State of the social protection system in Bangladesh

First part of the article on social protection in Bangladesh

Sadiq Ahmed | Sunday, 31 January 2021

Bangladesh has a strong tradition of caring for the poor and the vulnerable. The need for strengthening this tradition with formal publicly-funded support programmes was reinforced by the hard lessons of the 1974 Famine and the floods in the 1980s. The fight against hunger and strong commitment to poverty reduction are now core elements of economic and social policy making in Bangladesh. Yet, a coherent and systematic approach to social protection did not happen until very recently.

Over the years since the 1974 Famine, a multitude of small safety net programmes have emerged, mostly concentrated in the rural areas, to fight hunger and poverty. Many of these programmes were developed through donor assistance. Resource commitments were also made from the national budget, partly as a continuation of these donor-funded schemes.

In FY2015, there were a total of 145 safety net programmes involving Taka 308.0 billion (2.0 per cent of GDP) and administered by some 23 Line Ministries /Divisions with almost no coordination. The programmes were a mix of cash transfers and in-kind benefits involving some 80.4 million beneficiaries, which is a gross number because it does not net out beneficiaries who receive multiple program benefits. The largest share of spending accrued to the civil service pension (25.0 per cent) accounting for only 0.5 per cent % of the total beneficiaries. The remaining 75.0 per cent the safety net scheme resources were distributed to the 99.5 per cent of the beneficiaries spread over 144 other programmes. As a result, the average amount of benefit from each program and the average total benefit per family were very low.

A key objective of the social security program in Bangladesh is to focus these expenditures on the poor. Yet, the Household Income and Expenditure Survey (HIES) 2010 showed that only 35.0 per cent of the poor families reported receiving any government-funded social security benefits. On the other hand, some 40.0 per cent of the beneficiaries were non-poor. Program administrative costs were high and there were reports of considerable leakages. The combination of large exclusion and inclusion errors, leakages and high administrative costs sharply lowered the poverty impact of social security spending. Furthermore, there was no centralised database of beneficiaries and no systematic monitoring and evaluation of program implementation either at the individual program level or for the entire social security program.

ADOPTION OF THE NATIONAL SOCIAL PROTECTION STRATEGY: Faced with these tough concerns, in 2015 the government decided to adopt a major reform program that sought to overhaul the entire social safety net program into a modern social protection system. This was done through the formulation of the National Social Security Strategy (NSSS) that was adopted on 01 June 2015.

The adoption of the NSSS was a major breakthrough in social policy making in Bangladesh. It was intended that the first phase of the NSSS implementation will happen over FY2016-FY2020, to roughly coincide with the implementation of the Seventh Five Year Plan (7FYP). The 7FYP integrated the NSSS as a critical policy for reducing poverty and lowering income inequality.

The features of the NSSS are: (a) Took a strategic approach to social security by advocating the consolidation of the multitude of small and often overlapping schemes into seven core Life-Cycle based schemes; (b) Advocated the modernisation of the social protection system by the introduction of employment-based social security programmes including social pensions and unemployment insurance; (c) Called for substantial reform in beneficiary selection and program administration that uses modern ICT-based solutions, with a view to reducing transaction costs and eliminating leakages; (d) Advocated the expansion of coverage to the urban poor and the national non-poor vulnerable population; (e) Called for conversion of all programmes to cash-based; (f) Recommended the phasing away of many small schemes that did not fit into the core Life Cycle-based consolidate programmes and did not serve a useful purpose in terms of benefitting the poor and the vulnerable; (g) Advocated the establishment of an on-line grievance redressal system; and (h) Called for a strong M&E effort at both the individual program and at the full NSSS level.

TRACK RECORD OF IMPLEMENTATION OF NSSS: Available evidence suggests the implementation of the NSSS in the first five years (FY 16-FY20) since adoption in June 2015 has been patchy and weak. The Government had assigned the NSSS coordination and implementation monitoring role to the Cabinet Division. There was a long delay with startup of this implementation and monitoring role. Subsequently, with donor assistance, a formal NSSS Implementation Action Plan was adopted in 2018. This Action Plan is comprehensive and if these actions are implemented well it should help considerably in making progress with NSSS despite the time lost. The Action Plan set out a two-phased approach to the implementation of the NSSS: phase one comprising FY16-FY21 and phase two comprising FY22-FY26.

