To state the obvious, an economy at any point of time has three states of being in terms of its gross domestic product (GDP): moving forward, regressing backward and standing still. As is well known, the first is designated as growth, the second is marked by recession and the third defined as stagnation. All of these sobriquets are associated with three factors: growth in GDP, inflation and employment. The ideal goldilock situation is reached when growth in GDP is positive, unemployment registers a fall and inflation does not rise. Going by recent newspaper reports, Bangladesh economy appears so volatile that it defies being pigeonholed into any of the three for a good length of time. Just when the economy appears poised to gain momentum in growth, there materialise developments in macroecomic variables that pivot to stagnation or worse. The following give the backdrop to the sense of the economy being in a state of animated suspension that is prevailing now.

To state the obvious, an economy at any point of time has three states of being in terms of its gross domestic product (GDP): moving forward, regressing backward and standing still. As is well known, the first is designated as growth, the second is marked by recession and the third defined as stagnation. All of these sobriquets are associated with three factors: growth in GDP, inflation and employment. The ideal goldilock situation is reached when growth in GDP is positive, unemployment registers a fall and inflation does not rise. Going by recent newspaper reports, Bangladesh economy appears so volatile that it defies being pigeonholed into any of the three for a good length of time. Just when the economy appears poised to gain momentum in growth, there materialise developments in macroecomic variables that pivot to stagnation or worse. The following give the backdrop to the sense of the economy being in a state of animated suspension that is prevailing now.

Inflow of remittance sent by wage earners has not only been consistent but has also registered an uptick compared to corresponding period last year. In July a total of $2.47 billion was remitted by wage earners compared to $1.91 billion for the corresponding month last year. Taking the first two months of the current fiscal, July and August, remittance increased by 18.40 per cent. In September, Bangladesh received $2.69 billion, the fifth- highest monthly inflow on record, up over 11.7 per cent year on year from $2.40 billion in September last year. The rise in remittance earnings offers a much-needed respite for the economy which has been grappling with multiple macroeconomic challenges amid a persistent foreign exchange shortage. But for this favourable development, the economy per se cannot take any credit as remittance has nothing to do with the performance of the economy. Being extraneous, it behaves independent of the growth of the economy. Having said that, it should be pointed out that the foreign exchange received as remittance contributes significantly to the growth of the economy. It should also be admitted that fiscal and monetary policy can claim some credit for sustaining the upward trend in remittance. The provision of 2.5 per cent cash incentive that adds to the amount remitted has worked well to encourage wage earners to send their earnings through official channel. Income tax exemption on amount remitted has also acted as an incentive. On the monetary side, the introduction of market-based foreign exchange rate by Bangladesh Bank since May, 2025 has allowed the rate to be aligned with the exchange rate in the curb market or that available through Hundi. With the weakening of US dollar, Bangladesh Bank started buying dollar from the market and has by now bought about $2 billion from the commercial banks. This has kept the exchange rate high enough to attract wage earners to send remittance using official channel. Had the central bank not intervened to buy US dollar, the exchange rate might have been closer to Tk 115 per dollar instead of the current Tk 121-125 range. Buying dollar from the market has also boosted the foreign exchange reserves now stands at $31.43 billion according to Bangladesh Bank estimate and $26.55 billion on the basis of IMF’s estimate of BPM6. Purchase of dollar by Bangladesh Bank has had the additional benefit of boosting the liquidity of private banks.

