Bangladesh's RMG ascent: creating and climbing the dynamic smile curve

Abdullah A Dewan and Mustafizur Rahman | Wednesday, 6 May 2026

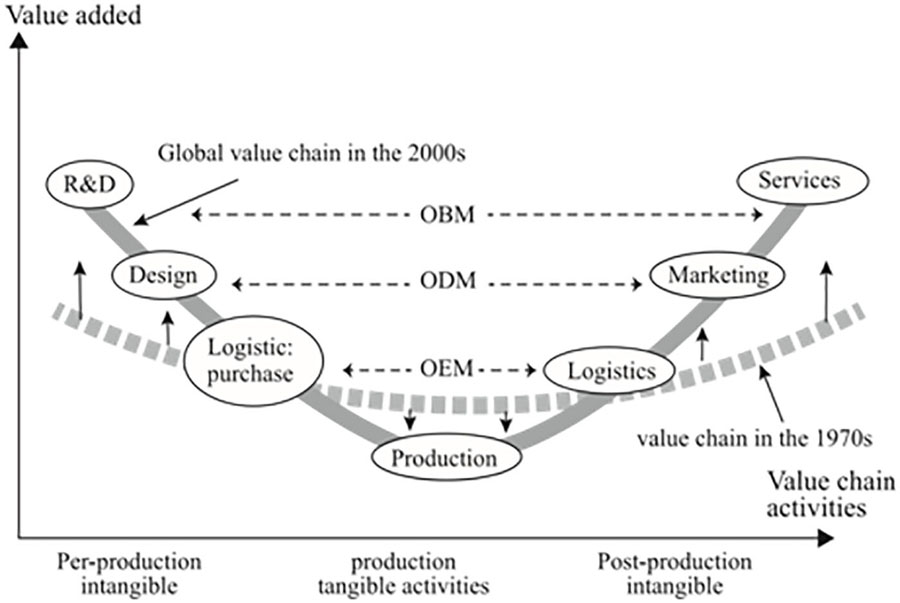

The smile curve is widely used to rank value in global production. At the two ends lie research, design, branding, and market control-the high-value segments. At the bottom lies manufacturing, often portrayed as the lowest-value activity. Bangladesh's ready-made garment (RMG) sector is therefore routinely placed at this lowest point. The conclusion seems obvious: to move up, the country must move out. This reading is widespread-and fundamentally wrong.

The problem is not with the smile curve itself, but the way it is interpreted. It is typically treated as a static ranking of activities. But production is not static. Industries evolve, productivity rises, technology improves, and firms learn. Once time is introduced, the smile curve ceases to be a picture of hierarchy and becomes a map of development.

In its simplest form, the curve is a timeline. The left side represents value created before production-research, design, and product development. The right side represents value captured after production-branding, logistics, and market control. The middle represents the stage where goods are physically produced.

That middle stage is not a dead zone. It is the most transformative phase of all. Manufacturing is not a trap; it is an entry point.

When Bangladesh entered the garment industry, it did so with limited capital, simple machinery, and an untrained workforce. Productivity was low, and value added per unit was limited. But this position was a starting point, not a permanent condition. Over time, factories expanded, workers gained skills, machinery improved, and production systems became more integrated. Backward linkages in textiles and accessories developed, lead times shortened, and compliance standards rose to global levels. Today, Bangladesh hosts many of the world's leading green garment factories. Millions of jobs have been created, female labour-force participation has expanded, and export earnings have stabilised the macroeconomy.

These changes reflect rising productivity. In economic terms, output depends not only on how much labour (L) and capital (K) are used, but on how efficiently (A) they are combined. This is captured in the production function: Y = A f(L, K), where A represents efficiency-technology, organisation, and accumulated knowledge. The history of Bangladesh's RMG sector is, in large part, the story of the rise of A through learning by doing, capital deepening, and scale expansion.

For this reason, the bottom of the smile curve cannot be flat. A flat bottom would imply no learning, no technological progress, and no economies of scale. The manufacturing segment must be seen as an upward-moving curve-one that rises as productivity and capability accumulate.

This dynamic interpretation changes how we understand industrial development. Firms do not leap from factories into global brands overnight; they move gradually along the value chain.

At the entry stage, firms operate as Original Equipment Manufacturers (OEM), producing according to foreign designs and specifications. As capabilities grow, firms begin to design products themselves-Original Design Manufacturing (ODM). At a more advanced stage, firms develop their own brands and control market access-Original Brand Manufacturing (OBM). Each step increases the share of value retained within the domestic economy.

The key is not moving away from manufacturing, but deepening within it. Building on an existing comparative advantage allows firms to climb the value chain from within rather than abandoning it prematurely. The global apparel market is approaching a trillion dollars, yet Bangladesh's share remains around 6 percent despite being the world's second-largest exporter. This gap itself is an opportunity.

