually by 34 per cent and the current account surplus increased. However, the depreciation of the taka during the last two years saw the largest deficit ever. In sum, what these numbers suggest is that the influence of the exchange rate on the current account is weak, and depreciation alone cannot be trusted to improve the current account. Perhaps the most one can say is the counterfactual that things could be worse without the depreciation.

This can be illustrated with the history of the exchange rate and the current account of the country. Since most of the foreign transactions are done through US dollar, the taka-dollar exchange rate can be regarded as the appropriate exchange rate. Between 1973-74 and 1989-90 the taka-dollar exchange rate depreciated more than 400 per cent, and yet the balance of payments worsened nearly 1000 per cent. Between 1995-96 and 2000-01 the exchange rate declined by 32 per cent, but the deficit widened by 53 per cent. The only period when the expected relationship held was the period 2001-02 to 2015-16. The currency depreciated gradually by 34 per cent and the current account surplus increased. However, the depreciation of the taka during the last two years saw the largest deficit ever. In sum, what these numbers suggest is that the influence of the exchange rate on the current account is weak, and depreciation alone cannot be trusted to improve the current account. Perhaps the most one can say is the counterfactual that things could be worse without the depreciation.

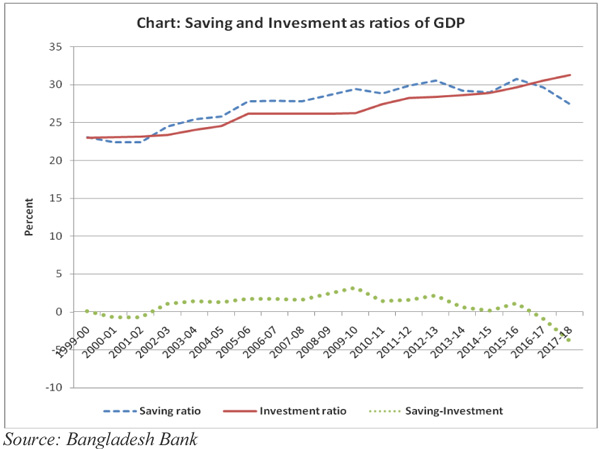

The national income account identity points at the macro factors that directly determine the current account. One representation of it is: Current Account Balance National Saving Domestic Investment. This identity asserts that no matter what, the current account balance will be in surplus if national saving is greater than domestic investment. Therefore, it is useful to examine the profile of saving and investment to understand the current account.

Bangladesh Bank data show that from 2001-02 to 2015-16 the saving of Bangladesh as a ratio of GDP (gross domestic product) exceeded the investment ratio every year except one implying that the country had a balance of payments surplus all these years. This is shown in the chart. These surpluses helped to build up a large stock of international reserves over this period. The saving ratio reached a peak of 30.5 per cent in 2012-13 and thenceforth gradually declined to 27.4 per cent in 2017-18. The investment ratio on the other hand sustained its slow increase and eventually exceeded the saving ratio by 0.9 per cent in 2016-17. The gap increased further to 3.8 per cent in 2017-18. These then were also the magnitudes of the current account deficits as suggested by the identity above. (Because of errors of measurement the relationship is not exact.) These deficits, which show the extent of the excess demand for foreign exchange, put pressure on the exchange rate to depreciate. But the depreciation obviously did not always reduce the deficits.

There are no estimates of private saving ratios. However, the large reduction in the private consumption ratio might suggest an increase in the private saving ratio over time assuming that private income relative to national income did not fall. The government consumption ratio on the other hand rose considerably, but its revenues did not increase much. This suggests that its saving ratio fell. A large source of national saving, remittances, also declined; the remittance-GDP ratio declined steadily from 9.5 per cent in 2009-10 to only 5.5 per cent in 2017-18. It seems reasonable to assume that the country's saving ratio declined mainly because of the decline in the government saving ratio and remittances. None of these respond much to depreciation.

Private investment ratio remained fairly stable during the last one decade, but government investment ratio steadily increased from 4.3 per cent to 7.3 per cent. Hence, the increase in the country's investment ratio could be attributed largely to the increase in government investment. The contribution of the private sector was small.

The excess of the country's investment over saving, that is, the current account deficit, was then caused mainly by both an increase in government investment and a fall in saving as well as a slump in remittances. An improvement in the deficit could be achieved by either a reduction in government investment or an increase in saving. The same objective could also be achieved by a reduction in private investment (through perhaps crowding out) or an increase in private saving. An increase in remittances will also prevent the necessity to reduce government or private spending in order to improve the current account balance.

Could a depreciation of the taka nudge the government to reduce its investment, which would require a reduction in spending on its much hyped mega projects, or to raise its saving effort that would inevitably involve raising taxes? These are unlikely since the government investment projects were well-thought-out and it is committed to their full implementation, while its effort to raise taxes hardly bore fruit in recent years. The government borrowed overseas to finance many of these projects in order to avoid, at least temporarily, higher interest rates and crowding out of the private sector. A depreciation could therefore work only by reducing private spending for both consumption and investment through price inflation. The crowding out of private absorption would release resources, which if adequate to offset the higher spending of the government could improve the current account balance.

However, if this were to transpire the private sector would be much aggrieved as it would bear the burden of the government expansion. This may not be a good political move for the government. Since the deficits have blown out, a very large depreciation would be necessary for achieving this type of adjustment. It is doubtful that the government will have the stomach for a large depreciation that could release the inflation genie and destabilise the economy. It would find it more judicious to defer the administration of any bitter antidote to reduce the deficit. It can keep a lid on the current difficulties temporarily by borrowing overseas to finance the deficits.

The author is an economist and currently an adjunct faculty at East West University. m_a_taslim@yahoo.com