Trend in cash holding outside banks: any reason for panic?

Zaid Bakht | Friday, 31 May 2024

The financial sector of Bangladesh experienced quite a bit of turbulence in recent times and in fact, is not out of the woods yet. In particular, there has been significant erosion of public confidence towards the country's banking sector. The classification of the commercial banks in different color zones (red, amber, green etc) reflecting the magnitude of their risk exposures, the ill prepared move towards bank mergers, sudden takeover of the ownership of several banks, particularly Islamic type banks by a lone business conglomerate, the news of big sums of money being given out as credit from these banks to hardly known entities without due diligence, the continued impunity of people responsible for the collapse of the BASIC bank etc have all been at the epicenter of the tremor shaking up public confidence in the country's banking system. The controversy surrounding the choice of the appropriate monetary policy in tackling persistent 9%-plus inflation added to the woes of the sector. The central bank retained, for quite sometimes, the cap on the deposit and the lending interest rates and then moved on to a moderately flexible interest regime guarded by the Six-monthly Moving Average Yield Rate of Treasury Bills (the so-called SMART rate) on two apparently valid grounds. First, the continued inflation was mainly import induced intensified by depreciating exchange rate and depleting foreign exchange reserves

The controversy surrounding the choice of the appropriate monetary policy in tackling persistent 9%-plus inflation added to the woes of the sector. The central bank retained, for quite sometimes, the cap on the deposit and the lending interest rates and then moved on to a moderately flexible interest regime guarded by the Six-monthly Moving Average Yield Rate of Treasury Bills (the so-called SMART rate) on two apparently valid grounds. First, the continued inflation was mainly import induced intensified by depreciating exchange rate and depleting foreign exchange reserves  and hence demand management through contractionary monetary policy was perhaps not the right answer particularly given the fact that credit growth to the private sector lagged significantly behind target growth. Second, the enhanced interest rate would be a fatal straw on the back of the business camel already overburdened by rising raw material and utility costs and the lingering adverse impacts of the pandemic and the Russia-Ukraine war. Ultimately, however, the central bank succumbed to the pressure for completely market-based interest rate. Possible reasons behind this policy shift includes the realisation that inflation control is unlikely to be successful unless inflationary expectations are subdued. Also, donor persuasions may have played an important role.

and hence demand management through contractionary monetary policy was perhaps not the right answer particularly given the fact that credit growth to the private sector lagged significantly behind target growth. Second, the enhanced interest rate would be a fatal straw on the back of the business camel already overburdened by rising raw material and utility costs and the lingering adverse impacts of the pandemic and the Russia-Ukraine war. Ultimately, however, the central bank succumbed to the pressure for completely market-based interest rate. Possible reasons behind this policy shift includes the realisation that inflation control is unlikely to be successful unless inflationary expectations are subdued. Also, donor persuasions may have played an important role.

Pending these policy corrections, the banking sector was up against two major battles - the fight for deposit under a negative real interest rate regime, and cash crunch caused largely by the need to purchase foreign currency for import financing.

Amidst such struggling time in the banking sector, a popular vernacular newspaper came up with a news story recently that cash held by public outside the banking system experienced sudden surge, rising by Tk 36.21 billion in March 2024. The newspaper ascribed this mainly to deteriorating public confidence in the country's banking system and the failure of the central bank to control money supply due to issuance of bonds by the government against the payments due in the power and fertilizer sectors. It also mentioned the ensuing month of Ramadan as a possible reason behind increased cash holding. Other possible reasons not included in the news report were low real rate of interest and increased flow of remittance prior to Eid-ul-fitar.

The news item triggered shockwaves in social media and concerns were expressed regarding the health of the banking sector and the effectiveness of the central bank. Clearly, these concerns lacked a proper understanding of the significance of additional cash holding of this amount and the true picture regarding the success of the central bank in controlling money supply. This write up is an attempt to shed light on these issues.

