A bank staff is counting notes —FE File Photo

A bank staff is counting notes —FE File Photo  Bangladesh is on the brink of a full-scale banking crisis, exacerbated by economic stagnation and political upheaval following the collapse of the Sheikh Hasina regime. At the heart of this crisis lies a banking sector plagued by skyrocketing non-performing loans (NPLs) and pervasive financial mismanagement.

Bangladesh is on the brink of a full-scale banking crisis, exacerbated by economic stagnation and political upheaval following the collapse of the Sheikh Hasina regime. At the heart of this crisis lies a banking sector plagued by skyrocketing non-performing loans (NPLs) and pervasive financial mismanagement.

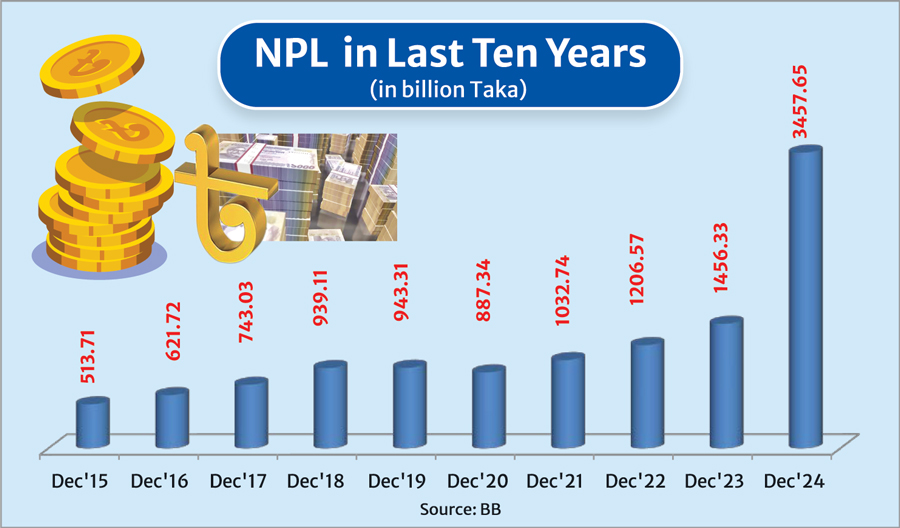

Last week, Bangladesh Bank disclosed a sharp increase in classified loans, surging from Tk 2.45 trillion in September to Tk 3.45 trillion in December 2024. Consequently, the NPL ratio jumped from 16.9 per cent to an alarming 20.2 per cent within just three months. In global finance, an NPL ratio exceeding 10 per cent signals severe distress, often necessitating immediate regulatory intervention.

A SECTOR ON THE VERGE OF COLLAPSE: Most of the country's 62 scheduled banks-including six state-owned commercial banks, three specialized banks, and 43 private banks-are in crisis. State-owned banks now report an unprecedented 42.8 per cent NPL ratio, while private banks struggle at 15.6 per cent - clearly far beyond acceptable thresholds.

As of December 2024, Janata Bank held the highest soured loan ratio among the state-owned banks, with 66.8 per cent of its total loans classified as defaults. Some of its largest defaulters included top business conglomerates like Beximco and S Alam Group.

High NPL ratios erode bank earnings, destabilise balance sheets, and weaken financial institutions' ability to meet depositor demands-classic precursors to systemic financial collapse. The 2007-2008 global financial crisis followed a similar trajectory of unchecked bad loans.

Worse still, Bangladesh Bank governor Ahsan Mansur warned last week that the NPL ratio could soon reach 35 per cent, attributing the crisis to widespread corruption and systemic looting over the past 15 years. Citing combined loans of Tk 2.5 trillion issued to S Alam Group and Beximco, he remarked, "Nowhere else have so many banks been looted at once." He further warned that with 12 banks under audit following board dissolutions, the true extent of NPLs may be even higher and that some banks may not survive.

