Time for new and innovative approach

Mohammed Tajul Islam | Thursday, 17 April 2014

As a nation we clearly need to invest in infrastructure. To be on the higher trajectory of GDP (gross domestic product) growth, the ratio of investment to GDP needs to be raised to 35-40 per cent from its present average investment-GDP ratio of around 25 per cent. The government has estimated that more than Tk 4.8 trillion or USD 58 billion needs to be spent in the five years from 2011 to 2016. With such a large infrastructure gap, the big question is how to fund and finance the nation's growing infrastructure need.

It should be made clear that the one important element in review of key infrastructure assets is the difference between funding and financing. Media discussions do not usually draw a distinction between these processes, but there is a clear line between the two activities, since the roles of both are distinct and critical in developing an efficient infrastructure market.

The funding of infrastructure has been defined as the allocation of ultimate cash flows that support the construction and operation of infrastructure. The financing of infrastructure has been defined as selecting the immediate source of cash that will physically develop the assets with the repayment of this investment over the life of the asset. Funding is the revenue stream that repays the financing. For example, a mix of private sector debt and equity financed the Gulistan Jatrabari toll flyover project -private investment funded with toll charges from users of the asset.

WHAT IS FUNDING? The implication of the above definition is that there are in reality only two sources of infrastructure funding for projects sponsored by a government: an allocation of general taxation revenue or direct user charges. Where projects cannot be funded by user charges the government must allocate taxation revenue. Naturally a government has the choice to fund through current taxation revenue, or future taxation revenue by borrowing to complete the infrastructure.

While the taxation approach does lead to a conservative pace of development, relying largely on year-to-year taxation to fund long-term assets raises important intergenerational equity issues. Faster infrastructure development requires a more innovative funding approach from the government, and this would stimulate further financing from home and abroad. Harnessing broader application of user charges is needed to ease the funding burden. Both the government and the private sector have critical roles to play in future infrastructure funding and financing.

WHAT IS FINANCING? Efficient financing of infrastructure is focused on the allocation of project and systematic risks to those parties best able to manage them. Governments have a wide range of financing solutions, public and private, local and foreign, to develop infrastructure. Mega projects like Padma multipurpose bridge, mono rail, metro rail, expressway, large power projects, deep sea port etc. require big investments and therefore determining the appropriate financing mix is very critical for the government to decide.

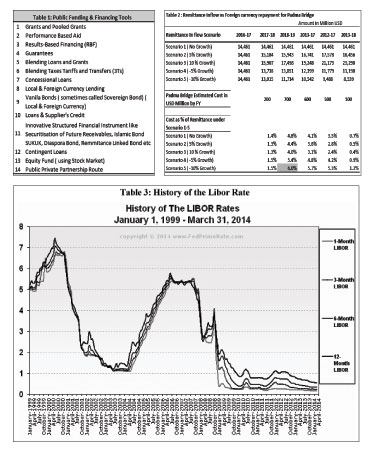

Let us see what the alternatives are available for the government to fund and finance mega projects as depicted in Table 1:

The government may choose any combination of funding and financing keeping in mind the availability and affordability, macro-economic impact, balancing the cost of fund, project economics, economic and social return of the project and ultimately short, medium and long term contribution to the national economy i.e GDP growth.

On many occasions, it is argued that any concessional loan from development partners is one of the best options available to the government to finance large and mega projects. Is it one of the best options or the only option? When we call it one of the best options, it is also implies that there are other alternative options. Now the question is: how is the best option defined? Is it defined based on the concessional rate of interest? Could all the mega projects be financed with concessional loans? If, for whatever reason, development partners are reluctant to finance any mega project, what is the future of the project? For example, the government undertakes a project which costs US$ 5.0 billion, if implemented by 2014-2019. If the government defers the project implementation to 2017-2022 for seizing any concessional loan, the cost of the project will rise to US$ 7.0 billion from US$ 5.0 billion. In view of the hike in project cost and getting the concessional loan three years later, is it cost-effective and does it have any impact on the GDP growth?

There is no straightforward answer to all the above questions. The government should take necessary steps to explore other innovative financing mechanisms alongside pursuing concessional loans for its mega projects, and this scribe believes the government is moving in that direction. The success of pursuing any alternative financing mix depends on project economics, the country and the concession, public-private risk sharing, financing structure, funding structure, government support, guarantees and risk analysis, and mitigation measures.

