Tax framework shift in FY27

NSC investors, exporters may face higher liabilities

DOULOT AKTER MALA | Monday, 15 June 2026

A structural shift in the tax collection system is likely to increase tax liabilities for national savings certificate (NSC) investors and exporters from July 1, 2026, despite no significant increase in withholding tax rates.

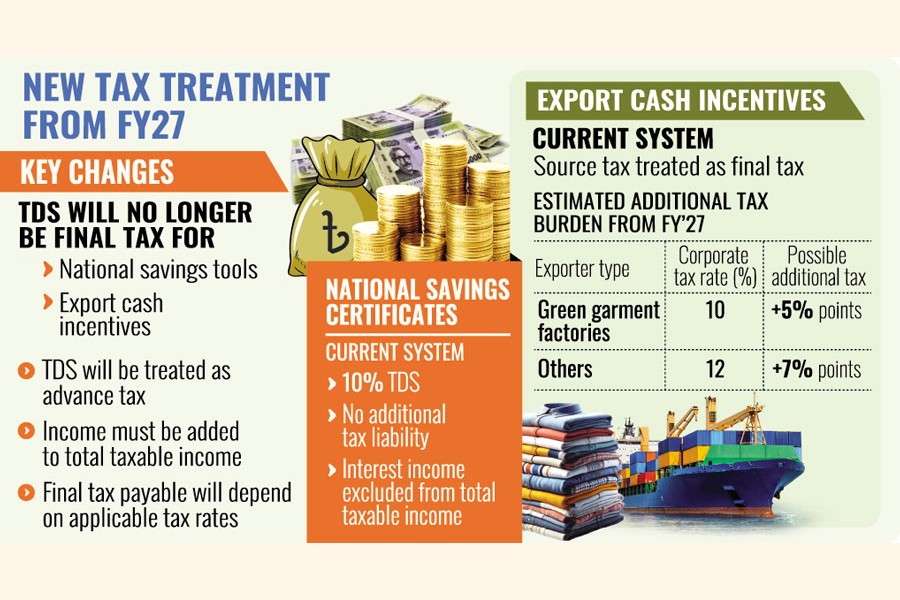

The proposed Finance Bill 2026 introduces a fundamental change by treating taxes deducted at source on certain incomes as advance tax rather than final tax.

Currently, taxpayers enjoy concessionary tax treatment on income earned from savings certificates and export cash incentives.

Such income is generally not added to their other taxable income, and the tax deducted at source is considered the final settlement of tax liability.

Under the proposed framework, however, the deducted tax will be treated as advance tax, requiring taxpayers to include the income in their total taxable earnings and pay tax according to applicable rates for individuals and companies.

The government has proposed reducing the source tax on export cash incentives from the next fiscal year.

While the move appears to provide relief, exporters may ultimately face higher tax liabilities because of the change in tax treatment.

For NSC investors, the budget proposes three major changes.

First, investors will no longer be eligible for investment tax rebates if they encash savings certificates before maturity.

Second, profits earned from savings certificates by taxpayers who have other sources of income will be taxed at regular income tax rates rather than the existing concessionary rate of 10 per cent.

Third, the tax deducted at source on savings certificate interest will no longer be treated as final tax.

At present, NSC investors are not required to pay any additional tax on interest income once the 10 per cent tax is deducted at source.

From July 1, however, taxpayers with other income sources will have to include such interest earnings in their total income and pay tax at the applicable slab rates.

Taxpayers whose only income comes from savings instruments will continue to enjoy the reduced 10 per cent tax rate and may claim refunds if excess tax has been deducted at source, says a senior tax official.

Tax expert Lutful Hadee, an accounting professional, says the government could keep the investment rebate unchanged as it is an instrument of the government's borrowing.

He, however, welcomes the restructuring of the collection method as justified.

"The government is not altering the deduction rate; they are changing the tax framework. This effectively shifts Sanchayapatra from a tax-sheltered haven into a progressive investment, meaning higher-income earners will face a larger tax bill on their savings interest," tax expert Snehasis Barua wrote in a LinkedIn post.

The removal of the final tax provision for exporters is also expected to have significant implications.

For green garment factories that enjoy a 10 per cent corporate tax rate, exporters may have to pay an additional 5 percentage points in taxes either through adjustment of advance income tax (AIT) or at the time of filing returns.

For other exporters subject to a 12 per cent corporate tax rate, the additional tax burden could reach 7 percentage points.

As a result, exporters may face higher overall tax liabilities, although they could benefit from a temporary cash flow advantage due to the lower withholding rate.

Bangladesh Knitwear Manufacturers and Exporters Association (BKMEA) President Mohammad Hatem says taxes on export cash incentives already create cash flow challenges because exporters receive the incentives after a lengthy and cumbersome approval process.

"If tax liabilities increase because of the change in the collection method, exporters will face additional difficulties," he said.

doulotakter11@gmail.com