Though remittance has registered upward trend during the current fiscal, exports that account for greater percentage of foreign exchange earnings, have gone through ups and downs causing concern. The country’s merchandise exports recorded a 4.61 per cent fall in September year on year, pulled down by a negative growth of the largest foreign exchange earner – readymade garment (RMG). The receipt of $3.62 billion last September was below the amount of $3.80 billion earned in September 2024. The monthly export decline came for a second consecutive month, after a strong start to the current fiscal year (2025-2026) with exports posting robust double-digit growth of around 25 per cent in July when earnings reached $4.77 billion. According to analysts, the strong performance in July reflects resilience while the slowdown in August and September highlights challenges for Bangladesh’s export sector amid fluctuating global demand. But the main constraint on export of RMG is the discouragement of American buyers of RMG after the imposition of 20 per cent tariff by Trump administration. Vietnam having a lower percentage of tariffs has become a substitute destination for American buyers, it is apprehended. On the other hand, Bangladesh’s RMG exports to non-traditional markets recorded sluggish growth in the first quarter of the current fiscal, reflecting persistent global demand weakness and economic uncertainty across key economies. Besides RMG, other export items showed mixed results during the first quarter of the present fiscal year. Leather and leather products earned $319.74 million, up by 10.62 per cent year on year, though leather footwear exports fell by 9.8 per cent, reflecting pricing and competitiveness challenges in global markets. According to a newspaper report, to enable garment and other exporters in attaining competitiveness the government is contemplating waiver of value-added tax (VAT) on local procurements by exporters (The Financial Express, October 12, 2025).

From newspaper reports it is seen that Bangladesh’s current account surplus has increased, with the August 2025 figure having nearly doubled to $500 million over the previous months. The surplus has resulted from higher remittance and lower import bills. It is reported that imports fell to $6.49 billion in April, 2025, a 3.25 per cent decline from $6.71 billion in March. The imports of machinery fell by about 25.50 per cent year on year. According to Bangladesh Bank, as against $2.34 billion worth of machinery import in FY24, the import of this item last FY25 declined to $1.75 billion only, registering a 25.41 per cent fall. (Bonik Barta, August 4, 2025) Decline in intermediate goods amounted to 6.26 per cent during the same period while opening of letter of credits (L/ Cs) for raw materials declined by 0.5 per cent. Decline in import of machinery, intermediate goods and raw materials indicate weaker investment in the economy that in turn produces lower rate of growth. The decline in imports also includes food items. According to the above Bengali daily, the opening of L/ Cs for import of food items have drastically shrunk in recent months.

The above account of imports related to investment is corroborated by the state of borrowing for investments from banks and financial institutions. According to the above Bengali daily, borrowing for new investment for business and industries have almost come to a standstill. Bangladesh Bank figures show that bank loan in the private sector touched rock bottom in June this year. In the month of July, bank loans for business and industries were in the negative territory. While bank loan for private sector in June was Tk 17.47 trillion, the figure amounted to Tk 17.40 trillion in July. To combat inflation, Bangladesh Bank had put the ceiling on private sector lending growth at 9.8 per cent during last fiscal. As against the target, achievement was only 6.5 per cent. The modest target of 7.2 per cent private sector credit growth fixed for the current fiscal year seems unlikely to be met, judged by the record of borrowing during the first quarter of the fiscal. On the basis of imports of machinery etc for investment and low level of borrowing for business and industries it can be concluded that investment in private sector is not conducive for growth. Needless to say, this has implications for the employment market.

Public sector investment under the annual development plan (ADP) is also lacklustre. The implementation of ADP during the first two months of the new fiscal has been only 2.57 per cent, indicating the chronic bureaucratic inertia. Among other constraining factors is the poor collection of public revenue. Till August this fiscal, Tk 271.52 billion have been collected as revenue against the target of Tk 308.89 billion. The shortfall in revenue collection has become chronic and is not likely to go away any time soon, constraining fiscal space for public sector investment.

