LDC graduation: Bangladesh makes good progress

First of a two-part article titled Graduation out of LDC status - towards a smooth transition

K.A.S. Murshid | Friday, 12 January 2018

The Istanbul Programme of Action set a difficult goal in 2011, namely to quicken the pace of LDC graduation and reduce the number of Least Developed Countries (LDCs) by half by 2020. That goal is clearly unlikely to be met. However, a number of Asia-Pacific LDCs, including Bhutan, Nepal, Lao PDR followed by Bangladesh and Myanmar, appear to be moving quite rapidly towards graduation. Timor Leste and the Pacific Islands enjoy a relatively high income level but are beset with deep structural issues that make graduation problematic while Afghanistan remains in the reconstruction and peace-building phase which may take some more time to be resolved.

The 12 LDCs in this grouping vary enormously in terms of income, human assets, type and nature of economic vulnerability, demographic patterns, dependence on agriculture, poverty and inequality, and stage of structural transformation. Four of these are land-locked (Afghanistan, Nepal, Bhutan, Lao, PDR) and four are 'sea-locked' (Timor Leste, Solomon Islands, Tuvalu and Vanuatu). There is also enormous variation in terms of demography, socio-economics, trade, industry and agriculture.

A number of these countries were initially selected for graduation in the 2015 triennial review of the United Nations Committee for Development Policy (CDP). These are Bhutan, Nepal, Timor Leste and Solomon Islands. A few more are likely to be approved or considered for graduation in 2018 (Bangladesh, Lao PDR, Myanmar and possibly Tuvalu and Vanuatu). Curiously, apart from Afghanistan, Cambodia is the only country in the region, which is not being considered for graduation before 2030 despite already being a Low Middle-Income Country (LMIC).

Three specially designed indices have been used to asses eligibility for graduation from the LDC category, based on income, human assets and economic vulnerability: Gross National Income (GNI) per capita (which is a moving target - was set at $1242 per capita in 2015), Human Assets Index (HAI) at 66 or above and Economic Vulnerability Index (EVI) at 32 or below.

CASE OF BANGLADESH: Bangladesh has made good progress in terms of meeting all the three graduation thresholds. It has already met the economic vulnerability criteria and will almost certainly meet the income criterion by 2018. The HAI is also very close to the threshold mark and will most likely be met by 2018 as well.

Macro and trade situation of Bangladesh remains healthy with strong Gross Domestic Product (GDP) growth and poverty reduction as a result of broad-based growth. Despite recent worries about the slowdown of exports and remittances, and pressure on the domestic currency and on the balance of payments - the current account dipped into red for two consecutive years - the outlook remains very positive. Foreign Direct Investment (FDI) is beginning to rise, reserves remain comfortable, and imports are growing quickly. There are risks in fiscal and financial management and growing public debt which will need to be contained - a difficult task in an election year.

At the sectoral level, agricultural growth is slowing down, the pace of industrialisation needs to be faster with diversification and new sources of growth, which also depends on productivity, human capital development and skilling of the labour force. The short and medium-term challenges relate to lowering transactions costs, further economic reforms, investment in energy and infrastructure to create the incentives to raise private investment from 23 per cent of GDP to 28-30 per cent. The poverty rate has declined to 23 per cent. However, its main foreign exchange earnings come from the ready-made garments sector (RMG) exports and remittances, which makes the country susceptible to external shocks.

HOW SIGNIFICANT ARE LDC BENEFITS? There are three types of benefits that are most frequently discussed:

- Benefits of Duty Free-Quota Free market access (so called DFQF)

- Benefits related to concessional finance received due to the LDC status

- Benefits from an array of General International Support Measures (general ISM).

GENERAL INTERNATIONAL SUPPORT MEASURES (ISM):These are numerous, usually of minor significance and principally relates to LDC contributions to the UN budget (which is capped), some travel funds for delegates to the UN, a number of scholarships and fellowships, assistance in developing a transition strategy, research opportunities, and so on. It would not be a fruitful inquiry to indulge into a detailed case-by-case analysis of general ISM for each country, mainly due to very limited usage and access, and severe lack of data. What is clear however is that access is made difficult by complex procedures and poor information, and are often simply not worth the trouble, especially for the larger countries. There may be some relevance for these, however, for the small island states - for example, Cape Verde, Maldives and Samoa had applied for and obtained assistance in developing their transition strategy before graduation. If these measures are to have greater impact it is necessary to make these more transparent and easily accessible. Indeed, it is even difficult to find a full list of ISM measures in any one place - perhaps this is where we need to start.

