The state of global economy

Hasnat Abdul Hye | Tuesday, 25 November 2025

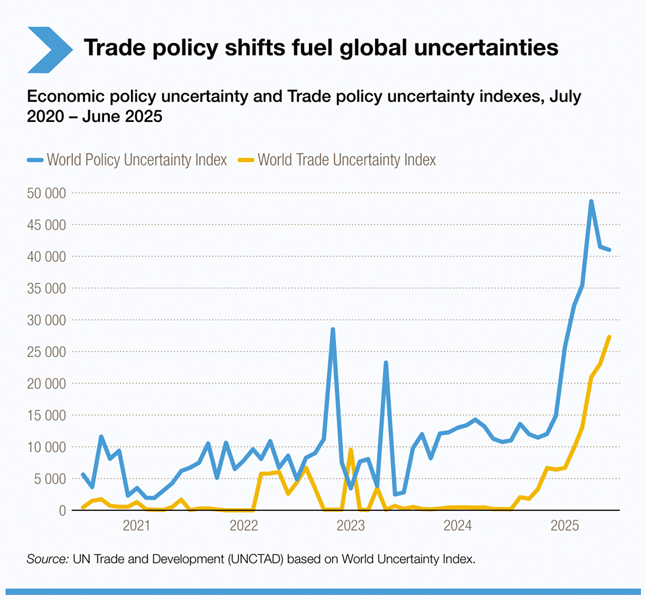

The world economy has been subjected to destiabilisation and uncertainty for quite some time. Factors contributing to this unforeseen situation are: (a) Lingering effects of supply chain disruptions caused by the 2020 Covid pandemic; (b) the Russia-Ukraine war adding to the already frayed supply chains, particularly for food, fertiliser, gas and oil; and (c) the wide-ranging tariff slapped on imports of almost all countries by America under Trump administration. Except the first, the rest have been the result of deliberate policies of two superpowers bent on achieving supremacy in spheres of geopolitics and global economy. As a result, all countries are now per force engaged in acts of painful adjustments and delicate balancing in their macroeconomic management. In the midst of geopolitical tension, trade fragmentation and shocks and elevated debt, global economic growth is on razor’s edge. The major policy instruments at the disposal of governments, monetary and fiscal policies, face a difficult trade-off between sustaining economic activity and containing inflation. According to the Organization for Economic Cooperation and Development (OECD), global growth is projected to moderate from 3.4 per cent in 2024 to 3.1 per cent in 2025 and further to 3.00 per cent in 2026. However, other institutions present more cautious numbers. For example, the World’s Bank Global Economic Prospects Report (2025) noted a sharper downgrade showing global growth of 2.3 per cent in 2025, attributing the cut to policy uncertainty, trade tensions and volatile financial conditions. Similarly, the United Nations has projected subdued growth in its World Economic Situation and Prospects Report (2025) estimating 2.8 per cent growth for the period, citing weak investment, high amount of debt and policy uncertainty as constraints.

According to the Organization for Economic Cooperation and Development (OECD), global growth is projected to moderate from 3.4 per cent in 2024 to 3.1 per cent in 2025 and further to 3.00 per cent in 2026. However, other institutions present more cautious numbers. For example, the World’s Bank Global Economic Prospects Report (2025) noted a sharper downgrade showing global growth of 2.3 per cent in 2025, attributing the cut to policy uncertainty, trade tensions and volatile financial conditions. Similarly, the United Nations has projected subdued growth in its World Economic Situation and Prospects Report (2025) estimating 2.8 per cent growth for the period, citing weak investment, high amount of debt and policy uncertainty as constraints.

Taken together, these estimates suggest that while the global economy is not heading towards a recession, growth is below long term pre-pandemic trends and is vulnerable to downside shocks. A brief appraisal of the main landmarks in the global economic landscape can give a more clear idea about the state of the global economy that prevails now.

Inflation: According to the OECD interim Economic Outlook (March, 2025), inflation in G20 economies is expected to decline modestly. Headline inflation is projected to fall from 3.8 per cent in 2025 to 3.2 per cent in 2026 but core inflation will persist in many countries. From the UN report, it transpires that global inflation is expected to moderate from 4.0 per cent in 2024 to 3.6 per cent in 2025, declining to 3.6 per cent in 2026. But policy uncertainty and trade measures could complicate inflation, the Report has cautioned. Thus, though inflation is easing globally it remains elevated in many countries. Persistent core inflation, especially in services, is of particular concern.

