Uneven disbursement of bank loans adds to regional disparity

Siddique Islam | Saturday, 14 March 2015

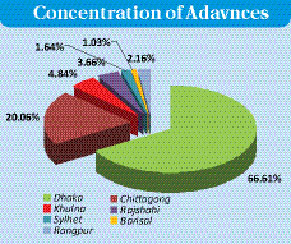

Nearly 90 per cent of the loans and advances of scheduled banks are concentrated in Dhaka and Chittagong divisions, showing an unequal distribution of resources of banks.

Around 70 per cent loans and advances of scheduled banks were invested in Dhaka division while about 20 per cent in Chittagong division during the period between July and September last year, according to the central bank's latest data.

The rest of the loans and advances were disbursed in five other divisions such as Khulna, Rajshahi, Barisal, Sylhet and Rangpur during the period under review.

During the period, the borrowers of Barisal and Sylhet divisions received the lowest volume of loans and advances among seven divisions, data shows.

The total outstanding loans and advances rose to Tk 4,842.52 billion as of September 30 last year from Tk 2,704.66 billion during the same period in 2010.

Available data in last five years has also showed a similar trend in the concentration of loans and advances at division and district level across the country from July-September 2010 to July-September 2014.

Senior bankers and experts have attributed the factors such as inapt planning and lack of attention of the banks, poor infrastructure, investment safety and absence of competent bank officers to the lower flow of credit to rural areas of the country.

They also said some regions grow faster as compared to others for a number of reasons, including better communication facilities, access to energy and natural resources, more concentration of entrepreneurs and availability of skilled workforce.

Such unequal distribution of bank loans and advances has been continuing for years despite strong commitment made by the government to minimise disparities between regions.

"We'll put emphasis on the issue in the next seventh Five-Year Plan which will come into effect from 2016," Senior Secretary and Member of General Economics Division (GED) of the Planning Commission Shamsul Alam told the FE.

Under the existing provisions, the ratio of urban and rural bank branches has to be 1:1 instead of 4:1 earlier.

"We're trying our best to expedite the credit flow in un-banked areas at an expected level through the ongoing financial inclusion programmes," Deputy Governor of the Bangladesh Bank (BB) SK Sur Chowdhury told the FE.

Such concentration of advances will add risk to the risk profile of the banks which will be required to maintain additional capital under Basel-II, according to the Bangladesh Institute of Bank Management (BIBM).

"The banks now need to ensure adequacy of credit flow progressively to rural areas in all productive initiative niche area entrepreneurs," the BIMB said in its latest Banking Review Series 2014.

Talking to the FE, Shah Md. Ahsan Habib, professor and director of the BIBM, said considering the economic and business activities in Dhaka and Chittagong divisions, it is not unusual to have credit concentration in these areas. However, the figure is very high.

"It is unfortunate that our banking sector could not find business cases in the rural economy and small scale business activities," he noted.

"We're enhancing the volume of our investment in small and medium enterprises (SMEs) along with medium and large borrowers for minimising disparities among different reasons and rural and urban areas in Bangladesh," Managing Director and Chief Executive Officer of the Islami Bank Bangladesh Ltd (IBBL) Mohammad Abdul Mannan told the FE.

Mr. Mannan, also vice chairman of the Association of Bankers, Bangladesh (ABB), said the major chunk of loans and advances is made available to a few business entities at Motijheel and Gulshan in the capital Dhaka and Khatunganj and Agrabad in the port city Chittagong, posing a risk in the banking sector. "We have to address the issue immediately."

He also said: "We've to go to the mass people with various banking products for achieving a sustainable and balanced growth and equitable socio-economic development in Bangladesh."

siddique.islam@gmail.com