Unlocking the remittance puzzle

Hundi's impact on Bangladesh's economy and strategies for reform

Syeda Nafisa Anjum and Yeashfa Haque | Wednesday, 14 February 2024

Hundi, is an informal channel of international money transfer, operating independently of the conventional banking system. The process involves Bangladeshi individuals transferring taka to a local hundiwala, who in return deposits equivalent foreign currency in the accounts held by that individual abroad. Similarly, the hundiwala also acquires foreign currency from migrant workers who seek to send remittance back to Bangladesh. The appeal of Hundi among migrant workers emanates from extensive paperwork involved in formal channels, presenting a challenge for the large number of illiterate workers living abroad. Even individuals possessing adequate literacy may also perceive the procedures as tiring and time-intensive. Moreover, the 2009 Bangladesh Household remittance survey revealed that 38 per cent of the remittance recipients lack bank accounts, hindering the use of formal channels.

The appeal of Hundi among migrant workers emanates from extensive paperwork involved in formal channels, presenting a challenge for the large number of illiterate workers living abroad. Even individuals possessing adequate literacy may also perceive the procedures as tiring and time-intensive. Moreover, the 2009 Bangladesh Household remittance survey revealed that 38 per cent of the remittance recipients lack bank accounts, hindering the use of formal channels.

In contrast to bank transfers, Hundi operators facilitate faster money transfers, with no extra fees, and offer flexible transaction hours. Furthermore, According to a scholarly article, a substantial number of 26,820 Bangladeshi workers migrated abroad illegally between 2017 and 2022. Thus utilisation of the formal channels for money transfers presents an inherent risk of divulging the identities of illegal immigrants who are residing abroad without a valid visa or worker’s permit. Hence recourse to Hundi emerges as their sole option. The overvaluation of the taka against the dollar also exacerbated the demand for Hundi services. Despite Bangladesh’s constitutional commitment to a floating exchange rate, in reality, the Bangladesh Bank intervenes to manage the exchange rate.

Moreover, the surge in the demand for Hundi corresponds with the escalation of money laundering. Both businessmen and individuals engaged in illicit activities such as bribes and trafficking employ Hundi as a means to launder their funds, benefiting from the absence of a track record. Additionally, the importers tend to under-invoice the value of their imports—which is declaring a price lower than the actual price— intending to evade taxes.

The increasing popularity of the Hundi creates a noteworthy impact on the remittances and foreign reserves of the economy. As per a 2023 article in the Journal of Economic Criminology, Hundi bears notable implications, signifying its facilitation of money laundering within the economy.

Despite being a significant contributor to Bangladesh’s reserves and economic growth, the decline in remittances from around 24.78 billion U.S. dollars in the FY 2020-21 to 21.03 billion U.S. dollars in the FY 2021-22, a decrease of 15.1 per cent, reflects the impact of Hundi on the accuracy of the current account in the balance of payments.

