Source: AI-generated picture from Google

Source: AI-generated picture from Google Fintech is revolutionising technology everyday not only in Bangladesh, but also around the world. The embracing of technology drives the financial sector to rethink about the service framework with time and cost efficacy. Banking services are currently going through a paradigm shift from traditional structures to digital transformation. Inclusion of technology in every sphere of service propositions derived from deposit account opening to lending along with bank assurance brings up a new style of advanced banking. Bangladesh is now in a position to be a smart witness to it. The economy demands to be cashless as well as services are assumed to be rendered through technological adoption in all spares of banking, where technological revolution like scoring based digital lending, embedded finance, blended finance, derivatives and digital trade are taking places. Furthermore, the thrive seeks a new model, where Open Banking, a new system to utilise the customer data from third party secured Application Programming Interfaces (APIs) to render financial services in the market. The nation's banking industry has been droning a lot about open banking in recent days. Through strong cooperation between banks, fintechs, and regulators, open banking is on the way to be introduced in Bangladesh very soon. The central bank plans to issue open banking guidelines very soon.So, it is time to understand what open banking actually is, where is its origin, which countries are the pioneers and which countries are practising what type of open banking model etc.

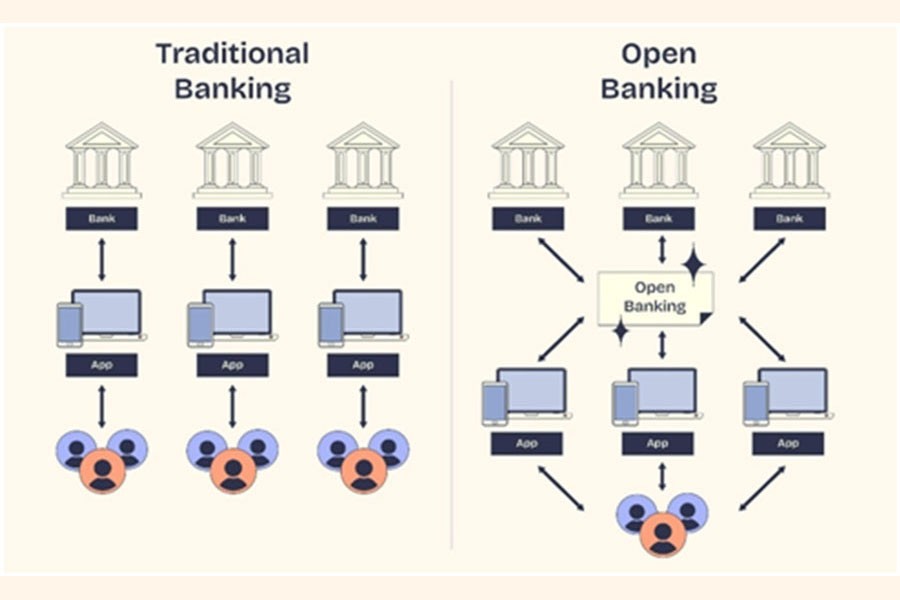

An innovative method of payment and servicemanagement avoiding additional expenses is Open Banking. Open banking as a customer-centric banking, allows a single window across different financial institutes for banking and advisory services within the shortest possible of time.It broadens the area of safely access to any banking information. It aids in comprehending the creditworthiness of customers, their spending patterns and preferences. With this information, businesses may provide goods and services that better meet the needs of their clients. Since the mobile penetration ratio in Bangladesh is high, it is possible to initiate open banking as a system for greater and quicker financial inclusion in the coming days.

An innovative method of payment and servicemanagement avoiding additional expenses is Open Banking. Open banking as a customer-centric banking, allows a single window across different financial institutes for banking and advisory services within the shortest possible of time.It broadens the area of safely access to any banking information. It aids in comprehending the creditworthiness of customers, their spending patterns and preferences. With this information, businesses may provide goods and services that better meet the needs of their clients. Since the mobile penetration ratio in Bangladesh is high, it is possible to initiate open banking as a system for greater and quicker financial inclusion in the coming days.