Worse still, Bangladesh Bank governor Ahsan Mansur warned last week that the NPL ratio could soon reach 35 per cent, attributing the crisis to widespread corruption and systemic looting over the past 15 years. Citing combined loans of Tk 2.5 trillion issued to S Alam Group and Beximco, he remarked, "Nowhere else have so many banks been looted at once." He further warned that with 12 banks under audit following board dissolutions, the true extent of NPLs may be even higher and that some banks may not survive.

THE MAGNITUDE OF THE CRISIS: When Sheikh Hasina assumed power in 2009, NPLs stood at Tk 224.82 billion. By September 2024-immediately after her removal-this figure had skyrocketed past Tk 2.84 trillion, excluding Tk 640 billion in written-off loans. Trillions more were rescheduled or restructured to obscure the crisis's actual scale. The International Monetary Fund (IMF) estimates that over a quarter of all disbursed loans-more than Tk 5 trillion-are in distress.

Bangladesh has long maintained one of South Asia's highest NPL ratios. Between 2012 and 2021, Bangladesh's NPL ratio averaged 8.16 per cent, second only to Pakistan's 10.32 per cent. By comparison, India and Sri Lanka had lower rates of 7 per cent and 3.94 per cent, respectively. Sri Lanka's NPL ratio in 2022, however, rose to 12 per cent amid a prolonged political crisis.

Moreover, the Hasina regime encouraged loan defaulting by manipulating classification guidelines to mask the true scale of bad loans. Previously, loans were categorised as "classified" if principal or interest remained unpaid, even if not overdue, and a loan was formally recognised as a "default loan" after six months of non-payment. However, in 2019, the Hasina government weakened this standard by granting borrowers an additional six-month grace period following an initial three-month overdue period-effectively delaying default classification until nine months of non-payment.

A LEGACY OF CORRUPTION AND MISMANAGEMENT: Bangladesh's banking sector has long been a breeding ground for corruption, attracting unscrupulous actors who amassed immense wealth at taxpayers' expense. While the problem has escalated to unprecedented proportions in recent years, its roots can be traced back to the immediate aftermath of liberation war, when the entire banking system was nationalised and placed under inept administrative and political control.

Over the decades, nationalised banks were systematically mismanaged for political gain, rewarding loyal cronies along the way. The introduction of private-sector banking since the 1980s did little to curb corruption, as politically connected businessmen continued treating banks as personal cash reserves rather than institutions of financial responsibility.

During Hasina's 16-year rule, banks were plundered by politically connected elites, exacerbating capital flight through illicit mechanisms such as hundi, over-invoicing, and trade mis-invoicing. Reports estimate that Bangladesh loses $3.1 billion annually to illicit financial flows.

A White Paper released by the Interim Government estimates that under Hasina's tenure, an average of $16 billion was siphoned off annually. At its unveiling, Professor Yunus lamented, "Our blood curdles to know how they plundered the economy. The saddest part is they looted the economy openly, and most of us lacked the courage to confront it."

BANGLADESH BANK'S RESPONSE: Taking charge of the financial sector in deep troubles, governor Mansur last November mandated that all overdue loans be classified as NPLs after three months instead of six. This policy, set to take effect in April 2025, aligns with IMF standards under the conditions of Bangladesh's $4.7 billion loan agreement. As part of this deal, he also committed Bangladesh Bank to reduce NPLs to 8 per cent by June 2026.

However, the contradiction at the heart of this policy is glaring: shortening the NPL classification period will inevitably inflate the reported NPL ratio. How, then, does Bangladesh Bank intend to cut NPLs from over 20 per cent to 8 per cent within such a short window? The target appears not just unrealistic but outright delusional. The authorities are thus clearly setting themselves up for inevitable failure-risking further damage to an already fragile banking sector.

