Troubled loans

Towards a client-focused solution

Nazneen Ahmed | Sunday, 24 November 2019

![]() The Achilles heel of Bangladesh economy's development story is the performance of the financial sector. To be precise, the banking sector's non-performing loans (NPLs) remain a major headache. When a loan is sanctioned, it includes a repayment schedule: paying off the principal amount along with interest. A loan becomes non-performing when the borrower fails to pay the scheduled principal off and interest amounts for more than 90 days. If the level of NPL grows, it reduces the capacity of the banks to extend further loans, their capacity to repay the depositors while undercutting their ability to earn profits. The building-up of massive NPL may lead to liquidity crisis in the overall banking sector and even failure of banks. As of June 2019, such loans in the banking sector reached Tk 1.12 trillion (112,425 crore), which is almost one-fifth of what was at the end of December 2018. The rising NPL is, no doubt, a threat to the stability of the financial health of the country and we need an effective remedy to this problem.

The Achilles heel of Bangladesh economy's development story is the performance of the financial sector. To be precise, the banking sector's non-performing loans (NPLs) remain a major headache. When a loan is sanctioned, it includes a repayment schedule: paying off the principal amount along with interest. A loan becomes non-performing when the borrower fails to pay the scheduled principal off and interest amounts for more than 90 days. If the level of NPL grows, it reduces the capacity of the banks to extend further loans, their capacity to repay the depositors while undercutting their ability to earn profits. The building-up of massive NPL may lead to liquidity crisis in the overall banking sector and even failure of banks. As of June 2019, such loans in the banking sector reached Tk 1.12 trillion (112,425 crore), which is almost one-fifth of what was at the end of December 2018. The rising NPL is, no doubt, a threat to the stability of the financial health of the country and we need an effective remedy to this problem.

So far, the discussion on NPL has been centered mostly around the issue of large loan defaults by influential borrowers and loan scams caused by collusions between bank officials and borrowers. While it is true that a large amount of bank loan has remained stuck and unrecoverable on these two counts (influential borrowers and collusion), there are at the same time a large number of other cases of NPL, which are due to the reasons beyond these two. The loan recovery strategy, therefore, needs to take these other reasons for default into cognisance and design the recovery measures accordingly. A standard practice to deal with defaulted loan is to reschedule the loan following the Bangladesh Bank guidelines. However, the common perception is that this measure has lost its effectiveness because of overuse by the loan defaulters, and therefore, future loan recovery pursuits should involve stringent measures against these defaulters. On the other hand, some underline the need for differentiating wilful defaulters from the rest of the defaulters and creating opportunities for the latter group to repay the loan, where possible, through rescheduling.

A standard practice to deal with defaulted loan is to reschedule the loan following the Bangladesh Bank guidelines. However, the common perception is that this measure has lost its effectiveness because of overuse by the loan defaulters, and therefore, future loan recovery pursuits should involve stringent measures against these defaulters. On the other hand, some underline the need for differentiating wilful defaulters from the rest of the defaulters and creating opportunities for the latter group to repay the loan, where possible, through rescheduling.

The Bangladesh Bank guidelines of 2012 clearly describe the conditions for rescheduling different types of NPLs (sub-standard, doubtful and bad loans). In May 2019, the central bank published a circular, which sets new conditions for rescheduling loans for some specific types of businesses and for loans classified as bad loans because of reasons beyond the borrowers' control. The application for rescheduling can be submitted only by those who were already declared defaulters on 31 December 2018. This circular allows a defaulter to apply for rescheduling by paying a minimum of 2.0 per cent of the ledger balance whereas, according to the 2012 guidelines, the down payment requirement varied from a low 5.0 per cent to a high 50 per cent. The maximum time limit for repaying loan according to May 2019 circular is up to 10 years, whereas, according to the 2012 guidelines, the total time limit (allowed in the maximum of three rescheduling process) could be four and a half years. Undoubtedly, the new circular has provided flexibility to the defaulters to repay loan by rescheduling it with relatively flexible terms and conditions. This circular has been heavily criticised and a writ petition has been filed to stop its application. The issue has yet to be resolved, though the Appellate Division of the Supreme Court has temporarily withheld the applicability of the stay order issued by the High Court Division in response to the writ petition.

The presence of influential borrowers amongst the top loan defaulters has triggered public outcry with a call for strict actions against the loan defaulters. However, a dispassionate approach to the issue requires one to assess the incidence of wilful defaulters and examine other possible reasons behind loan default. To the extent that a borrower may have experienced business failure due to reasons beyond his or her control, there may be a strong case for extending a helping hand, thus create opportunities for business revival leading to the recovery of loans. For designing such a pragmatic recovery plan, it requires empirical evidence on the distribution of loan defaulters by reasons behind loan default.