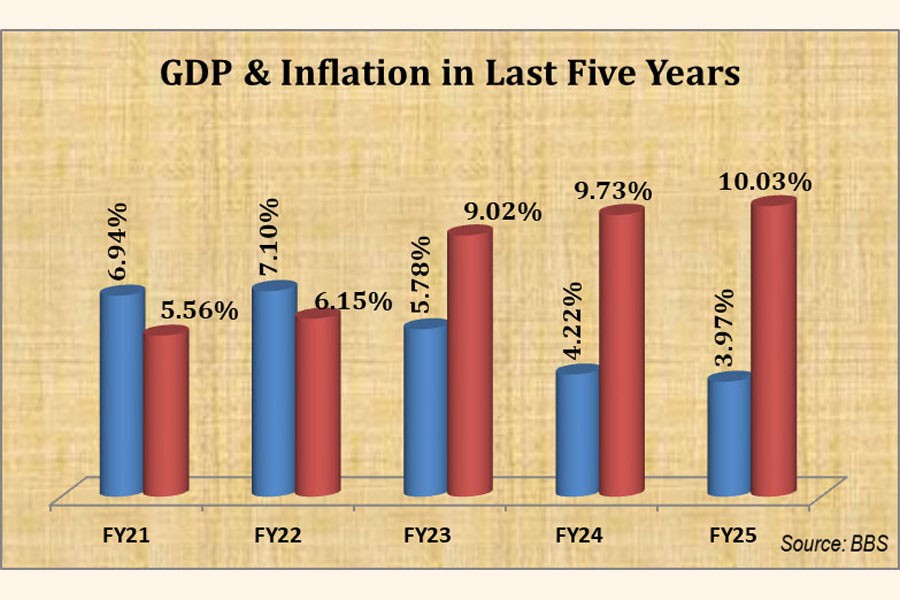

News on the inflation front has not been anything to cheer about. It has stubbornly remained at or near about 9 per cent for the last one year. The rate of inflation on a point to point basis was recorded at 8.36 per cent in September last, 0.07 percentage points higher than 8.29 per cent in August. In the corresponding period during last fiscal year, inflation was at 9.92 per cent. Despite a contractionary monetary policy that has seen policy rate (repo) of central bank’s lending to banks rise from 5 to 10 per cent and deregulation of commercial bank’s lending rate at 6 per cent, it has so far been unsuccessful to bring down inflation to the targeted level of 5.5 per cent through monetary policy.

In the current budget, deficit has been proposed to be narrowed to 3.6 per cent of GDP. In his budget speech the finance advisor assured that although the expenditure on principal and interest payment of foreign loans increased due to the huge depreciation of Taka against Dollar, the overall budget deficit would be at a tolerable level during fiscal 2026. Against this optimistic scenario sketched in the budget the reality check is: Bangladesh debt-to-GDP ratio has climbed nearly 11 per cent over the past decade, reaching 37.62 per cent in FY25. The IMF has projected that the ratio could reach 40.03 per cent by the end of 2025. With a tax-GDP ratio hovering around just 7.4 per cent, the country continues to rely heavily on borrowing rather than on internal revenue generation. Of the 37.62 per cent debt-to-GDP ratio during FY25, around 21.52 per cent came from domestic sources (banks and savings certificate) while 16.10 per cent came foreign lenders. Given this reality it will be nothing short of a miracle to bring the debt-to-GDP ratio to 36.2 per cent of GDP. According to the Bengali daily mentioned above, about 89 per cent of foreign loan have been used for repayment of debt liability during the first two months of the current fiscal year. (Bonik Barta, September 29, 2025).

Before the pandemic, Bangladesh economy posted a hefty growth rate of 8 per cent which, after making allowance for official hubris, was reasonably estimated at over 6 per cent. The recessionary impact of the pandemic brought the growth rate down to 3.7 per cent in FY21 from which its recovery was made slow, first, by the global supply chain disruptions and subsequently by the economic shock of the Ukraine war. In the budget of FY26 the growth rate of 5.5 per cent has been targeted even though the GDP posted less than 4 per cent growth at the end of the FY25. The World Bank in its latest ‘Bangladesh Update’ has estimated this fiscal year’s GDP growth rate at 4.8 per cent and expects it to rise to 6.3 per cent next fiscal. The upbeat report says, ‘The real GDP is projected to increase by 4.8 per cent in FY2026, an improvement from FY2025 but still below the past 10-year average of 6.3 per cent’. The increase is anticipated to be supported by a gradual recovery in private consumption as inflationary pressure eases. About investment, the World Bank Update says that private investment growth is ‘expected to recover by marginally to 1.9 per cent in FY2026, remaining well below its last decade’s average of 7.4 per cent.’ Persistent policy uncertainty surrounding the national election and fragilities in the banking sector are likely to weigh on private-sector activity, the Update cautions. Similarly, ‘public investment growth is likely to remain subdued ahead of the election and in the light of the authorities’ intent to implement development projects ore prudently’, the Update adds. The downsides that may compromise the projected growth have also been mentioned in the report which include: further banking - sector weakness, heightened political instability around the election, shortfalls in reform implementation, international trade disruptions from policy uncertainty, persistent inflation, and energy-supply constraints.

