Before the budget speech, there was an expectation, encouraged by the finance minister’s pre-budget remarks, that the government would offer a candid accounting of the fiscal inheritance: a banking sector carrying the world’s highest non-performing loan ratio, private-sector credit growth near a multi-year low, inflation stuck above 9 per cent, and revenue collections running far below target. That accounting did not materialise.

Instead, the budget for the fiscal year 2026-27 was framed around forward-looking intentions. The finance minister acknowledged “challenges” in general terms but chose not to present a detailed public autopsy of FY2025-26. For a government fewer than four months old, the political logic is understandable. But the analytical gap is real: without a clear-eyed diagnosis of what went wrong, and what structural constraints remain, the budget’s promises risk floating free of the conditions they must operate within.

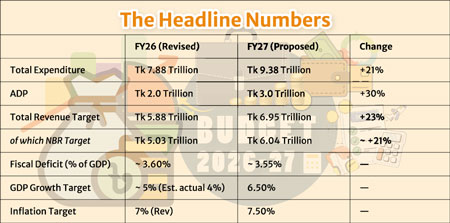

The deficit of 3.55 per cent of gross domestic product (GDP) is below the conventional 5 per cent threshold — an improvement on paper. Whether it holds depends on two things: whether revenues are collected and whether expenditure is contained. The budget was more confident about the former than circumstances warrant.

The National Board of Revenue (NBR) would need to increase 50 per cent of its actual tax collections, not its stated target, but what it has actually been collecting, to hit the FY27 revenue goal of Tk 6.04 trillion. In a country where the revenue authority has never met its target, this is the number on which the entire fiscal framework rests.

The National Board of Revenue (NBR) would need to increase 50 per cent of its actual tax collections, not its stated target, but what it has actually been collecting, to hit the FY27 revenue goal of Tk 6.04 trillion. In a country where the revenue authority has never met its target, this is the number on which the entire fiscal framework rests.

What Genuinely Changed: The most significant move in the budget is the focus on the heath sector as allocation rises by over 95 per cent to Tk 694.09 billion, 1 per cent of GDP, the highest ever in absolute terms and as a share of national income. Bangladesh has chronically underinvested in health relative to its income and population. A near-doubling of the allocation is directionally right. The test, as always, is execution: the health sector has a poor track record of spending what it is allocated. The real story will be in the utilisation rate six months from now.

Education gets a second record allocation as proposed spending rises 57 per cent to approximately 2 per cent of gross domestic product (GDP), which is also a record.

Two consecutive record allocations to health and education, if actually spent, would mark a genuine structural shift in Bangladesh’s public investment priorities. Whether the Ministry of Education can absorb and deploy a 57 per cent budget increase in a single year is a separate and harder question.

In the energy sector, there is a serious renewable push, with a tariff question unresolved. The budget sets a target of raising renewable energy’s share of total generation to 20 per cent by 2030. To get there, it introduces a zero-duty regime on imports of solar generation equipment and a 5 per cent rebate on consumers’ solar electricity bills. The incentive architecture is coherent: zero import cost on the supply side, a direct price signal on the demand side.

The zero-duty window is sensibly designed — Bangladesh has no domestic solar manufacturing base worth protecting, so tariff barriers on panels have been a pure tax on adoption. What the budget does not address is grid capacity: intermittent solar at scale requires storage and grid management investment that was not announced.

Notably, the BERC tariff decision is still pending. Energy pricing is the single largest constraint on Bangladesh’s industrial competitiveness, and leaving the tariff question unaddressed means the budget’s growth assumptions rest on a foundation that hasn’t been laid.

Subsidies in agriculture are frozen at Tk 170 billion, unchanged from the prior year. In a context of elevated input costs and stagnant farm incomes, this is a meaningful and unannounced policy choice: farmers will not feel relief from this budget. The Tk 79.46 billion development allocation for cold storage, rural infrastructure, and crop insurance pilots holds more promise, but delivery depends on implementation capacity that has historically lagged.

Information Technology (IT), artificial intelligence (AI), and the creative economy get a number of perks in the budget. Tax holidays for software and IT-enabled services are extended to 2030. Tk 5.0 billion crore fund for AI, electronics, and IT entrepreneurship has been confirmed. The creative economy target (0.5 million high-value jobs in content creation, gaming, and animation) is more credible than it might first appear. Bangladesh already has a substantial freelancing base and genuine comparative advantages in a young, digitally literate population. The question is whether training pipelines, intellectual property frameworks, and payment infrastructure will follow the headline number.

The RMG corporate tax structure remains unchanged. The bonded warehouse facility has been extended to non-RMG export sectors. Tk 50 billion SME credit guarantee fund is confirmed operational, and the Export Development Fund has been expanded to $5 billion, the most operationally ready of the budget’s commercial incentives.

The Bottlenecks: The revenue-to-expenditure pipeline. The NBR must increase actual collections by roughly 50 per cent to hit its target. The budget proposes digital filing reforms but does not address the structural obstacles: a narrow tax base, powerful constituencies that resist taxation, and a legal culture that treats tax payment as negotiable. When revenues fall short, expenditure will be cut and history suggests the Annual Development Programme (ADP) will bear the heaviest burden. A 30 per cent larger ADP, in that context, is a promise the implementing ministries will struggle to honour given persistent land acquisition delays, procurement bottlenecks, and capacity constraints.

Banking, credit, and investment. No bank recapitalisation was announced, despite the International Monetary Fund (IMF)’s characterisation of the sector’s vulnerabilities as “systemic.” Non-Performing Loans (NPLs) stand at 30.60 per cent of total advances. Credit growth is below 5 per cent. The budget extends incentives to exporters and MSMEs, but does not address the fundamentals constraining investment — energy reliability, contract enforcement, and regulatory complexity. The 6.5 per cent growth target requires a private investment recovery that the banking sector, in its current state, cannot finance.

Bottom Line: This is a budget of genuine ambition on health and education, with real money behind priorities that have been underfunded for decades. But the ambition rests on a fiscal framework that requires revenue performance without historical precedent, expenditure execution without institutional reform, and private-sector growth without banking-sector repair. The promises will be measured not by the speech, but by the utilisation rates IMED publishes in the months ahead.

The writer is former director general of Bangladesh Institute of Development Studies (BIDS). The piece is excerpted from The Dhaka Brief (www.kasusual.substack.com/p/the-dhaka-brief)

© 2026 - All Rights with The Financial Express