The working area of open banking integratesseveral activities like personal finance & budgeting (renowned apps in the world are Revolut, Moneyhub, Emma, Rocket Money, Quicken Simplifi etc.), payment & transfer (renowned apps in the world are Yolt, Stripe, Trustly etc.), data integration and connectivity (platforms includes Plaid, Salt Edge, Yapily etc.), credit scoring and lending (renowned platforms are Finicity, nCino etc.), wealth management and investing (renowned platforms are US based namely Empower,Acorns etc.)

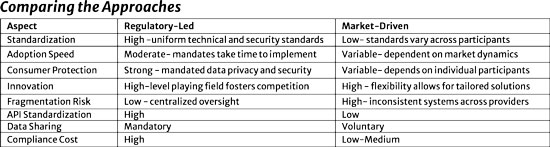

The evolution and progress of Open Banking worldwide emerged when the EU regulations established under the first PSD, which was implemented in 2007, are updated and improved by the revised Payment Services Directive (PSD2). Open banking is getting momentum in many countries around the world. However, countries that are considering to move into open banking system, the question remains whether they should use an already established approach in any country or replicate the European approach! To consider this issue, the country's financial sector infrastructure, the country's market and policy objectives for open banking should be given priority.However, there are currently two types of approaches in open banking: Market-Driven Approach and Regulatory-Driven Approach. In addition, Hybrid or Collaborative Models/Approaches are followed in some countries.

MARKET-DRIVEN APPROACH: Market-driven open banking having no single mandate, is a model of financial innovation where banks voluntarily create APIs (Application Programming Interfaces) to share customer data with authorised third parties forming bilateral agreements, driven by competition and market demand rather than strict government rules, allowing for flexible innovation in services like personal finance apps, but potentially leading to less standardisation than regulatory-led systems like the EU's PSD2. Countries like the US, Japan, India, and Singapore often favour this approach, focusing on flexible, negotiated data access, while regulatory-driven models mandate standardised access.

REGULATORY-DRIVEN APPROACH: Regulatory-driven open banking mandates secure customer data sharing via standardised APIs (Application Programming Interfaces) through government rules, fostering innovation, competition, and consumer protection by creating a level common field for banks and fintechs, exemplified by the EU's PSD2 and the UK's initiative, ensuring unified standards and trust, unlike market-driven models that evolve organically.

HYBRID OR COLLABORATIVE APPROACH: This model of Open Banking is known as the "Middle Ground" approach combining both the above structures, where the government set "rules of the road" and banks & fintechs work together for value added services. This model is followed in Australia, Mexico, Hong Kong.

THE EFFECTIVE APPROACH FOR BANGLADESH: In Bangladesh, Open Banking is in early stage of development. Since there is no concrete data analytics about the population, their credit accessibility, and other personal informamation, the market-driven approach will be a bit challenging to implement as the fintechs are not highly regulated in the financial market and credit bureau is still under process of licensing. The Asian countries following market-driven approaches are Singapore, India. Furthermore, every country needs a regulatory framework to operate the Open Banking platform, so does Bangladesh. Our country can follow the models of Singapore, India etc., as global examples in formulating an open banking framework. For Bangladesh, the effective approach may be the hybrid or collaborative approach, where Bangladesh Bank as a regulator may set the Unified API standards and phased implementation criteria as "rules of the road" and to encourage the bank and fintechs to leveragecommon infrastructure. In addition to this, Bangladesh Bank should open competitive playing fields for fintechs and encourage all the financial institutions to make incentive-based collaboration such as revenue sharing, cost minimisation, data privacy and consent management etc. It will ensure the technological agility for the upcoming financial and banking sectors in Bangladesh.

CHALLENGES AHEAD: A major challenge of open banking is data security and privacy management. The biggest asset of this techno driven world is data, integration of which into every financial platform is challenging. This integration along with digital literacy can strengthen the banking system in large scale.

Therefore, in all respects,Open Banking is a key enabler of a cashless Bangladesh because it promotes digital payments, improves financial inclusion, enhances customer convenience, fosters innovation, reduces costs, and strengthens the country's digital economy. By creating a connected and customer-centric financial ecosystem, open banking can accelerate Bangladesh's transition from a cash-based society to a modern digital economy.

A.S.M. Ahsan Habib is a banker and Certified Digital Finance Practitioner (CDFP). Sanjoy Pal is a Researcher, banker and Visiting Faculty of an institute affiliated with National University, Bangladesh. sanjoy25@gmail.com

© 2026 - All Rights with The Financial Express