In the meantime, Bangladesh Bank has aggressively restructured over a dozen struggling banks, including those tied to the scandal-ridden S Alam Group. In a recent virtual session, central bank governor warned that 10 more commercial banks were on the brink of collapse and that some may fail. While such transparency is a welcome departure from past denialism, without concrete, pragmatic solutions to restore stability, these warnings may fuel panic rather than confidence in a banking sector already on the verge of collapse.

Reports indicate that Bangladesh Bank is considering establishing bridge banks-temporary entities to take over failing institutions-along with a Bank Restructuring and Resolution Fund, supported by government contributions and international lenders. While these measures aim to stabilise the sector, they raise serious concerns. Bridge banks offer only a short-term fix, often plagued by inefficiencies and weak depositor confidence, which could worsen instability. Meanwhile, reliance on government funds and external aid risks depleting public resources, increasing debt, and exposing the country to restrictive lender conditions. Rather than providing lasting solutions, these initiatives may merely postpone an inevitable financial reckoning.

REFORM OR RUIN: Bangladesh's banking sector has devolved from mere inefficiency into a hub of corruption, money laundering, and financial fraud. What was once a state-controlled system designed to serve the public has been hijacked by political elites, prioritising their own interests over economic stability. Rampant mismanagement and regulatory complacency have turned the sector into a liability rather than an asset for the nation.

Restoring credibility demands more than superficial reforms-it requires a complete overhaul, strict accountability, and a decisive break from the entrenched culture of financial exploitation. Without bold action, the sector risks sinking further into dysfunction and systemic collapse. Here are some suggestions that policy makers may consider.

First, without reducing NPLs, improving banks' capital adequacy is impossible. Over a decade, state-owned banks have consistently failed to meet minimum capital requirements, with NPL ratios averaging over 20 per cent. Specialised banks, in particular, remain critically undercapitalised. Yet, instead of enforcing discipline, Bangladesh Bank has repeatedly bailed out these failing institutions-at taxpayers' expense and under political directives.

This cycle of barefaced financial misgovernance has not strengthened the banking sector; it has entrenched its weakness. The time for half-measures is over. The state must stop propping up insolvent banks and let market forces determine their fate. A failing bank should fail-prolonging its existence through endless bailouts only deepens systemic inefficiency and corruption.

Second, privatisation of perenniaally losing state-owned banks is an unavoidable imperative to eliminate political patronage and entrenched corruption and mismanagement. It is, understantably, an ambitious task that the interim government may not have the capacity to fully implement, but it can certainly initiate. A logical starting point would be Janata Bank, which is sinking fast under the weight of corruption, mismanagement and bad loans.

Third, while full-scale privatisation may be beyond the scope of the interim government, at the very least, it can insist on professionalising bank management, severing it from the grip of bureaucratic incompetence and partisan loyalty. This requires accountability-holding those responsible for the financial collapse to criminal justice, whether their crimes stem from negligence, favoritism, or outright embezzlement. Unfortuntely, the interim government has so far shown little inclination to pursue such a course.

Fourth, the Interim Government must urgently overhaul Bangladesh Bank. A politicised and compromised regulator cannot fix the system it helped destroy. The institution needs a complete reset-governed by an independent board of proven experts, each overseeing critical policy areas, under a respected, impartial chairman. Leadership must be earned through merit and expertise, not bureaucratic inertia or political patronage. Without this fundamental restructuring, any attempt at financial reform will be nothing more than a facade, perpetuating the same dysfunction that brought the sector to the brink of collapse.

Ultimately, Bangladesh's financial recovery hinges on a fundamental transformation: a banking system that serves the people, not the powerful elites.Without this seismic shift, the nation's economy will remain shackled to the very predators who drove it to the edge of collapse.

Dr CF Dowlah is a retired professor of Economics and Law in the United States. Currently he serves as Chair, Bangladesh Institute of Policy Studies (BIPS).

Chair-BIPS@bipsglobal.org

© 2026 - All Rights with The Financial Express