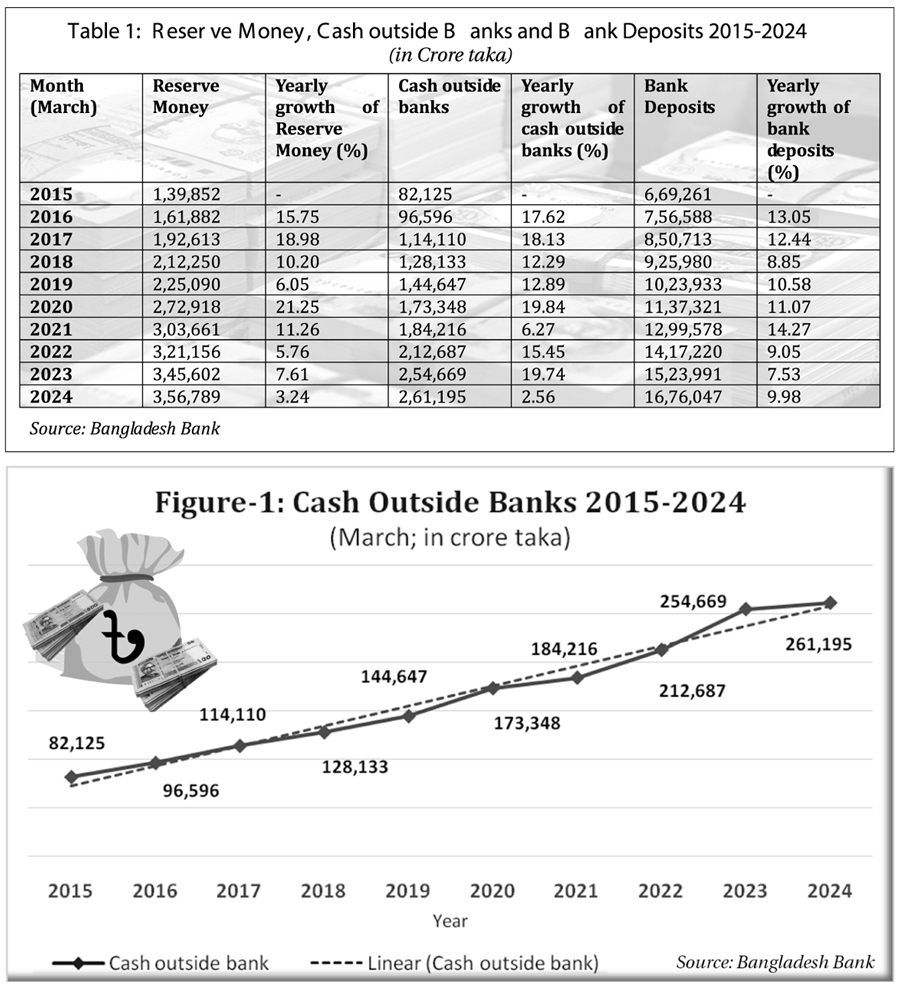

Table-1 shows Reserve Money, Cash outside Banks, and Bank Deposits in the month of March during the past 10 years. Since there can be significant month to month variations in cash holding due to a variety of reasons such as festivals, special occasions etc. one needs to look at yearly growth in cash holding rather than month to month changes.

The evidence shows that growth of Reserve Money was the lowest in 2024 (March) during the last 10 years. It may be mentioned here that the central bank set a target growth of zero per cent in Reserve Money for the half-year ending on December 31, 2023 but the actual growth of Reserve Money during this period was negative (-)2per cent. The sale of huge quantities of foreign currency by the central bank during this period was the reason behind this negative growth of Reserve Money. So, the view expressed in the news story regarding the failure of the central bank to contain money supply does not appear to be tenable.

Also, the practice of commercial banks borrowing from the central bank under REPO by surrendering government bonds is a usual part of bank's treasury management. Such treasury measures are guided by the bank's liquidity needs and the fixed interest rate of the bond. So, the view expressed in the news report that the central bank failed to control money supply because of the bonds issued by the government against the payments that fell due in the power and fertilizer sector seem to have little merit.

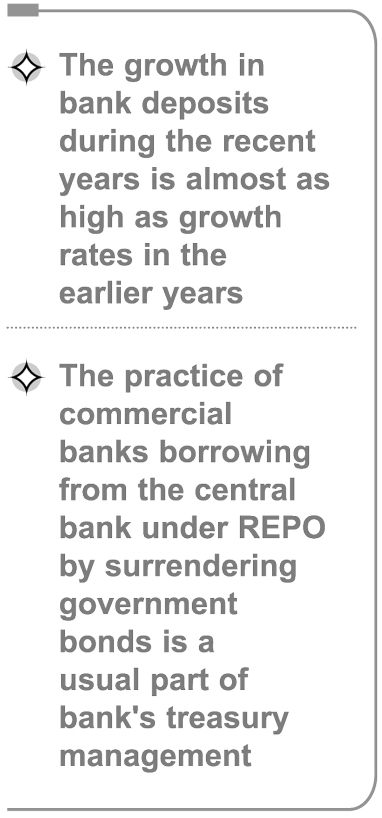

Data provided in Table-1 also shows that during the past 10 years, growth of cash holding outside banks was the lowest in the year ending in March 2024. This implies that the surge in cash holding outside banks in March 2024 reported by the newspaper was due to monthly fluctuations caused by temporary reasons. Also, the line chart in Figure-1 shows that the cash holding level in March 2024 was much in tune with the trend in cash holding during the past 10 years.

Table-1 also shows that the growth in bank deposits during the recent years is almost as high as growth rates in the earlier years. So, the apprehension that depositors have been withdrawing deposits in recent times due to erosion of confidence in the banks and these withdrawn amounts are not being deposited back in other banks is not borne out by actual deposit growth data. While it is true that the debacle in a few taken-over Islamic type banks and the premature announcement of bank merger caused depositors to make large scale withdrawal of deposits from some of these banks the possibility of withdrawn sum being retained as cash in hand seems unlikely.

The upward sloping trend line in Figure-1 suggests, as expected, that cash holding steadily rose over time perhaps due to rising prices and income levels. The fact that the observed trend line (dotted line) shows a close fit with the actual cash holding level (solid line) implies that despite somewhat wide monthly fluctuations in the cash holding the yearly cash holding level followed a steady growth pattern which dispels grounds for panic that may have been caused by the particular news of monthly surge in cash holding.

Dr Zaid Bakht is Chairman, Agrani Bank PLC.

zaidbakht@gmail.com