Unitholders of pooled funds managed by the ICB Asset Management Company Ltd did not receive any return on investment for FY24. FY25 is going to be as frustrating.

But the asset manager is positive about dividend distribution for the ongoing fiscal year because of the funds' recovery from losses on the back of enough provisioning and portfolio diversification in the previous two years.

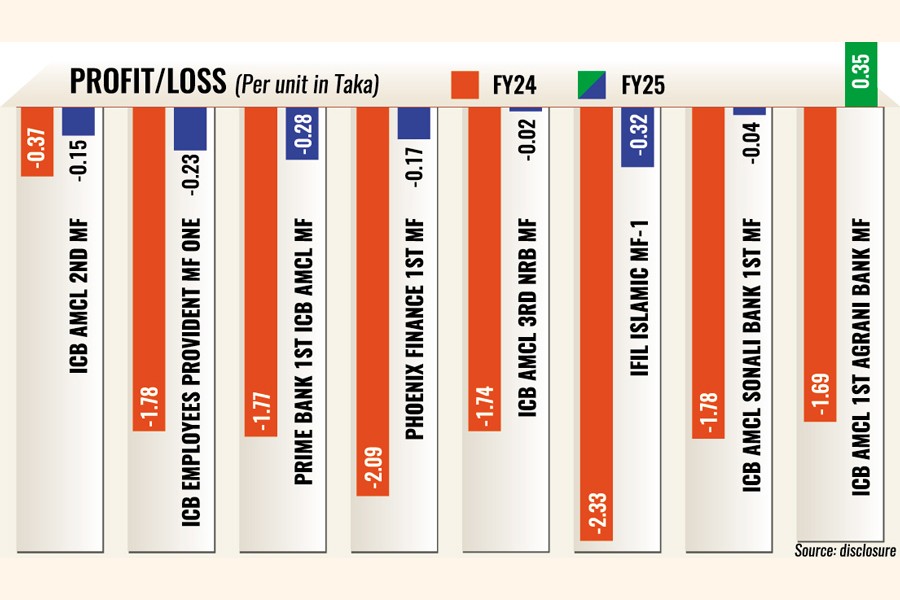

There was a disclosure on Thursday of the funds' current status, confirming that the MFs witnessed a decline in erosion of asset values in FY25, compared to the year before. One of the ICB AMCL managed funds -- ICB AMCL 1st Agrani Bank MF -- even returned to profit in FY25. It gained a profit of Tk 0.35 per unit in FY25, recovering from a loss of Tk 1.69 per unit the year before.

Another fund, ICB AMCL Second Mutual Fund incurred a loss of Tk 1.86 per unit in FY24. The loss was reduced to Tk 0.15 per unit in FY25.

The loss was inevitable in FY24 as the broad index of the Dhaka bourse lost 1,015 points in the year through June last year. The portfolios mainly consisted of equity-based securities in the year.

The funds are unable to pay dividends for FY25 as well because of the persistent fall of the equity market in the year to June this year and provisions made for the losses. The index saw erosion by 9.40 per cent or 502 points to 4,838 points in FY25.

However, the company's Chief Executive Officer Mahmuda Akhter said the provisioning that they did in FY24 helped reduce losses in FY25.

"We also reshuffled portfolios, taking positions in government securities," she said.

In fact, the company's cautionary measures started to show results -- in the financial statements for January-March (Q3), FY25.

For the quarter, many of the pooled funds reported positive earnings, a turnaround from losses in the same quarter of the previous year.

Ms Akhter said they were unhappy about not distributing any dividend to unitholders.

However, ICB AMCL is optimistic that it will pay dividends for FY26 even if the equity market remains at the current level, she said.

The provisioning supported a boost to the portfolios.

Take for example, a fund manager purchased the stock of a company at the expense of Tk 10 on October 1, 2024 and the stock price declined to Tk 7 on December 31 of the year, leading to a loss of Tk 3.

If the fund manager keeps provision of Tk 3 and the company's stock price rises to Tk 8 from Tk 7, then a provision reversal of Tk 1 will be added to the profit.

As per the rules, a pooled fund is required to invest at least 60 per cent in listed securities and the remaining 40 per cent in the money market.

But a greater portion of the portfolios of pooled funds managed by different fund managers consists of listed securities. That is why MFs endured substantial erosion in their portfolios in the last few years against the backdrop of unabated fall of the equity market.

In recent months, the stock market experienced a strong recovery. The DSEX gained 16.62 per cent or 771 points to 5,408 points between May 29 and August 7.

The CEO of ICB AMCL said their provision shortfall had been reduced by 24 per cent and the funds' net asset value (NAV) increased by 14 per cent following the recent recovery of the equity market.

mufazzal.fe@gmail.com

© 2026 - All Rights with The Financial Express