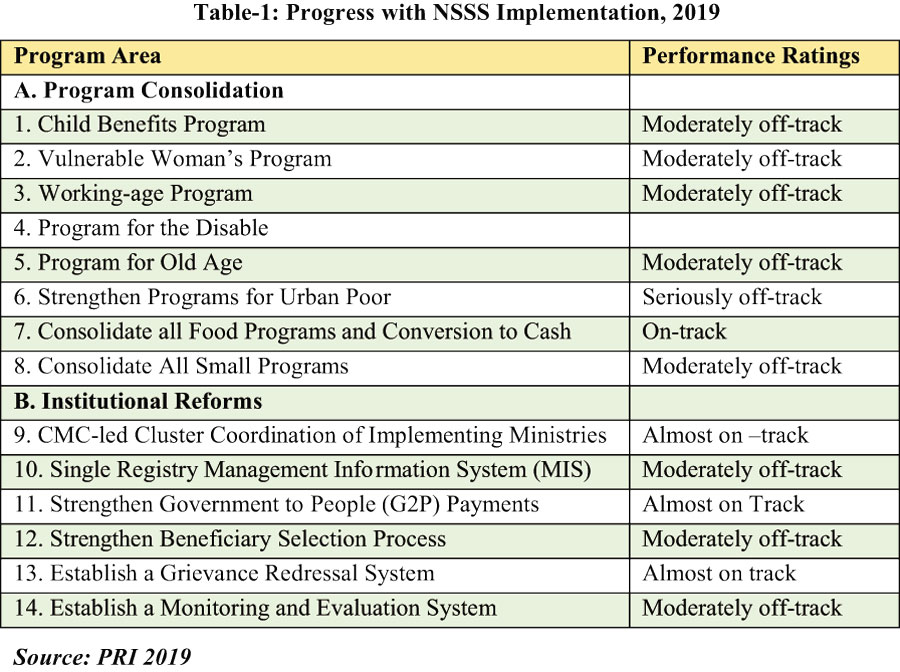

The most systematic and comprehensive review of the implementation of the NSSS and the NSSS Action Plan is done by the Policy Research Institute of Bangladesh (PRI). In addition to providing a detailed review of implementation progress by each area of reform proposed in the NSSS, the Review uses a quantitative approach to assess NSSS implementation progress based on assigning scores to the measurable indicators of progress identified in the NSSS Action Plan. A rating of "on-track" is assigned if all indicators are met; "almost on track" if substantial progress with the implementation of performance indicators is achieved; "moderately off-track" if progress is made in some indicators but majority is lagging behind; and performance is rated "seriously off-track" if little or no progress is made with implementing the indicators. The performance assessment distinguishes between (i) progress with program consolidation; and (ii) progress with institutional reforms. The ratings are summarised in Table-1. The program consolidation monitoring involves 86 indicators, of which 20 were on-track, 12 were almost on-track, 11 were moderately off-track and 37 were seriously off-track. Institutional reforms monitoring involves 50 indicators, of which 14 were on track, 3 were almost on track, 12 were moderately off-track and 23 were seriously off-track. The overall conclusion is that only modest progress was made with the implementation of the NSSS after four years of adoption. There are substantial gaps that will require major efforts.

The performance assessment distinguishes between (i) progress with program consolidation; and (ii) progress with institutional reforms. The ratings are summarised in Table-1. The program consolidation monitoring involves 86 indicators, of which 20 were on-track, 12 were almost on-track, 11 were moderately off-track and 37 were seriously off-track. Institutional reforms monitoring involves 50 indicators, of which 14 were on track, 3 were almost on track, 12 were moderately off-track and 23 were seriously off-track. The overall conclusion is that only modest progress was made with the implementation of the NSSS after four years of adoption. There are substantial gaps that will require major efforts.