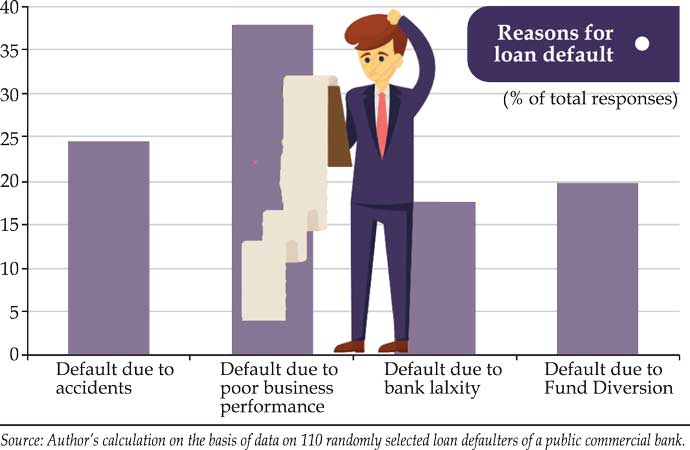

We made an attempt to get a glimpse of the situation on the basis of a randomly selected sample of classified loans of a public commercial bank. A total of 110 such cases were examined where the loan amount varied from Tk. 0.2 million and Tk. 8.6 million. Most of the loans became classified during the last 15 years, while some have remained classified for the last 25 years.

An analysis of the causes behind these loan defaults shows the following distribution.

(i) Poor business performance

About 38 per cent of the default cases belonged to this category, where the borrower incurred loss due to unfavourable business situation beyond his/her control.

(ii) Personal and other mishaps/ shocks

Another 25 per cent of the loan default cases was due to shocks arising out of personal mishaps such as death, major illness etc. or accidents such as fire or other family and social calamities.

(iii) Laxity on the part of the bank

The lack of due diligence, monitoring and follow up support on the part of the bank account for another 17 per cent of the default cases.

(iv) Fund diversion

Loan default due to fund diversion accounts for about 20 per cent of the studied cases. There are two variants of this category. In a smaller number of cases, the borrower did not undertake any investment with the borrowed fund and instead indulged in money laundering, conspicuous consumption or made unproductive uses such as land purchase. These fall in the true "wilful defaulter" category and account for only about 3.2 per cent of the cases. The remaining 16.8 per cent of the fund diversion cases involved the use of the borrowed fund for unplanned expansion of the existing capacity or unplanned investment in other businesses without the approval of the bank. In many cases, thin distribution of the fund against over-expanded business threw the borrower into cash flow problem, resulting in default in repaying installments.

Many of the wilful defaulters are influential borrowers who managed to get the loan against little or no collateral or collateral of dubious quality-something that kept the state lender from pursuing the recovery. These wilful defaulters have little incentive to repay the loan. However, the majority of borrowers who defaulted because of unplanned business activities can flex no muscles and are willing to pay the loan back. They often take recourse to legal action to temporarily shield themselves from the recovery drive of the bank.

The May 2019 circular of Bangladesh Bank has come under fire on the ground that it shows undue leniency towards wilful defaulters. This criticism, however, seems to be misplaced as the circular is targeted not towards the wilful defaulters but other defaulters, who-unlike the wilful defaulters-lack the clout to shield themselves indefinitely from the pressure of the bank for loan repayment, and who can be induced into clearing their defaulted loans with right incentives.

As the limited evidence presented here shows, in nearly 80 per cent of the cases, the borrower is not particularly responsible for the loan default. Most of these borrowers are regular businessmen or entrepreneurs, some belonging to small and medium enterprise categories who are struggling to create self-employment and employment for others but suffered business losses for various reasons. They do not have the power to reschedule their loans beyond regulations and are willing to repay the loan if they are given the breathing space.

Even in cases, where the fund has been diverted in an unauthorised manner to expand business, "irrational exuberance" rather than unwillingness to repay bank loans, seems to have been the causal factor behind loan default. In such cases, providing the space within which the borrower can rationalise his or her business involvement can create the scope for the borrower to revive business and repay loans.

While the number of wilful defaulters seems to be relatively small, the amount of loans involved is colossal. It is interesting to note that a few of such large wilful defaulters have tried to avail the flexible rescheduling facility of Bangladesh Bank. These and other defaulters who did not avail the facility and those who faltered in paying installments after availing the liberal rescheduling facility will prove themselves to be wilful defaulters. The government will be left with no choice but to proceed against them in the strongest possible manner. For this, a firm commitment is needed like the on-going anti-corruption drive, to uproot the cancerous ill of defaulted loans from our banking system. There is also a need for challenging the criticism that the flexible rescheduling facility offered by Bangladesh Bank will encourage future borrowers to default in their loan repayment, perpetuating the loan default culture.

Bangladesh has achieved a phenomenal success in steadily raising its GDP (gross domestic product) growth and reducing poverty. The financial sector in Bangladesh has a critical role to play in sustaining this growth momentum by encouraging budding entrepreneurs to undertake investment and generate employment. While maintenance of discipline in the financial sector through strict dealing with wilful defaulters is an essential prerequisite for this endeavour to succeed, flexible treatment of genuine business people also must go hand in hand.

The writer is Senior Research Fellow, Bangladesh Institute of Development Studies (BIDS). nazneen7ahmed@yahoo.com