The dos and don\\\'ts of agent banking

Shariful Islam Bhuiyan | Sunday, 27 April 2014

Agent banking is now a buzzword in the banking industry. Its importance is immense in paving the way for financial inclusion. But, many of us, including bankers, still do not have a clear perception of agent banking, its services, risks and responsibility and other regulatory issues.

Agent banking was first introduced in Brazil in 1999. Then it was introduced in other countries of Latin America, namely Peru (2005), Colombia (2006), Bolivia (2006), Ecuador (2008), Venezuela (2009), Mexico (2009) and Argentina (2010). Other countries in the world adopting this model are Pakistan, the Philippines, Kenya, South Africa, Uganda, India, etc.

According to a circular issued by the Bangladesh Bank (BB) on December 09 last, "Agent Banking means providing limited-scale banking and financial services to the underserved population through engaged agents under a valid agreement, rather than a teller/cashier. It is the owner of an outlet who conducts banking transactions on behalf of a bank.' Agent Banking offers banking services on a limited scale to semi-urban and rural people through a person or entity authorised under a valid agreement by a scheduled bank. The authorised persons or entities or their employees provide services to customers during the usual business hours of scheduled banks on their own premises rather than on any bank premises or at any ATM booth.

AGENT BANKING SERVICES: The agent banking services are: i. small-value cash deposit and withdrawal, ii. disbursement of inward foreign remittance, iii. disbursement of small-value loan and recovery, iv. utility bill payment, v. cash payment under the social safety net programme of the government, vi. fund transfer, vii. balance inquiry, viii. collection and processing of forms and documents regarding account opening, loan application, debit and credit card application, ix. receiving clearing cheques, and x. post-sanction monitoring of loans and advances.

But banking agents are not allowed to provide services like: i. To give final approval of account opening, ii. To issue bank card or cheque books, iii. Encashment of cheques, and iv. dealing in foreign currency.

As per the BB circular, eligible banking agents are: i. non-government organisations (NGOs) and micro-finance institutions (MFIs), ii. cooperative societies formed under the Cooperative Society Act, 2001, iii. post offices, iv. registered courier and mailing services, v. registered companies, vi. agents of mobile network operators, vii. offices of rural and urban local government, viii. union information and service centres, ix. educated individuals (who are tech-savvy, agents of insurance companies, pharmacies, chain shops, petrol pumps, gas stations).

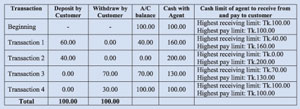

An agent must maintain an account with their principal bank. Every transaction has an impact on the agent's account with the bank. The agent must deposit a certain amount of money (the highest limit is Tk 1.00 million) with a bank in advance as security money before launching the service. Let's cite an example. An agent has deposited Tk 100.00 to his bank account with his principal bank and started operation of agent banking with a hard cash Tk 100.00.

The following chart presents the transactions:

So, both cash receipt and payment are restricted by a pre-determined limit.

As per a circular issued on March 24 last, the highest balance of an agent's account with the principal bank will be Tk 1.0 million (10 lakh). Customers should not be charged directly by the agent. Banks should pay reasonable fees and commissions to their agents. However, banks may charge commission, fee, charge, etc. as applicable.

INCLUSIVE GROWTH AND SOCIAL INCLUSION: Agent banking can pave the way for inclusive growth and social inclusion the ways highlighted below:

1. Reduction of social cost: Customers do not need to pay extra or take the trouble of travelling to a bank branch far away by bus or boat for paying a bill or withdrawing money. Customers can do it easily at the local agent bank. Many such activities reduce the social cost.

2. Targeting new customer segment: Low income people in our country do not feel easy to visit luxurious bank premises as they have the perception that such services involve high and hidden costs. But agents are locally known and trusted. So the segment can be targeted.

3. Expanding outreach: There are many areas in our country where the economic condition of the people is not good and profits from those areas are not that much that can offset a branch's fixed and operational expenditure. Banks may thrive by covering these areas through engaging local agents as agents do not have to incur any significant amount of cost for rendering the services. In Brazil, Banco Bradesco partnered with their national post office as agents to cover such new areas.

4. Marketing and recommendation: Agents are locally-known community leaders and trusted. Their reference and marketing can boost assets and liability of a bank. Their reference is more effective than a third party deployed for marketing.

5. Credit recovery: This is a very sensitive area. Local agents can play a great role in loan repayment. But, they should not force anyone to repay overdue loan instalments, which may tarnish their image in the community and dissuade the people from going to the agent banks. However, as the local agents are community leaders and socially accepted, they can play a persuasive role in loan repayment.

6. Customer care: Agents can help fill in account opening forms in their remote areas. They may inform the people of the benefit of depositing money in a bank account rather than keeping hard cash at home. People in remote areas may hesitate to visit branch premises or seek any information from customer care. But, they will feel homely when they visit the local agents and the local agents also can help them accordingly.

DRAWBACKS: However, there are some drawbacks and also the way out:

1. Risks of theft or robbery: There are risks that incidents like theft or robbery can take place on an agent bank's premises. So, before picking an agent, banks need to examine and consider the security of the place. Banks should also consider the rate of theft or robbery in an area before selecting an agent. If needed, banks can also arrange an insurance coverage.

2. Reluctance to technology: People in remote and semi-urban areas are usually reluctant to use technology. They are not habituated to use any card or point of sale (POS) device. Banks may draw up any effective promotional plan to reduce this reluctance. Banks may arrange demonstration of POS use in the localities.

