Commendably, Bangladesh bank is now well-aware of the causes of poor recovery of defaulted loans as well as delayed case disposal and trying to mitigate the crisis of non-performing loans (NPLs) in the banking sector. A number of steps have already been taken by the central bank. Focus should be on the nature and effectiveness of each step or directive, and also on what is still ignored as a real remedy for rejuvenating the recovery drive. It has to be made clear-what actually we are pursuing - balance sheet beautifying approach or balance sheet enriching approach or both in a balanced framework? During the regime after July-uprising, we have had an opportunity to initiate reforms in many crucial areas, and as such stringent and unflawed legal measures can be designed to beef up our recovery battle. Are we moving on that track?

BANGLADESH BANK'S DIRECTIVES/STEPS TO REDUCE NPL:

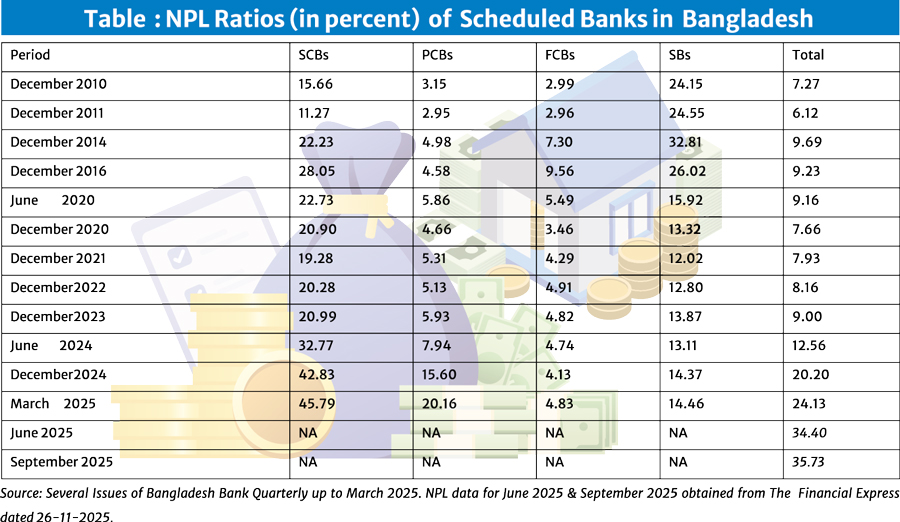

(i) Bangladesh Bank (BB) chalked out a roadmap to bring down overall NPL ratio to below 8 per cent, below 10 per cent (in state-owned banks), and below 5 per cent (in private banks) by June 2026.

(ii) The central bank has directed all commercial banks to implement the regulator's instructions to significantly reduce mounting default loans (the ratio of which reached around 36 per cent in September 2025) by December 2025.

(iii) Reducing write-off period from three years to two years. Rescheduling facilities for aggrieved borrowers.

(iv) Establishment of a separate unit named 'Write-off Loan Recovery Unit' to oversee the recovery process for defaulted loans. The managing director or chief executive of the bank will supervise this unit. Achieving the loan collection targets will be inserted in their performance evaluation.

(v) BB has issued circulars directing banks to enhance the efficiency and capacity of their legal divisions to ensure prompt legal action and expedite loan recovery.

(vi) Strengthening governance to reduce NPL, which is considered a root cause of the issue. Revising policies related to the qualifications and responsibilities of stakeholder directors, as well as formulating policies regarding the appointment, remuneration, and responsibilities of individual directors.

(vii) Special allowances for bank officers involved in recovering non-performing loans.

(viii) Formation of Asset Management Company (AMC) that will facilitate disposal of written-off assets.

ANALYSIS AND EVALUATION OF BB'S STEPS/DIRECTIVES: The Central bank's direct measures to curb NPL ratio can be singled out, and they include shortening writing-off period and loan rescheduling (SL-iii). The step in (i) indicates only targets (i.e. ends, not means or measure) and the directive in (ii) signifies a strong reminder to the banks to comply with regulator's instructions. The other steps or directives (iv to viii) may have indirect impact upon NPL reduction.

Write-off and loan rescheduling would result in a cut in NPL in the form of balance sheet cleaning only, not in terms of real recovery of loans. The regulator is yet to go beyond measures like rescheduling and writing-off. Similar steps led to reduction or slight fluctuations in NPL ratios over the period from 2010 to 2023 ( as perceived in trends of NPL ratios shown in the Table).That those steps only were not sufficient to reduce NPL proportion is evident in the years 2024 and 2025 ( as the Table shows) which register a unbridled growth of NPL ratio, a transition from chronic stage to acute stage.