Most disappointing is the fact that there are still 114 specific active social security programmes and not one single consolidated life cycle program had emerged as of June 2020. The absence of a consolidated online list of beneficiaries and the lack of a well-thought out beneficiary selection process are also major disappointments. Evaluation results of individual programmes continue to show high exclusion and inclusion errors and continued leakages. In a recent study using data from Multiple Indicator Sample Survey (MICS) 2019 [Binayak et. al. (2020)] show that a substantial share of the benefits accrues to the non-poor. This prevails even when the target group is broadly defined to include the poor and the near-poor as suggested in the NSSS. The results are summarized in Table-2.  The area where the NSSS is facing the most difficulty is the availability of resources. The financing of social security programmes has become a major challenge owing to substantial revenue shortfalls in the past three years. Contrary to expectations at the time the NSSS was formulated, budget

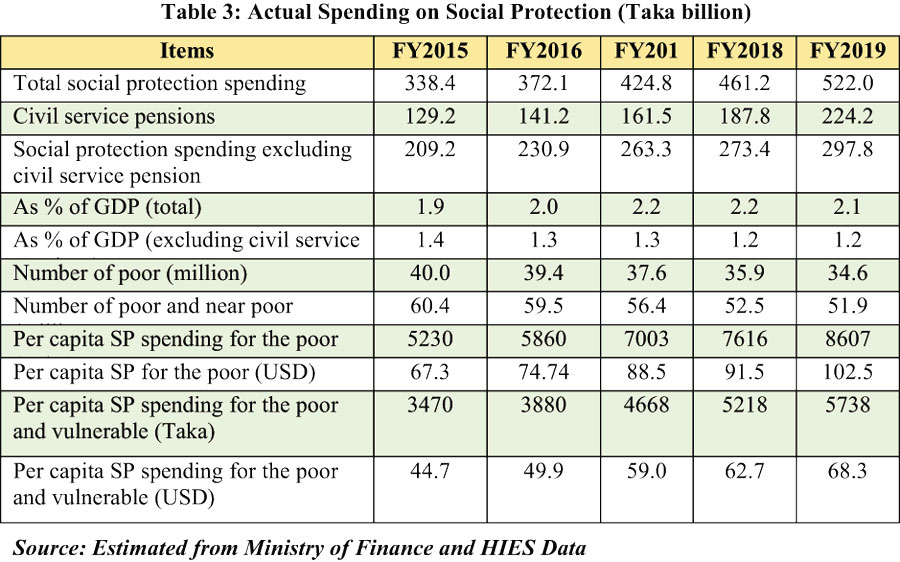

The area where the NSSS is facing the most difficulty is the availability of resources. The financing of social security programmes has become a major challenge owing to substantial revenue shortfalls in the past three years. Contrary to expectations at the time the NSSS was formulated, budget  resources have increasingly become constrained that has reduced the ability to provide higher allocations to most government programmes including social protection. While the government budgets show large planned allocations, actual financing is substantially smaller. Also, much of the actual increase in social protection spending since FY16 has happened for civil service pensions (Table-3). The large wage increases awarded to civil service employees in the FY2015-16 Budget has also translated in commensurate increases in civil service pensions. Excluding civil service pension, which accrues to only 0.6 million retirees and has very little poverty focus, total actual spending on social protection is around 1.2 per cent of GDP. Also, it is falling as a per cent of GDP.

resources have increasingly become constrained that has reduced the ability to provide higher allocations to most government programmes including social protection. While the government budgets show large planned allocations, actual financing is substantially smaller. Also, much of the actual increase in social protection spending since FY16 has happened for civil service pensions (Table-3). The large wage increases awarded to civil service employees in the FY2015-16 Budget has also translated in commensurate increases in civil service pensions. Excluding civil service pension, which accrues to only 0.6 million retirees and has very little poverty focus, total actual spending on social protection is around 1.2 per cent of GDP. Also, it is falling as a per cent of GDP.

Furthermore, there are questions regarding the inclusion of many programmes funded from the development budget in the Ministry of Finance definition of social protection. These programmes amounting to 0.20 per cent of GDP concern spending in health, education, water supply and infrastructure; it is not obvious that these spending are targeted to the poor. Even so, and taking a very liberal approach to the definition of social protection spending as defined by the Ministry of Finance, total spending excluding civil service pensions (that have little or no poverty relevance) was Tk298 billion in FY19. This is very small for a country with an estimated 35 million poor and 52 million poor and vulnerable population. In per capita terms this amounts to an annual spending of a mere Tk 8607 (US$102) per year when only the poor are included and Tk 5738 ($68) when the poor and vulnerable are included. Given the targeting errors, the actual benefits per poor person is considerably lower.

Dr Sadiq Ahmed is the Vice Chairman of the Policy Research Institute of Bangladesh. sadiqahmed1952@gmail.com