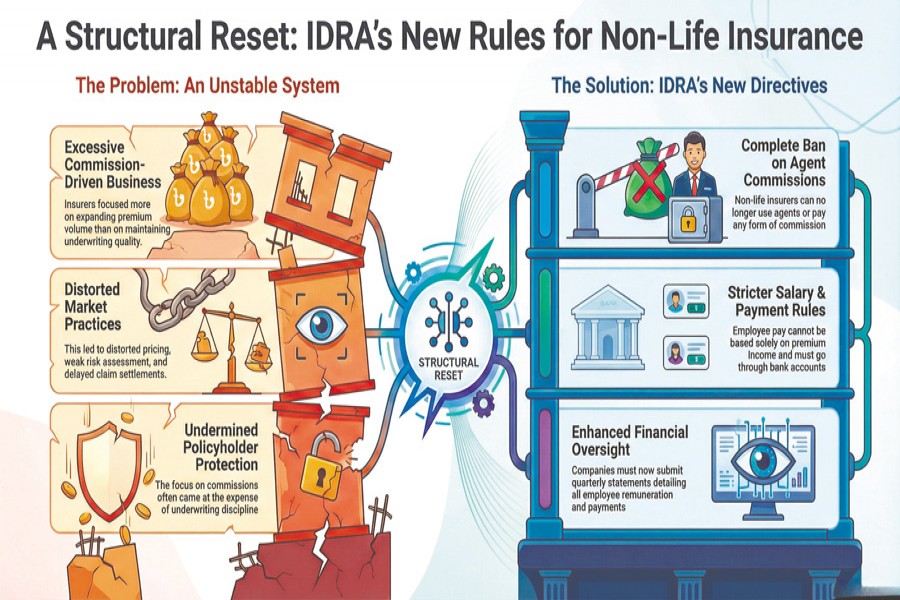

The Insurance Development and Regulatory Authority (IDRA) has imposed a complete ban on agent commissions in the non-life insurance sector, introducing stricter rules on salary and benefit payments to employees.

According to a notification issued by the regulator, non-life insurance companies will no longer be allowed to conduct business through agents. Hence, agent commissions in the sector will cease entirely from January next year.

IDRA clarified that under the Insurance Act, 2010, no insurance agent is permitted to pay or receive commission -- directly or indirectly -- in the name of any individual or institution. Any violation of this provision will invite regulatory action.

The notification also stated that salaries, allowances and other benefits of non-life insurance company officials and employees cannot be determined solely on the basis of collected premium income.

Except for risk-based investments, all investment-related benefits must be paid in line with the insurer's approved service and investment policies.

In addition, the regulator instructed that all salary, allowance and benefit payments must be made through designated bank accounts. Cash payments or any other unauthorised methods will not be permitted.

Insurance companies will also be required to submit quarterly statements in a prescribed format, detailing employee remuneration and related payments.

IDRA said the measures aim to protect policyholders' interests, strengthen financial discipline, and ensure better governance in the non-life insurance sector.

The new directives will come into effect in January.

Why agent commission has been abolished

IDRA's decision to abolish agent commissions in the non-life insurance sector marks one of the most significant regulatory shifts in recent years.

The move is aimed at correcting long-standing structural weaknesses in the market, where excessive commission-driven business has often undermined underwriting discipline and policyholder protection.

Industry insiders say commission-driven growth has been a key contributor to distorted pricing, weak risk assessment and delayed claim settlements in the segment. In many cases, insurers focused more on expanding premium volume through high commissions than on maintaining underwriting quality.

IDRA's intervention is a structural reset for Bangladesh's non-life insurance sector. While the transition may be challenging-especially for commission-dependent players-the reform could lay the groundwork for a more disciplined, sustainable and policyholder-focused insurance market in the long term.

farhan.fardaus@gmail.com

© 2026 - All Rights with The Financial Express