THE CASE OF PADMA BRIDGE: For example, many say that implementing the Padma multipurpose bridge project without any concessional loan would not be a viable option. What is the rationale of the argument? Can we draw a conclusion based on facts and figures only? Has the government made the feasibility report? Do we know what the toll framework for the proposed bridge is? Do we have any data on traffic flow to and from each direction? Do we have any assessment report on affordability? Do we know the terms and conditions of the existing financing structure? Do we have any study on the bridge's contribution to the economy? What is the extent of risk associated with the interest rate, if the bridge is constructed with market-based financing, and what is the extent of impact? What is the economic and social return of the project? What is the impact of various financing methods on macroeconomic indicators? The government may have most of the answers, but we don't. Hence, there is no single answer to these questions, as it depends on the circumstances of a specific project. Therefore, without knowing the exact facts and figures we cannot take a concrete decision that there is hardly any alternative option.

INNOVATIVE FINANCING MIX: The government now needs to explore an alternativee model, which could be categorised as a hybrid funding and financing solution designed to deliver economic and social benefits from infrastructure investments while maximising the ability to leverage private sector capital at home and abroad.

The financing mix may include providing debt and equity by the government, establishing infrastructure development companies and exploring new funding instruments like infrastructure bonds, Diaspora Bond, Remittance Linked Bond, Izara Sukuk (Islamic Shariah Compliance Instrument to tap the Shariah compliance investors-local and global), Securitisation of Future Receivables, Guaranteed Bond, Equity Fund etc. Each model is different and has varied impacts on financial efficiency, pricing and the ability to leverage private capital. Selection of the right model must be made on a case-by-case basis in light of each project's specific risk profile and will require the government to apply sound commercial principles and make a strong contribution to delivery. Now is the time for the government of Bangladesh to cement its position in the global market through innovative infrastructure financing and funding models.

Now let us focus on Diaspora Bonds.

WHAT IS DIASPORA BOND? A diaspora bond is a bond or debt instrument that is issued by the government of a country, say Bangladesh, similar to other bonds except that this financial instrument will be marketed to Bangladeshis overseas and will not be sold in Bangladesh. This bond gets its name because it is sold to a nation's diaspora who are able to purchase the bond in foreign currencies which is extremely valuable for investments at home. Although the diaspora bond is marketed and sold to the diaspora, several countries that have successfully issued these bonds have permitted proxy purchase, which allows citizens at home to buy these bonds through friends and families abroad. The bonds are issued based on the presumption that their emotional ties to a country make investing in such products worthwhile. Sales can be restricted solely to members of a particular nationality or open to all buyers, with nationals receiving a preferential rate.

Bangladesh is one of the top remittance-receiving countries of the world. This is a clear indication of the bonding of a diaspora with its home country. With a large diaspora population there the bond provides an opportunity to tap into a capital market beyond international investors, foreign direct investment and loans. If a government experiences difficulties raising money on the international market or attracting investment, the diaspora bonds can be an attractive new source of financing. Three other principal benefits stand out for the issuing governments:

* A successful issue, along with the access to steady new funding, may help improve ratings on a country's sovereign debt.

* Buyers may continue to purchase bonds, even when markets are sceptical about a nation's economic outlook.

* Countries in essence receive a "patriotic" discount when they issue diaspora bonds, as investors are often willing to accept returns much lower than they might on the open market.

Patriotism, an emotional force, has rarely been applied to finance, but it could yet prove an effective fundraising mechanism for emerging economies that are struggling to raise money on the capital markets or through foreign investment. Any government that wants to issue diaspora bonds must lay the groundwork with a strong information campaign. Perhaps, more importantly, it must also be prepared to give its diaspora people a greater say on how any fund raised will be used. Clearly diaspora bonds cannot solve all the problems of a country in need of alternative sources of investment. But they can be part of the solution. To tap that wealth, however, countries will have to focus on engaging with their diaspora population and treat them as returning customers rather than fair-weather friends.

Mr. Vayalar Ravi, Overseas Indian Affairs Minister, said at the 5th biennial diaspora conference of India in June, 2013: "Underlining the need for greater two-way engagement between India and its diaspora, the government had initiated a number of steps to ensure greater participation of the community in the economy of the country. Diaspora engagement is also seen in the strong surge in remittances back home, the return of many to live and work in India and in their increasing participation in India's development."