Apart from the fact that only some reforms in the banking sector have been initiated (merger of five sick banks, restructuring the boards and independence of the central bank), all the rest of the downsides have a high probability of becoming real, not least because of the lame duck status of the interim government. This probability makes the World Bank estimate and projection highly problematic. A week after the World Bank Update was made public The Financial Express quoted data from Bangladesh Bureau of Statistics (BBS) showing GDP growth at constant prices slipped to 3.35 per cent in Q4 (April- June) compared to 4.86 per cent in Q3 and 4.48 per cent in Q2 (FE, October 10, 2025).This means macroeconomic variables being in a mismatch all bets are off, including those used by the World Bank. Just as policies cannot be formulated in a political vacuum, projections can only be reasonably realistic in a situation of political certainty. This does not mean that projections and estimates cannot be made in periods of political transitions. These exercises can take place to justify the existence of institutions and experts but what is important is to remember that their worth is no more than fortune telling by reading tea leaves.

The combined impact of slow rate of growth, lesser employment opportunities ( three million new unemployed) and persistent inflation in recent years have worsened the poverty situation in Bangladesh. According to World Bank (WB) Update, extreme poverty may reach 9.3 per cent this year, increasing from the present figure of 7.7 per cent. On the basis of its estimate, absolute poverty rate in FY26 may increase by 0.7 per cent raising the poverty rate to 21.2 per cent. The percentage of poor this fiscal estimated by BBS is 19.2 per cent which is close to the WB figure. The estimate made by Power and Participation Research (PPRC), based on a recently carried out survey, puts the figure higher, at 28 per cent, an increase of 9.3 per cent (Bonik Barta, October 8, 2025). There may not be unanimity on the scale of increase but all three sources point to increase in the incidence of poverty which is a reversal of success in poverty reduction in the recent past.

To sum up, despite posting a real GDP growth rate of 4.6 per cent, Bangladesh economy, figuratively speaking, appears to be in a state of ‘animated suspension’. In this state, the economy is visibly active but internally strained. The high inflation rate of 8.4 per cent continues to erode household purchasing power, dampening benefits of economic growth. While key macroeconomic indicators suggest momentum, the everyday reality for the majority reflects stagnation, even deterioration in their standard of living. With growing unemployment and wages lagging behind price increases of essential consumer goods, the middle class and poor have been hit hard. With fiscal space constrained, the government is unable to adopt Keynesian ‘pump-priming’, taking up the slack in private sector investment and creating jobs for the unemployed. This creates a paradox where the economy is neither in full crisis nor in robust recovery — suspended between forward motion and structural inertia. Without targeted intervention to address inflation and boost productivity, this fragile balance may tip toward deeper economic stress giving rise to stagflation risk or incipient stagflation. To put it differently, Bangladesh economy is experiencing a growth-inflation mismatch where output is expanding at a slow rate and real income is being eroded by rising prices. Technically, this is not stagflation as GDP is growing, albeit at a slow rate. But the persistence of inflation and increasing unemployment along with slow growth indicates that the economy is facing a new territory — incipient stagflation.

hasnat.hye5@gmail.com

© 2026 - All Rights with The Financial Express