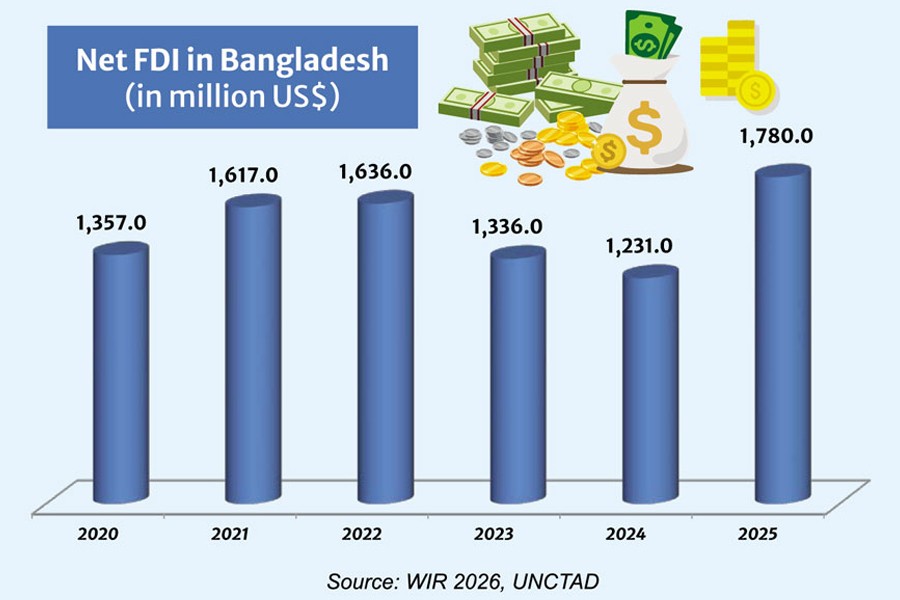

When UNCTAD released its World Investment Report 2026 on July 7, the headline appeared encouraging. Foreign direct investment (FDI) in Bangladesh rose 45 per cent in 2025, reaching $1.78 billion — the fastest growth rate in South Asia and the first significant recovery after two consecutive years of decline.

Yet the headline tells only part of the story. Bangladesh, an economy of more than 170 million people with a gross domestic product (GDP) exceeding half a trillion dollars, still attracted less foreign investment than Uganda ($3.4 billion), and roughly the same as Ghana and the Democratic Republic of Congo (about $1.9 billion each) — economies a fraction of its size. It also received slightly less than Pakistan ($1.85 billion), despite Pakistan’s far deeper macroeconomic distress in recent years. India, by comparison, attracted nearly $39 billion. These comparisons are imperfect given differences in scale, but they point to an uncomfortable reality: Bangladesh continues to occupy a modest position in global investors’ calculations.

The more important question, then, is not why FDI rose in 2025, but why it remains so low relative to the country’s potential. Investors commit capital not because of last year’s growth figures, but because they believe a country offers predictable returns over the next decade. Confidence is shaped less by temporary improvements in macroeconomic indicators than by expectations about policy consistency, institutional quality, and financial stability. Viewed this way, the rebound signals that existing investors remain willing to stay — not that Bangladesh has regained the broad-based confidence needed to attract a new wave of long-term investment.

recovery driven by existing INVESTORS not renewed confidence: A closer look at the 2025 data reinforces this distinction. Much of the increase came not from new multinational entrants, but from firms already operating in Bangladesh choosing to reinvest earnings rather than repatriate them. Reinvested earnings show that existing operations remain commercially viable; they do not show that Bangladesh has become substantially more attractive to investors who have yet to arrive.

Greenfield investment — the kind that builds new factories, transfers technology, and generates the largest employment gains — remains comparatively weak, and FDI continues to account for less than 0.4 percent of GDP. The comparison with Uganda and DR Congo should also be read carefully: their 2025 numbers were driven by exceptionally large oil, gas and mining projects that reflect natural-resource endowment as much as investment policy. Bangladesh’s challenge is different — its competitiveness depends on manufacturing, modern services, logistics and export-oriented production, precisely the sectors where investment momentum has yet to recover.

In short, existing investors are staying, but many potential investors are still waiting. Understanding why matters more than celebrating one improved year.

The confidence gap: International investors weigh expected returns against long-term risk, and several reinforcing risks currently widen that gap for Bangladesh.

The first is institutional credibility. Investors can adapt to high taxes or complex regulation provided rules are predictable and consistently applied. What discourages investment is uncertainty over how policy will change or whether commitments will be honoured. Political stability following the recent transition has removed one source of uncertainty, but stability alone does not automatically produce confidence; investors seek institutional continuity beyond political cycles.

The second is the health of the financial system. According to Bangladesh Bank’s Financial Stability Report 2025, the banking sector recorded its first system-wide net loss in over a decade, driven by a sharp deterioration in non-performing loans. For investors, this raises concerns well beyond credit access — it touches liquidity, exchange-rate management and payment reliability, making the banking crisis an investment issue, not merely a financial one.