Employment: Labour markets globally have shown resilience. The OECD notes that nominal wage gains remain strong and disinflation is helping restore real incomes, though private consumption remains subdued amid weak confidence. According to the UN’s World Economic Situation and Prospects Report (June2025), while the the global unemployment rate held around 5 per cent, forward- looking indicators suggest potential deterioration because of policy uncertainty. The International Labour Organization (ILO) has recently revised its global growth forecast downward, projecting a measly 1.5 per cent job growth in 2025, equivalent to some 53 million new jobs – about 7 million fewer than previously estimated. In short, globally labour markets remain comparatively tight and risks loom: slower growth, policy uncertainty and fragmentation of trade. All or any combination of these factors can weaken job creation in near future .

Now let us see the snapshots of the major economies in terms of the indicators discussed above.

America: According to OECD projections, the American gross domestic product (GDP) growth is expected to decelerate from 3.00 per cent to 2.8 per cent in 2024 to 2.2 per cent in 2025, and further to 1.6 per cent in 2026, largely due to the high trade barriers and policy uncertainty caused by Trump administration. The IMF’s World Economic Outlook also signals a slower trajectory with constrained net immigration and rising tariffs weighing on investment. Some analysts even warn of a possible ‘stagflation- like’ situation, with tariffs slowing growth sharply and inflation persisting.

Inflation. Elevated tariffs and trade fragmentation may reintroduce upward price pressure in America. The OECD warns that persistent trade fragmentation could not only make inflation stubborn, but also push it higher.

Employment. The OECD notes that labour markets in America are easing gradually and unemployment remains relatively low compared to historical averages. Wages are still rising nominally, supporting consumer income. However, with growth slowing, job creation may weaken. The risk that elevated tariff and trade uncertainty may dampen hiring, especially in trade-exposed sectors looms large.

Policy constraints. Under pressure from president Trump, American central bank, the Fed, has lowered basic interest rates by .05 basis points recently, bringing the total to 3.5 per cent. But inflation is still around 3 per cent, which is above the 2 per cent target of Fed. The out-of-sync monetary policy is likely to aggravate inflation and unemployment. The high debt-to-GDP ratio (125 per cent) of America has increased fiscal risk especially when interest payment remains a burden.

European Union: According to the European Commission’s 2025 Forecast, EU’s real GDP is projected at 1.1 per cent in 2025, rising to1.5 per cent in 2026. Compared to America, the growth rate in EU is lower for a number of reasons. The first is the Ukraine war which has affected the energy sector, raising cost of production and has in some cases led to reduction and even stoppage of production. The second is the tight monetary policy followed by European Central Bank since 2022. High rate of interests discouraged new investment resulting in lower rate of growth. The third is the strict regulatory framework applied uniformly across EU for business and industries. Compliance with rules and regulations has discouraged producers of goods and services. Fourthly, China’s economic slowdown and trade frictions have reduced external demand for EU goods leading to reduced production. As a result if all these EU’s present rate of growth at 1.1 per cent is less than half of the growth rate that prevailed before 2020.

Inflation. The European Union has been most successful in containing inflation and then America and the UK. Through its robust monetary policy the European Central Bank (ECB) has managed to bring down inflation to the targeted rate of 2 per cent. This has enabled the central bank to reduce the interest rate to

Employment. Because of low rate of growth unemployment in EU countries is high, about 5.9 per cent in 2025 with little change expected in 2026.

Debt to GDP ratio. EU-wide debt is around 83 per cent of GDP in 2025 and projected to rise to 84 in 2026. Several member countries (Italy, Greece, Portugal, Belgium) have debt levels above 100 per cent. The debt amount is high because many EU countries run large budget deficits, the average deficit is around -3.3 per cent of GDP. Rising interest costs, larger defence spending after Ukraine war and spending for subsidy in agriculture are keeping deficits high.

Policy tools. The ECB has used monetary policy vigorously to stabilise the euro zone economies, first through Quantitative Easing and lately with monetary tightening. But fiscal policy of member countries has been lacklustre, marked by deficits and public borrowing to bridge the fiscal gap. Monetary policy is likely to be more dominant as a policy instrument than fiscal policy in the near future.

China: After posting GDP growth rate between 8 to 10 per cent annually for a decade, China’s economy cooled and settled at the modest rate of 5 per cent during 2024. For 2025, the Politburo fixed the growth rate at 5.5 per cent indicating the pragmatic approach of its policymakers. The export-driven growth strategy may receive a makeover now after the shock of high tariffs on almost all Chinese exports by America. This is likely to lead to a drastic restructuring of Chinese economy, giving emphasis on consumer goods for domestic market. Long-term forecasts indicate a gradual slow down due to demographic decline, weak property markets and slower productivity growth.