According to the World Bank, African diaspora savings, at US$ 53 billion every year, exceed annual remittances to the continent and are mostly invested abroad. "If one in every 10 members of the diaspora could be persuaded to invest $1,000 in his or her country of origin, Africa could raise $3 billion a year for development financing," Dilip Ratha and Sonia Plaza write in the World Bank's 2011 report on Diaspora for Development in Africa.

Diaspora bonds typically offer small denominations and are marketed to expatriate communities, whose long-term and emotional connection to their homelands often makes them open to smaller returns or riskier propositions than the average foreign investor.

THE RATIONALE FOR THE ISSUER OF DIASPORA BONDS:

* Countries are expected to find diaspora bonds as an attractive vehicle of securing a stable and cheap source of external finance. Since patriotism is the principal motivation for purchasing diaspora bonds, they are likely to be in demand in fair as well as foul weather.

* The patriotic discount, which is tantamount to charity, raises an interesting question as to why a country should not seek just charitable contributions from their diaspora instead of taking on debt associated with the diaspora bonds. More importantly, diaspora bonds allow a country to leverage a small amount of charity into a large amount of resources for development.

* The benefit of issuing diaspora bond is the favourable impact it would have on the country's sovereign credit rating. By making available a reliable source of funding that can be seized in both good and bad times, the nurturing of the diaspora bond market improves a country's sovereign credit rating. Rating agencies believe that the country's ability to access the worldwide Bangladeshis for funding has undoubtedly supported its sovereign credit rating.

* Another important rationale is that when a diaspora bond will be redeemed, the maximum proceeds of the bond received by the diaspora bondholders will be ploughed back to its home country through remittance which will positively impact on the foreign currency reserve. But it will not be the case for other foreign currency bond.

THE RATIONALE FOR THE INVESTORS OF DIASPORA BONDS:

* Why would investors find diaspora bonds attractive? Patriotism defines largely the investors purchasing diaspora bonds. Beyond patriotism, however, several other factors may also help explain diaspora interest in bonds issued by their country of origin.

* The principal one among these is the opportunity such bonds provide in risk management. The worst-case default risk associated with diaspora bonds is that the issuing country would be unable to make debt payments in the hard currency. But its ability to pay interest and the principal amount in the local currency is perceived to be much stronger, and therein lies the attractiveness of such bonds to diaspora investors.

* Typically, diaspora investors have current or contingent liabilities in their home country and hence may not be averse to accumulation of assets in the local currency. Consequently, they view the risk of receiving debt service in the local currency with much less trepidation than purely dollar-based investors. Similarly, they are also likely to be much less concerned about the risk of currency devaluation.

* Still other factors supporting purchases of diaspora bonds include the satisfaction that investors reap from contributing to economic growth in their home country. Diaspora bonds offer investors a vehicle to express their desire to do "good" in their country of origin through investment.

* Furthermore, diaspora bonds allow investors the opportunity to diversify their assets away from their adopted country.

* Finally and somewhat speculatively, diaspora investors may also believe that they have some influence on policies at home, especially on bond repayments.

Only features of the diaspora bond have been discussed here because of its unique characteristics. The policy makers may also think about SUKUK, Remittance-linked bond issuance and other structured products for its mega project financing. The Table 2 shows different scenarios of remittance inflow and foreign currency payment for the Padma Bridge project. Under all five different scenarios, the highest outflow would be in the fiscal year (FY) 2018-19. Therefore, there is a strong proposition for launching Remittance-Linked Bond as well.

Now it can easily be said that the domestic market alone cannot meet the investment requirements. Exploring foreign markets with an appropriate structure is inevitable to bridge the gap of financing. The time is also very important for raising funds from foreign markets. The Table 3 gives the history of Libor Rate from 1999 to 2014. It is clearly shown that the Libor rate is historically lowest during these periods. In March 2014, the 6-month Libor rate is only 0.334 per cent and the 3-month Libor rate is 0.234 per cent. Therefore, it is the right time to approach the international market for financing large projects.

The writer is Senior Vice President and Chief Rating Officer of the Credit Rating Agency of Bangladesh Limited. The views expressed are solely the writer's own. tajul@crab.com.bd