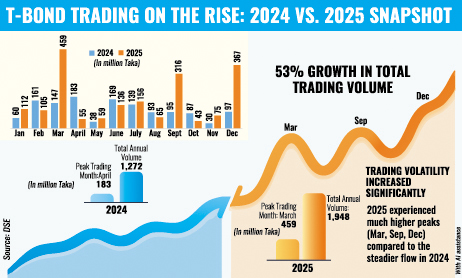

Secondary market trading in Treasury bonds surged 53 per cent year-on-year to Tk 1.95 billion in 2025, driven by falling yields and investors' preference for risk-free assets.

Bond prices are inversely related to interest rates. As a result, sellers booked capital gains, while buyers parked funds in safer instruments than equities.

In 2025, the average cut-off yields of bonds with maturities ranging from five to 20 years fell by 150 to 180 basis points over the previous year, before yield rates crossed 10 per cent again two months ago as the government's appetite for fresh funds increased ahead of the national polls.

As returns from stocks remained very low or negative amid a persistent economic meltdown and political tension, banks and institutional investors channelled their funds into government securities.

Salim Afzal Shawon, head of research at BRAC EPL Stock Brokerage, said institutional investors - including some fixed-income funds created in 2025 - had injected money into T-bonds.

"Investors consider T-bonds a better alternative to bank deposits or savings certificates. Many banks in the country are struggling with poor-quality assets, raising fears of default on interest payments."

Moreover, T-bonds offer better liquidity and tax benefits, Shawon added.

Fixed-income debt securities became more lucrative when the prime index of the Dhaka Stock Exchange (DSE) plunged 6.7 per cent, with the market capitalisation shrinking by around Tk 360 billion in 2025.

T-bond trading in the secondary market began in October 2022, offering an additional investment tool for retail investors who had previously relied mainly on stocks and mutual funds.

Although investors initially faced difficulties trading via brokerage firms, many brokerages later equipped themselves to facilitate T-bond trading and started raising awareness among general investors about the instrument.

Akramul Alam, head of research at Royal Capital, said long-term bonds, which are particularly sensitive to price and interest-rate movements, were becoming increasingly attractive to bond traders.

Bond duration indicates how much a bond's price is likely to change in response to movements in interest rates.

The rise and fall of yields depend on the government's fund requirements to meet budgetary shortfalls and the liquidity situation in banks. The policy rate set by Bangladesh Bank also influences T-bond interest rates, as banks borrow from the central bank at the repo rate - 10 per cent at present - which is the same as the policy rate.

"We have many beneficiary owners' (BO) accounts holding T-bonds, which were devoid of debt securities in the past. Investors now have better scope to exchange bond holdings, which is another reason for the higher trade volume," Alam added.

Treasury bonds are coupon-bearing long-term investment instruments with repayment periods ranging from two to 20 years. At present, there are 231 Treasury bonds listed on the prime bourse, with a face value of Tk 100 each.

EBL Securities predicts that the 10-year T-bond yield will come down to 9.5 per cent this year from 10.9 per cent in 2025.

"The bond yields may flatten in the coming months when private sector credit demand increases following the national election," said Mr Alam.

Experts say trading value is still insignificant compared to the market's potential. Still, signs have already emerged that the Tk 2 trillion Treasury bond market is expanding and helping the secondary market grow as well.

Shawon said the secondary market growth of T-bonds had remained slower than expected. T-bond trading accounted for less than 1 per cent of daily turnover on the prime bourse.

The market is capable of executing a much higher volume of trades than what was recorded in 2025. High transaction costs remain a key barrier.

At present, the commission on selling T-bonds is 0.1 per cent, while there is no cost involved when banks trade bonds among themselves in the central bank's secondary market. A parallel secondary market for Treasury bonds exists at Bangladesh Bank and has been operational for years - another reason for the lower-than-expected trading volume in the capital market.

Major traders of Treasury bonds are banks, but they are reluctant to trade through stock exchanges due to higher transaction costs.

"We expect trading of T-bonds through the stock exchanges to increase as the fixed-income instrument is gaining popularity among individual investors," Shawon said.

Alam of Royal Capital said the T-bond market would grow further as the government would have to borrow billions of taka to reduce its budget deficit.

"Our tax collection is poor. So, the government has no option other than T-bonds and T-bills to implement its budget," he added.

Most banks prefer to invest their excess funds in risk-free government securities, given weaker private-sector credit demand. Investment opportunities have shrunk in recent months because of the economic slowdown. Private-sector credit growth remained low, standing at 6.58 per cent in November, recovering slightly from the historic low of 6.23 per cent the previous month.

Well-governed banks are sitting on surplus liquidity, while the government still needs to borrow to bridge its budget deficit.

babulfexpress@gmail.com

© 2026 - All Rights with The Financial Express