CONCESSIONAL FINANCE: The world Official Development Assistance (ODA) architecture has undergone huge changes in the last 50 years. Traditional donors and multilateral bodies, including the UN, are no longer the only actors in the world of ODA. Important new actors have now emerged including South Korea, China, Russia and India. Much of the ODA is multilateral, e.g., by the World Bank, Asian Development Bank (ADB) and International Monetary Fund (IMF) - but these follow their own rules and classifications for their ODA rather than those suggested by UN. For example, the World Bank has its own classification system (low income, middle income, etc.), which it uses to decide on lending terms including concessional finance. Unfortunately, this classification does not correlate so well with the UN classification in terms of LDC, developing countries and advanced countries - which introduces additional confusion if not complexity.

Much of the ODA remains bilateral, by both the Asian donors as well as others. These flows are determined by a host of factors of which LDC status could be one - but does not have to be. In other words, 'buy-in' to the LDC classification is not as strong as it might have been (or actually was in the past).

Total ODA (gross) disbursed in 2015 was $131.4 billion (Organisation for Economic Cooperation and Development - OECD) with ODA/GNI ratio at 0.30 per cent; bilateral ODA counting for 72 per cent and the LDC and LMIC share being 25 and 21.70 per cent respectively. In other words, LDCs do appear to have a slight edge when it comes to ODA.

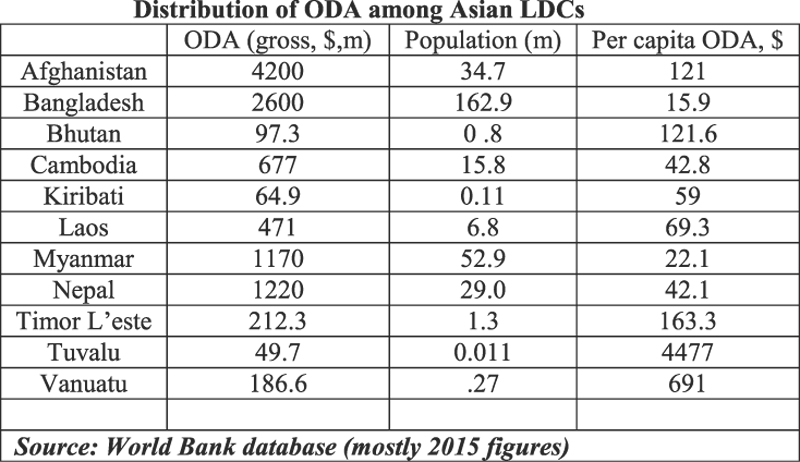

If we examine the geographical distribution of ODA, we find that the following countries were the top ten beneficiaries in 2015 (in absolute, USD terms): Afghanistan, India, Vietnam, Ethiopia, Indonesia, Pakistan, Syria, Kenya, Jordan, and South Sudan.

These 10 countries accounted for 20 per cent of total ODA. The top 20 countries accounted for 33 per cent of ODA. It is interesting to note that the only Asian LDC in this list is Afghanistan although the bulk of ODA going there is not related to its LDC status. In per capita terms, however, smaller countries tend to obtain a larger share. This is shown in the Table for the Asian LDCs.

MARKET ACCESS: Market access is probably the most important LDC benefit for members, especially those who have begun to emerge as significant exporting countries for manufactures. These tend to be the larger, non-island countries like Bangladesh, Cambodia and Myanmar. DFQF benefits have been extended to LDCs by many countries including European Union (EU), Canada, USA, China and India. However, terms like Rules of Origin (ROO) and what products will be eligible for DFQF vary considerably. Individual countries also have access to markets based on bi-lateral FTAs (free trade areas) or membership of regional groupings (like SAARC, ASEAN).

If one wants to look only at LDC benefits, this is difficult due to data limitations as countries obtain support from a number of sources for different things. These are based on different criteria and considerations emerging from regional or bilateral treaties, strategic geo-political considerations as well as LDC status - and frequently these are impossible to disaggregate.

The writer is Director General of Bangladesh Institute of Development Studies (BIDS). kasmurshid@gmail.com