In democratic governance, the question of how public resources are mobilised and spent is particularly important to the relationship between citizens and state. The government is always expected to respond to this question by ensuring greater transparency in its fiscal administration and management. However, the state of transparency in government finances differs remarkably across the world as some countries exercise greater state-citizen engagement in public financial management while others do not. Given the importance of public participation in the government's budget decision making, the International Budget Partnership's (IBP) Open Budget Initiative has been striving to promote transparency and oversight of government spending. As a part of the Initiative, the IBP has been conducting the Open Budget Survey (OBS) since 2006 with a view to conducting a comparative and independent assessment of fiscal transparency, oversight, and participation at the national level. In performing the assessment, the OBS mainly focuses on such practices as public access to information, good public financial management by executives, and adequate oversight practices by legislature and auditors, which presumably consolidate representative democracy in a country.

Being the world's only independent and comparative assessment of the three major pillars of public budget accountability system - transparency, public participation, and oversight, the OBS takes place once every two years. The latest round of this biennial exercise - the 2019 survey - assessed 117 countries across six continents, adding 15 new countries to the assessment since the 2015 survey. In terms of the assessment of budget transparency, the OBS considers the timeliness and volume of budget information made publicly available and ranks each country on the Open Budget Index (OBI) with a score between 0 and 100. The higher the score is, the greater budget transparency the country exercises. Budget transparency of a government is reflected through the publication of the following eight budget documents in a timely and comprehensive manner: (i) pre-budget statement, (ii) executive's budget proposal, (iii) enacted budget, (iv) citizens budget, (v) in-year reports, (vi) mid-year review, (vii) year-end report, and (viii) audit report. OBI categorises countries into five major heads in terms of the availability of information - 'extensive' with score between 81 and 100, 'substantial' with score between 61 and 80, 'limited' with score between 41 and 60, 'minimal' with score between 21 and 40, and 'scant' with score 0 and 20. The measure of public participation takes account of the opportunities provided by the government for the public and civil society to engage in decision making on how public resources are generated and used. Finally, oversight, as another component of budget accountability system, is assessed based on the role and effectiveness of formal oversight institutions, such as legislatures, national audit offices, and independent fiscal institutions.

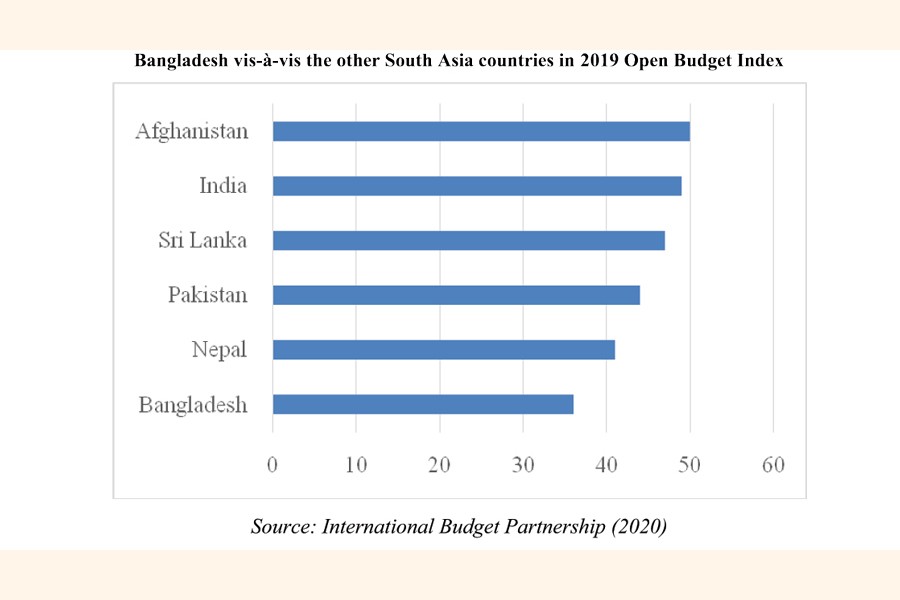

Bangladesh lags behind many of its South Asian counterparts in terms of the three above-mentioned pillars of budget accountability system. Moreover, Bangladesh's score on OBI has substantially declined over the past few years. In 2015, Bangladesh's score on OBI was 56, which declined to 41 in 2017 and 36 in 2019. According to the 2019 OBI, the country ranks below all the OBS-participating South Asian countries such as Afghanistan (50), India (49), Nepal (41), Pakistan (44) and Sri Lanka (47). Bangladesh's score on 2019 OBI is even lower than the global average of 42. It can, however, be noted here that one of the reasons for such a decline in Bangladesh's score may be the change in the definition of "publicly available" in OBS 2017, which only considers those documents as publicly available that are published online on an official government website. Since publication of government information online is now considered as a basic standard for public availability of the budget documents, Bangladesh can no longer receive score for the publication of mid-year review, which is only available in published form. In addition, inconsistency has been observed in the country's performance in making the budget documents publicly available in a given year. For instance, in 2019, Bangladesh delayed the publication of in-year reports online (not published within three months) and failed to produce the year-end report within one year as well as the audit report within eighteen months, thereby receiving a lower OBI score.

In terms of the public participation in budget decision-making, Bangladesh's score of 13, which is slightly lower than the global average score of 14, indicates that the country provides very few opportunities for meaningful civic engagement in the budget process. Regional comparison suggests that Bangladesh lags behind Nepal (22), Sri Lanka (17) and Afghanistan (15), and surpasses India (11) and Pakistan (4) in enabling the citizens to participate in the process of public financial management. For improved public participation, initiatives such as participatory budgeting and social audits can be adopted to facilitate exchange of views between the citizens and the government. In addition, preparing audit report on a regular basis in a timely manner and holding legislative hearings on that involving the public or civil society organisations can further promote public participation in the budget process.

Given the limited oversight provided by the legislature and the supreme audit institution during the budget cycle, Bangladesh experiences inefficient implementation of its overall budget plan. The country's score of 39 for budget oversight falls below that of India (59), Sri Lanka (50), Nepal (48), and Pakistan (45), although it is higher than that of Afghanistan (31). It is important to note that, as suggested by the OBS 2019, countries with lower level of budget transparency usually undergo lax budget oversight despite the availability of the basic conditions for supreme audit institutions to perform their oversight functions. The major problems associated with budget oversight in Bangladesh, which should be addressed sooner rather than later, are (i) not providing the Executive's budget proposal to legislators in advance, (ii) legislative committee's failure to examine or publish reports on in-year budget implementation online, and (iii) little or no consultation with the legislature while the budget is implemented.

Dr. M. Abu Eusuf is the Professor, Department of Development Studies & Director, Centre on Budget and Policy, University of Dhaka;

Executive Director, Research and Policy Integration for Development (RAPID). eusuf101@gmail.com

© 2026 - All Rights with The Financial Express