If considered just quantitatively, NPL ratio may be reduced by adoption of the measures such as (a) increasing recovery rate, (b) loan rescheduling, (c) writing-off, (d) deferring classification time, and (e) increasing volume of new loans. But only satisfactory level of recovery can lead to real progress in NPL management. Unfortunately, that has become a dream now. The regulator has fixed targets of NPL reduction by June .2026 but it seems impossible to achieve the targets with the measures taken so far. The banks instructed to cut NPL by December 2025 is more likely to extend new loans to facilitate target realisation. If new loans are sanctioned and disbursed carefully, that tendency may produce some good to NPL management. Much stronger monitoring is crucial.

WHAT IS TO BE DONE: We are actually heading towards great distress of the banking sector as a whole. It is, no doubt, easy to find faults, but very difficult to suggest solution options. Top priority on resorting to stringent legal measures has no alternative at the present situation. We must work for developing a radical reform framework, particularly making the recovery laws free of all possible loopholes on which borrowers may capitalise to bypass the obligation of repaying bank dues fully or partially. Appropriate laws and regulations are a necessary condition. But strict enforcement, government's uncompromising stance, united efforts of the regulator and the banks can ensure success in recovery drive.

It is to be mentioned from my own working experience and some bank professionals 'views that the bank authorities or the branch managers face challenging situations while placing the collateral in auction process. First, the concerned borrowers complain saying that auction price is too low and that price affects their interest. Then, many of them go to file cases in the court against the bank. Second, some situations arise when no person or institution participates in the auction.

Third, without auction sale of collaterals and loan adjustment with sale-proceeds, lawsuits cannot generally be filed in any Artha Rin Adalat. Besides, branch managers going for tough recovery drive often face several threats. So strict legislation and enforcement thereof are an urgent necessity.

Apart from legal measures, maintaining integrity, due diligence and high sense of responsibility is a prerequisite for successful credit management. Improvement of bank officials' efficiency in loan processing, sanctioning, disbursement, security valuation, documentation, renewal, enhancement, rescheduling and recovery at the individual bank level as well as performance monitoring and control are all crucially important. How far the valuation of collaterals by enlisted valuation companies is unbiased and reliable is also an important issue to be addressed seriously.

Our legal battle for loan recovery is at bay mainly due to loopholes, deficiencies, and leniencies in law. Bangladesh Bank data show that as of June 2025, 222,341 cases involving Tk 407,435 crore were pending across the courts (The Daily Star, December 07, 2025).The government should make a draft outline of necessary amendments to the existing Act as soon as possible. As the national elections are scheduled in February, the new political government would govern the country. The draft would then be left to the new government for discussion, approval, and legislation by parliament.

ESSENTIAL CONSIDERATIONS FOR DRAFT AMENDMENTS: Amendments to Artha Rin Adalat Ain, 2003 are very essential. Effective consultation with every bank is necessary. A bank's views and suggestions must come mostly from field and mid-level officials/branch managers (handling credit management, recovery of loans, cases) and legal advisors. An outline (not exhaustive) of considerations is inserted here.

1.The length of step by step procedures required for every stage from filing of cases to disposal and enforcement thereof should be maximally shortened to quicken the legal solution.

2. There should be a provision for an agreement between the bank and the borrower to the effect that the borrower shall not have any right to sue against the bank raising any question regarding the value of collateral set in auction process.

3. Withdrawal of the maximum limit than the loan dues more than three times the principal loan amount cannot be realised from a borrower or borrowers.

4. Adequate number of courts, judges and logistic support must be ensured for quick disposal.

5. Close cooperation of police department in management and disposal of cases by courts. Every police station must have an enforcement cell especially designed for banks' loan cases and also for ensuring security of banking personnel dealing with cases.

6. Scopes for stay orders must be curbed significantly.

In fine, it may be reiterated that the concerned recovery laws and regulations ought to be revised, amended, and strengthened sufficiently to ensure quick and fruitful recovery of all loan dues. Internal credit governance system also needs to be streamlined. The government and the regulator should attach top priority to public interest, rather than the interest of the few influential.

Haradhan Sarker, PhD, is ex-Financial Analyst, Sonali Bank & retired Professor of Management. sarkerh1958@gmail.com

© 2026 - All Rights with The Financial Express