Transactions through mobile financial services (MFS) continued their upward trajectory in October 2025, buoyed mainly by strong person-to-person (P2P), cash-in, and cash-out activities, reflecting sustained consumer reliance on digital platforms for daily financial needs.

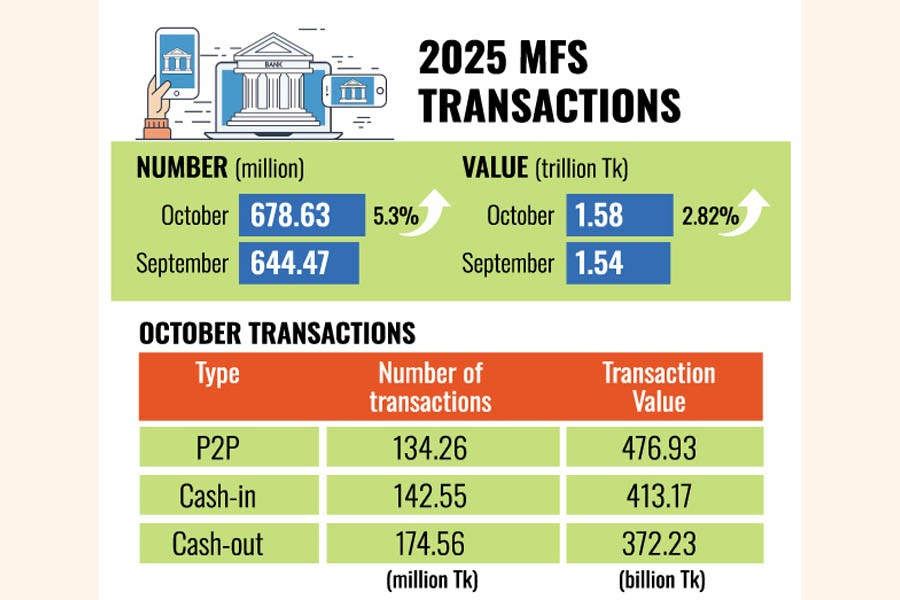

The number of MFS transactions rose by 5.30 per cent month-on-month to 678.63 million at the end of October, while the transaction value increased by 2.82 per cent to Tk 1.58 trillion, according to the latest Bangladesh Bank (BB) data.

The total value of MFS transactions reached Tk 1.54 trillion at the end of September 2025, while the number of transactions was 644.47 million.

MFS has significantly expanded financial inclusion in Bangladesh by providing accessible, secure, and convenient digital financial services to millions of people, especially in rural and underserved areas.

MFS statistics are compiled considering providers, such as bKash, Rocket, Upay, etc.

Currently, 13 MFS providers are offering different modes of services.

Due to unavoidable circumstances, Nagad has been unable to submit data since March 2025.

P2P transfers emerged as the largest segment, accounting for 30.13 per cent of the total transactions.

The number of P2P transactions was 134.26 million, with transferred funds amounting to Tk 476.93 billion at the end of October, highlighting the growing preference for instant digital transfers among users.

Cash-based services remained the dominant driver of MFS usage.

Cash-in transactions accounted for 26.10 per cent of the total value of transactions, while cash-out services made up 23.51 per cent, underscoring the sector's continued role as a key liquidity channel for households and small businesses.

The number of transactions in cash-in services reached 142.55 million, amounting to Tk 413.17 billion during the month. The number of cash-out transactions reached 174.56 million, amounting to Tk 372.23 billion.

The distribution of MFS accounts shows that both male and female accounts increased compared to the previous month.

Compared to September 2025, the number of male MFS accounts increased by 0.37 per cent to 79.61 million in October, which was 56 per cent of the total accounts.

On the other hand, the number of female MFS accounts rose by 0.35 per cent to 61.80 million, which was 44 per cent of the total accounts.

Industry insiders say the steady growth in P2P usage indicates deeper penetration of MFS into everyday transactions, including family support, small trade settlements, and informal services.

Meanwhile, inward remittances through MFS channels also posted notable growth.

In October, remittance inflows via MFS reached Tk 18.31 billion, marking a 5.85 per cent increase from September, suggesting rising confidence among expatriates and beneficiaries in digital remittance platforms.

Analysts view the October performance as a sign of resilience in the MFS ecosystem despite broader economic challenges, noting that the sector continues to play a crucial role in financial inclusion, liquidity management, and remittance distribution across the country.

They, however, caution that sustaining growth will require further improvements in service reliability, transaction security, and interoperability, alongside supportive regulatory oversight.

The continued growth in MFS transactions in October reflects the deepening integration of digital financial services into everyday economic activities.

Strong cash-in and cash-out volumes indicate that MFS remains a critical liquidity bridge for households, micro-entrepreneurs and informal businesses, says a senior executive of a leading service provider.

The steady rise in person-to-person transfers shows increasing trust in digital platforms for instant fund movement, while the growth in inward remittances through MFS highlights the sector's role in making cross-border inflows faster, safer, and more accessible, he adds.

"Going forward, our focus will be on enhancing customer experience, strengthening security, and expanding interoperable services to ensure that MFS continues to support financial inclusion and economic resilience," he notes.

sajibur@gmail.com

© 2026 - All Rights with The Financial Express