Inflation. China is experiencing very low inflation over the past few years, ranging around 0-1 per cent. It tends to be so low at times that deflationary pressure is apprehended. However, the inflation target has been revised and is expected to rise to 1.5 per cent next year.

Employment. Official urban unemployment remains roughly at 5.0-5.50 per cent. But youth unemployment is higher and is considered a major structural problem. A shrinking working- age population is expected to reduce labour supply in the long run.

Fiscal policy. China has adopted a more aggressive fiscal stance for 2025, raising its deficit target to 4 per cent, higher than in recent years. The government plans to issue 1.3 trillion yuan of long-term special treasury bonds in 2025 to support local government financing. The fiscal stimulus is designed to boost infrastructures development, support local government spending and boost consumer spending. China’s fiscal policy is aggressive and pro- growth but in the process it may be running up debt and fiscal liabilities that may not be sustainable in future.

Monetary policy. People’s Bank of China has adopted a moderately loose monetary policy stance, cutting interest rates, reducing reserve requirements of banks and injecting liquidity into financial institutions. These policies aim to support domestic demand and counter deflationary pressure. However, this policy’s effectiveness may be hampered by weak consumer demand, property overinvestment and fall in exports resulting from high tariff imposed by America on all Chinese goods.

Bangladesh: Bangladesh’s GDP growth slowed to about 3.8 per cent in FY25 due to external shocks (supply chains, Ukraine war) and popular unrest during 2024. The political uncertainty that has followed the upheaval has created a kind of economic doldrums, keeping new investment suspended. According to the World Bank forecast, growth is expected to rebound to around 6.5 per cent in FY26 as conditions stabilise.

Inflation. Consumer price index has remained stuck above 8.5 per cent over the past year. The inflationary factors have not responded to tight monetary policy indicating that fiscal profligacy of the past may be having its last gasp. Meanwhile, soaring living costs have inflicted great suffering on middle and lower middle class, not to speak of the poor.

Employment. Following the Covid pandemic, the number of unemployed rose steeply, particularly among the educated semi- skilled. The present stagnation in the economy has accounted for increase in the number of unemployed in addition to increase in the number of poor. Many workers remain vulnerable due to reliance on informal sectors and limited social protection.

Policy options. The country has faced chronic fiscal deficit owing to very low collection of revenue. With revenue-GDP ratio at 6 per cent, successive governments have relied on borrowing from banks and external agencies to cover its expenses. Bangladesh’s debt- to- GDP ratio being at 45 per cent the country is still within the acceptable limit. But its rising trend and the growing burden of debt servicing has become a matter of concern. The fulfilment of conditionalities attached to the $4.5 billion IMF loan could improve the fiscal space but the performance to date does not engender much hope. The government faces a difficult trade-off: increasing debt to invest in infrastructure and to drive growth and manage fiscal sustainability at the same time .

Monetary policy. Bangladesh Bank, in charge of formulating monetary policy, has a limited space, faced as it has been with a inflation rate ranging between 8.5 to 9.5 per cent during the past one year. Constrained by the need to control inflation, the central bank has raised the policy rate to 10 per cent. This, together with the high lending rates of commercial banks has dampened private sector investment, the major contributor to GDP growth and employment. The investment climate is so bleak that private sector borrowing has come down to 6 per cent even though the target had been fixed at 10 per cent. The monetary policy has been more successful in controlling the volatility in the foreign exchange market.

Conclusion: The global economy is going through a turbulent patch, mostly an outcome of self-serving policy stances taken by the two superpowers. Their pursuits of geo-political and geo-economic interests have upended the rule-based global economic and political orders with resultant adverse consequences both for the perpetrators and third parties. Under the weight of multiple sanctions the Russian economy has shrunk but the sanctions have also affected other countries, including Bangladesh, which have trade relations with Russia. The impact of the wide-ranging tariffs imposed by America has started to bite the economies coming within its ambit but its full force is yet to be the felt. Ironically, American consumers and investors have become the unintended victims of the sweeping tariff regime unleashed by their president. Economic sanctions, making financial transactions in global trade nearly impossible even for other countries in addition to the sanctioned, may lead to a new reserve currency and a new international payment system. BRICS member countries have already taken some tentative steps in that direction which may evolve in to a full-fledged alternative financial mechanism, rivalling the present one based on US dollar and the SWIFT account network. Meanwhile, rationalisation of tariffs by all countries may come out of the crisis created by the vindictive trade policy of president Trump. On the policy side, countries can be expected to give more attention to revisiting their fiscal and monetary policies for dovetailing to manage their economies routinely, rather than tinker with these during emergencies.

hasnat.hye5@gmail.com