This is where the contrast with successful Asian economies becomes instructive. South Korea began as a contract manufacturer but progressively internalised design, technology, and branding. Taiwan followed a similar path, evolving from assembly into high-value electronics and semiconductors. In each case, manufacturing served as the foundation upon which higher-value activities were built. The difference lies in value capture.

A country that remains confined to low-value segments generates output but retains little of the value created. Margins remain thin, capital accumulation is constrained, technological upgrading slows, and wages cannot rise sustainably. But when firms internalise design, technology, and market access, a larger share of value is retained within the economy, investment capacity increases, and productivity growth becomes self-sustaining.

This global restructuring is already underway. China-the dominant player-has been gradually shifting towards higher-end fashion, design, and technologically sophisticated segments, while also diversifying into other industries. Its share of global apparel exports has declined from roughly 37-38 per cent two decades ago to around 27-28 per cent in recent years. This has given rise to the widely discussed "China-plus-one" strategy, creating a historic opening for countries like Bangladesh, Vietnam, and India to capture additional market share.

This is where the logic intersects with a broader economic balance. When value creation expands, labour income can rise without undermining capital accumulation. Structural balance becomes feasible not through redistribution after inequality emerges, but through value capture at the point of production.

Whether this transition occurs depends not only on industrial capability but on institutional incentives. Where profits depend on productivity and innovation, firms invest in skills, technology, and organisation. Where profits depend on political access, protection, or discretionary allocation of resources, upgrading stalls and remaining at the lowest-value segment becomes a rational equilibrium. The smile curve, therefore, reflects not just industrial structure but the political economy of accumulation.

For Bangladesh, the implication is clear. The country has already demonstrated that manufacturing can transform an agrarian economy into one of the world's leading apparel exporters within a single generation.

To describe this achievement as being "stuck at the bottom" is to misunderstand both the curve and the country's development process.

The next phase does not require abandoning garments. It requires deepening them-through textile innovation, product development, digital supply-chain integration, regional branding, and more direct access to final markets. Each layer of knowledge that becomes domestically embedded raises productivity and expands value capture, shifting the curve upward.

At this stage, the path to ascent becomes operational. The sequence is cumulative. It begins with deepening manufacturing itself-raising productivity through better machinery, worker skills, and factory organisation-followed by strengthening backward linkages so that dependence on imported inputs gradually declines.

Encouragingly, domestic value addition has already risen significantly-from roughly 25 per cent in the early years to around 50 per cent today, particularly in the knitwear segment. This demonstrates that upgrading within manufacturing is already in motion, though the journey remains incomplete, especially in woven garments where import dependence is still high.

As capabilities mature, firms can move into product development and design, shifting from OEM to ODM. The next step is to develop branding, marketing networks, and direct buyer relationships, enabling the transition toward OBM and greater control over market access. At each stage, the objective is to retain a larger share of value within the domestic economy while reinvesting in technology, skills, and innovation. Competitiveness must increasingly rest not on low wages but on rising productivity.

Today, the competition is even more intense. Countries such as Vietnam, India, and Turkey are pairing competitive costs with rising productivity, stronger logistics, and expanding design capabilities.

Vietnam and India, in particular, enjoy structural advantages-Vietnam through deep integration with global value chains driven by foreign direct investment, and India through scale, domestic raw material base (especially cotton), and growing productivity. Both have also secured preferential trade agreements with major markets such as the European Union. Bangladesh, by contrast, faces a structural turning point: upon graduation from Least Developed Country (LDC) status, it will gradually lose duty-free access, facing tariffs of around 12 percent in key markets like the EU and UK. Although temporary extensions may soften the transition, the long-term implication is unavoidable-cost advantage alone will no longer suffice.

In comparison, Bangladesh still relies heavily on low wages and thin margins. This advantage is fragile: when not matched by productivity growth and upgrading, it traps firms in low-value contracts.

The risk is clear. If Bangladesh competes only on cost, it remains confined to the narrowest segment of the value chain; if it raises productivity and capability, it can sustain higher wages while expanding margins. The contest, therefore, is not low wage versus high wage, but low value versus high value.

At the same time, structural transformation may bring its own trade-offs-fewer factories, higher productivity, rising wages, but potentially slower employment growth. This underscores the importance of complementing intra-RMG upgrading with broader, extra-RMG diversification over time.

The smile curve is not a picture of where countries are. It is a map of how they move. Bangladesh is already on that path-and its future lies not in escaping garments, but in deepening them until the curve itself rises.

Dr. Abdullah A. Dewan, Professor Emeritus of Economics, Eastern Michigan University (USA); former physicist and nuclear engineer, Bangladesh Atomic Energy Commission (BAEC).

aadeone@gmail.com

Dr. Mustafizur Rahman, Distinguished Fellow at the Centre for Policy Dialogue (CPD), Dhaka, Mustafizur rahman@cpd.org.bd