3. Both deposit and withdrawal need to go simultaneously: An agent maintains a Current Deposit account with a principal bank and deposit a certain amount of money for the security purpose and this is the highest limit for an agent to accept deposits from customers. If deposits by customers touch the limit of the agent's deposit, any new deposit from any customer is not allowed until a customer withdraws some money. Banks may persuade the agents to deposit an additional amount of money to increase the limit for collection of deposits from customers to avert any such problem.

4. Fraudulence by agents: Agents may take money and tell the customers that deposit has been credited to his/her account, but there is no automated printed receipt because of any mechanical fault. So banks may have written and pictorial instructions and those should be placed at visible places inside any agent bank to make customers aware that no transaction is completed without an automated printed receipt. Such activities can bar any agent or their employees from any such fraudulent activities. Banks may provide a customer care contact number at the agent bank's premises to help the customers get information or lodge any complain.

5. Conflict of interest with similar service providers: As per the Bangladesh Bank circulars, NGOs, micro-finance institutions, cooperative societies, etc. can act as agents on behalf of a bank. Since these organisations are involved in a similar kind of activities in remote areas, there may arise a conflict of interest. Customers may get confused about the service provider. They may think the service is rendered by an MFI (microfinance institution), when the MFI is acting as an agent, indeed. As per a circular of the Bangladesh Bank, an agent bank's premises should be marked with the principal bank's name, logo, colour etc. so that the customer can understand easily which bank the agent belongs to.

6. Agents' indifference: Post offices, registered companies, agents of mobile networks and insurance companies, pharmacies, chain shops, etc can act as agents. So, each and every agent has their own business to do. So, the agents may be less attentive to banking services. Banks should motivate the agents. Banks may go for commission-based business-the more you do business, the more you earn commission. Banks may give proper training to agents or agents' employees as to how to handle IT-related issues and deal with customers effectively and efficiently. More importantly, the agents should be convinced that alongside the financial services the sale of other products at the agents' stores will also peak up. Many stores in Brazil saw 30 per cent increase in sales because of the traffic generated to the store by their newly-offered banking services.

7. Selection of improper agent: Sometimes the agents may not be locally trusted. History of business, personal reputation and leadership of the store owner concerned within the community may not be checked before selecting an agent. Credit history, police record, cash handling efficiency, control etc may be considered as minor criteria for selecting an agent. Banks may never know that if these issues are overlooked or not taken seriously, these agents will tarnish the brand image of the bank knowingly or unknowingly. So, before selecting an agent these issues claim to be prioritised.

8. Selection of improper store: The size, location and cleanliness of an agent bank premises may not be convenient for the customers. Banks may not consider the type of the agent bank's existing business. Proper space at an agent's store or shop deserves consideration for branding a bank. This aspect should not be ignored.

VISION AND PROSPECTS: Agent banking can add an impetus to financial inclusion, if the BB along with commercial banks can unleash the power of agent banking properly. The BB should have a vision regarding this. The BB may encourage banks to go for agent banking. Commercial banks, on the other hand, will have to plan and execute agent banking. But, this is not that much easy as it appears to be. Banks may think about selection of right places, stores, agents and POS. But these are just the beginning. There is a lot more to do. A crucial one is strategic. Banks need to have their vision, mission, goals and objectives, which must fulfill the need and requirement of their new customer base. If not, this is going to be a failed venture, for sure!

Then banks will have to chalk out a 5/10-year strategic plan and a short-term plan as well for establishing an agent banking network. A dedicated team/department should be formed comprising IT experts, financial analysts and marketers headed by high officials of banks. Few indicators i.e. business transaction, unbanked population, checking existence of banks' branches, inward foreign remittance, etc. need to be analysed before deploying an agent in a new area. Most importantly, a bank will have to establish its own marketing and sales team. This will be sheer imprudent to depend solely on agents for marketing a new concept in remote areas, as it is an IT-based financial service. In a BB circular, marketing has also been given priority. According to the BB circular, marketing communication can be made in the local language with the people in remote areas. In addition, banks may arrange drama shows with the help of projectors in villages and market places. Then the people will have a clear perception of the necessity, benefits and the security aspect of agent banking. Banks may distribute leaflets showing the steps of how to use POS alongside other benefits. Banks should not go for TV commercials (TVCs) or a big marketing campaign at the very beginning of establishing an agent banking network. But it may be different based on the vision of a bank. The bank should focus on proper training, development and motivation of agents.

Another very important aspect of agent banking is financial inclusion. Studies have proved that financial inclusion is a tool for inclusive economic growth and poverty alleviation. But financial exclusion, that means the lack of access to financial services, limits opportunities for enterprise development and employment and imposes a premium on the cost of basic services. Financial exclusion thus makes it difficult to reduce inequalities and alleviate poverty. According to the Working Paper Series: WP1101 of the BB Research Department, the number of bank branches per 1000 square kilometres increased from 44.24 in 2005 to 53.34 in 2010. This is a very slow growth because of the high cost of setting up a branch. But agent banking that involves low costs can help enhance the financial inclusion. Moreover, customers including the poor and illiterate people will find it easy to enjoy services from the agents.

The goal of agent banking is not mere making profit. There is a far greater cause. It is an initiative that helps social inclusion, national integration and consolidation of citizenship. Implementation of agent banking is an art even within the stringent rules and regulations of the BB. It is high time to popularise agent banking to serve the cause of social inclusion.

The writer is Senior Officer of Bank Asia Limited, MCB Dilkusha Branch. sharif_mkt.du@yahoo.com