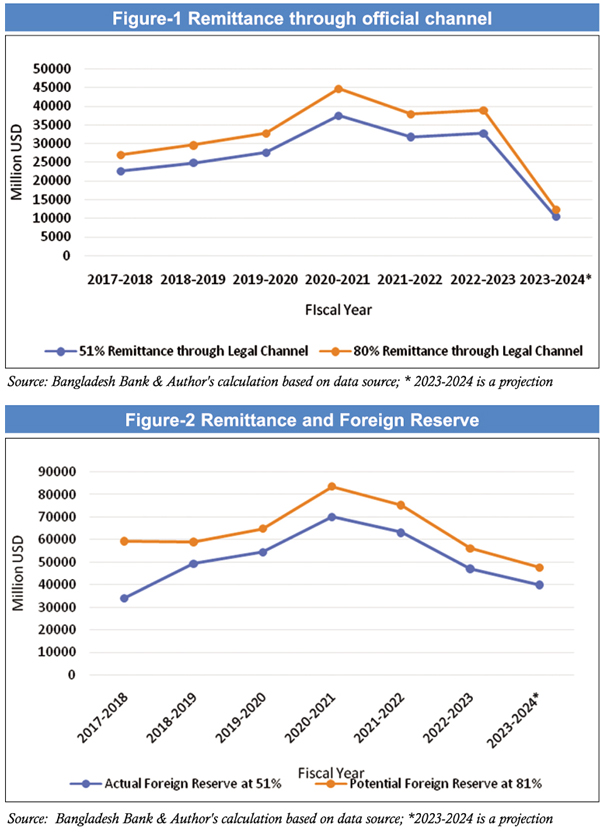

Reports stated that 51 per cent of the remittance transpires through the formal channels while the remaining 49 per cent comes through Hundi. This dichotomy gives rise to two scenarios shown in Figure-1 and Figure-2. Figure-1 illustrates the remittance amount received under 51 per cent utilisation of official channels and the potential remittance amount the economy could accrue under 80 per cent utilisation of official channels.

The presented data illustrates that with 51 per cent of remittance directed through legal channels, Bangladesh accrues approximately US$ 32632.2 million of remittance. However, by augmenting the utilisation of legal channels for international transactions to 80 per cent, the anticipated remittance inflow would reach US$ 38899.31 million in the fiscal year 2022-23. This difference in the two given scenarios emphasises the substantial economic loss incurred by Bangladesh due to the prevalence of Hundi transactions.

Similarly, Figure-2 illustrates that when 51 per cent of remittance is channeled through official avenues the foreign reserves amount to $47116.53 million. Conversely, in the latter scenario, the potential foreign reserve rises to $56165.4 million in the year 2022-23. Consequently, the percentage disparity between the actual and potential foreign reserves is around 19.2 per cent. Notably, Foreign reserves have experienced an increasing trend across all the given fiscal years from 2017-2023.

Therefore, mitigation in remittance through Hundi channels instigates an elevation in the remittance flow within the economy, augmenting the reserve position. As a result, this can potentially assist in mitigating the current dollar crisis to a certain extent.

The transfer of taka to other countries through this informal system devalues the currency leading to a fall in the consumer purchasing power and making imports more expensive within the domestic market. Consequently, inflationary pressures are exerted on essential commodities, contributing to a sharp decline in foreign reserves. Moreover, the prevalence of Hundi for tax evasion results in a fiscal shortfall for the government, thus adversely affecting the spending on public infrastructure.

To mitigate dependency on the Hundi for money transfers, Bangladesh could enact several policy measures. This includes discontinuing the Multiple Fixed exchange rates policy and adopting a Floating exchange rate. The policymakers are advised to abstain from fine-tuning, instead strengthening the market, allowing it to operate at equilibrium. A distinguished article published in the Social Science and Humanities Journal highlights that Bangladesh’s inflation rate persistently exceeds that of the United States (US) by 3 to 5 per cent, hence a gradual depreciation of taka is recommended. This would incentivise remitters to opt for legal channels as the recipient will receive more taka for an equivalent sum of dollars. Besides, higher cash incentives could be extended to encourage the utilisation of legal channels, rendering it more lucrative than resorting to Hundi. Moreover, promoting mobile banking is advocated, given its facilitation of efficient and flexible procedures. Numerous banks like Citibank, Agrani Bank, and Prime Bank have introduced their online banking services, reporting enhanced labour and cost efficiency. Additionally, initiatives by Sonali Bank and various Bangladeshi private banks to establish exchange houses in countries contributing significantly to remittances in Bangladesh can minimise the transaction costs associated with bank-to-bank transfers, as a large volume of money can be sent at once, reducing the cost per transaction. Furthermore, Governmental efforts should focus on reinforcing institutions and the judicial system to restrain criminal activities like illegal money transfers. Additionally, under-invoicing practices can be controlled through the establishment of Pre-Shipment Inspection (PSI), verifying the trade statistics, and imposing heavy fines for violations.

Syeda Nafisa Anjum and Yeashfa Haque are undergraduate students at the Department of Economics and Social Science, BRAC University. syeda.nafisa.anjum@g.bracu.ac.bd, yeashfa.haque@g.bracu.ac.bd