A third concern is productive competitiveness. Bangladesh’s traditional advantages — competitive labour costs, a large domestic market, strategic location — have been eroded by persistent constraints in energy supply, logistics and the cost of doing business. Investors still navigate multiple agencies before projects become operational, and as wages rise, low-cost labour alone can no longer sustain competitiveness.

Recent disruption to global energy markets illustrates how external shocks compound these domestic constraints. Tensions around the Strait of Hormuz have curtailed LNG supplies, forcing some textile manufacturers to cut production. Geopolitical shocks are beyond the government’s control, but resilience to them is not — and investors watch that resilience closely.

The composition of external financing adds another signal. Over the past five years, Bangladesh received about $7.6 billion in net FDI, against more than $40 billion in external borrowing — roughly five and a half times as much. Debt must be serviced regardless of performance, while equity investors share the risk and often bring technology and managerial expertise. When debt grows far faster than equity, it typically reflects greater willingness among investors to lend than to own — a meaningful signal about how they perceive Bangladesh’s risk.

None of these challenges is individually insurmountable, but together they shape the cumulative risk premium investors attach to the country — and that premium, not any single indicator, is what ultimately distinguishes sustained investment from cautious, incremental capital.

domestic investment matters even more: Foreign investment draws public attention, but Bangladesh’s growth depends even more on domestic investor confidence — private investment accounts for nearly a quarter of GDP, far more than FDI. Domestic investors know the regulatory and financial environment better than any foreign entrant; when they hesitate, foreign investors take notice and rarely move ahead regardless.

That hesitation is visible. Private investment as a share of GDP has stagnated, and private-sector credit growth has fallen to historic lows — signs of a broader reluctance to commit capital amid uncertain financing conditions and energy reliability. The consequences are increasingly visible in the labour market: overall unemployment remains low by international standards, but graduate unemployment has risen steadily, with nearly 900,000 graduates now estimated unemployed. This is a structural imbalance — the economy still generates jobs, but not enough high-productivity, formal-sector positions for an increasingly educated workforce, precisely because too few new firms are being built.

Restoring confidence, then, is not only about attracting foreign capital; it is about reviving the investment cycle across the whole economy. Domestic and foreign investment reinforce each other — strong domestic investment signals confidence that draws foreign capital, while foreign investment brings technology and market access that strengthens domestic firms.

Restoring confidence: Investors do not commit long-term capital because governments promise reform; they invest once reforms are implemented consistently. Three priorities matter most.

Institutional credibility comes first. Bangladesh has introduced one-stop services and regulatory reforms through BIDA, but investors still report lengthy approvals and overlapping requirements across agencies. The task now is ensuring existing reforms function in practice, not designing new ones.

Confidence in the financial system comes second. Resolving non-performing loans, strengthening bank governance and recapitalising viable institutions should be national priorities, alongside maintaining stable foreign-exchange management so businesses can access trade finance reliably.

Productive competitiveness comes third. Reliable energy, modern logistics, efficient ports and digital public services matter more than labour costs alone going forward. The Hormuz-linked disruption underscores the need for diversified energy imports and expanded storage capacity.

These priorities reinforce one another — stronger institutions support a healthier financial system, which supports productive investment and higher-quality employment. Rebuilding this kind of credibility takes years, not months: currency or rate adjustments can shift sentiment within months, but institutional trust is earned through reforms that survive changes in political leadership. Bangladesh does not need to convince investors of its economic potential — its growth record already does that. The task is demonstrating that its institutions can deliver stability and predictability over the long term.

A reform window: One deadline deserves attention. Bangladesh was scheduled to graduate from Least Developed Country (LDC) status in November 2026, but the government has requested a three-year postponement, citing the pandemic, geopolitical shocks, financial-sector weaknesses and the political transition as disruptions to its preparation. The proposal has received positive consideration, though the final decision rests with the United Nations.

Whether graduation occurs in 2026, 2029, or in between matters less than what should not become the central debate: an extension buys time to strengthen institutions, but it does not by itself improve the investment climate. Its value depends entirely on how that time is used.

Bangladesh’s fundamentals — a large domestic market, a young and increasingly skilled workforce, a dynamic export sector — have not disappeared. What has weakened is investors’ confidence that institutions can consistently convert those strengths into predictable returns. The real test after these encouraging UNCTAD figures is not whether Bangladesh attracted more FDI in 2025, but whether it can show, through consistent policy, sound financial governance and effective institutions, that this rebound marks the start of a sustained investment cycle rather than a temporary recovery. Rebuilding that belief is now Bangladesh’s most important economic task.

Thus, Bangladesh’s latest FDI figures offer cautious optimism, but sustainable investment will depend less on short-term inflows than on restoring confidence through credible institutions, financial stability, and consistent reforms.

Golam Rasul is a Professor of Economics at the International University of Business Agriculture and Technology (IUBAT), Dhaka.

golam.grasul@gmail.com

© 2026 - All Rights with The Financial Express