Despite known and evolving challenges, Bangladesh economy has demonstrated good consolidation in 2025. Market liquidity especially foreign currency liquidity improved much with significant rise in wage earners' remittances, moderate rise in exports and foreign aid disbursement. Inflation continued to remain high with regular pinch on personal spendings. Bangladesh Bank couldn't do much with high interest rate as the government heavily relied on borrowing from banking sector at high rates as well as bad debt bonanza continued with much pressure on banking sectors' ability to generate fresh lending to the needy streams. High interest rate also constrained good entrepreneurs to go for further investment. Large banks found a 'safe heaven' in investing in high-yield govt. treasury bonds rather than extending fresh loans to business houses. Unrest and witch hunting in the industrial sector also dented stability in country's production belts. The interim government as a whole wanted to maintain status quo with regard to overall public financial management. Therefore no 'new model' was initiated for better management of budgetary resources, social safety net allocations or overall fiscal issues. Long pending revenue reform was pushed forward by IMF but the overall restructuring fell into cracks due to legacy problems within the civil bureaucracy and lack of fair visibility about the destination. There seemed to few directional steps taken by the central bank, however we have to wait for few years for real results to come in from moves to 1) identify how big is the hole created by bad loans and capital flights in the large banks' balance sheets, 2) bring back the siphoned-off money, 3) recapitalization of the large banks and 4) merge Islamic banks at the cost of the national exchequer.

Hence, we should keep our fingers crossed about 2026. However, all including the development partners and investment community seemed to have pinned high hopes on national election scheduled for February. They expect a notable boost in confidence among entrepreneurs and investors, both local and foreign. Many hope this political clarity will pave the way for higher job creation and stronger GDP growth.

Inflation, very loud through much of 2025, is also expected to ease. Analysts justify this with softer global food and energy prices along with stabilization in the domestic economy. Yet a full economic turnaround may take time, as any new government will need several months to implement policies effectively. Much also depends on how the new government decide on the next course of action and who calls the shot. To the irony, despite new government in the chairs, much change may not be seen as long as the 'Bank' and the 'Fund' or as such only development partners continue to decide our course of economic management.

We do see some relief coming from improvement in the balance of payments and foreign exchange reserves. We have seen over the past year, the interim government trying to narrow the gaps in the macroeconomy and halt the erosion of foreign reserves.

The financial sector also endured a difficult 2025, grappling with mounting non-performing loans. The merger of five struggling banks though not visible yet, is expected to provide a stronger foundation for lending and financial stability in 2026.

The primary hope for the year is the democratic transition in February. A new government must channel this political mandate into higher economic growth that is inclusive, equitable, and just.

Ongoing reforms though still very feeble, combined with the stability offered by a five-year policy horizon, would give businesses the confidence to invest. Higher investment potential after an inclusive and fair election should boost employment, purchasing power, and overall growth.

Considering the role of development partners in Bangladesh's economic journey, the new government should get more engaged with global investors, trade partners, and development agencies. For this we need political stability and peace in the production belts.

Hence a congenial law and order situation is non-negotiable. No doubt, lower energy and food prices, along with stronger global supply chains, could further support growth, provided no major disruptions occur.

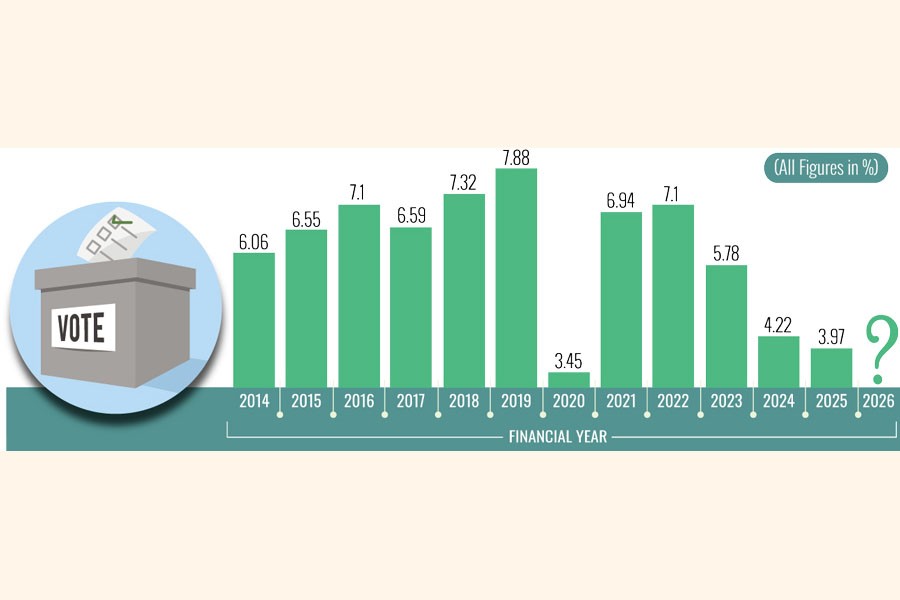

Several challenges from 2025 are also likely to continue into the new year. Investment remains sluggish, and creating decent jobs for youths is an urgent task. As mentioned, in an emerging economy like ours, inflation requires careful management through market oversight and supply-side measures. Rising debt repayments demand stronger domestic revenue mobilization, which can be achieved through the digitization of the tax system, strong stance against corruption, reducing VAT leakages, and expanding income tax collection. Keeping a constant eye on the exchange rate should also be considered.

In order to ensure distributive justice by the new government, income and asset inequalities also be addressed. As we also know, export growth has slowed in recent months, highlighting the need to reduce the cost of doing business, improve turnaround times, and better management of industrial parks.

While we talk of improving the export basket and pie, product and market diversification has long been discussed, but progress remains limited. As Bangladesh prepares to graduate from LDC club this year, these measures will warrant greater urgency.

In brief, we recommend following priorities for 2026.

-Addressing ongoing macroeconomic challenges like improving overall fiscal management and optimizing the expenditures.

-Stimulating growth streams that have slowed, including investment, exports, small businesses, and domestic demand.

-Restoring economic governance across the financial sector, including banks, insurance, non-banks, and the capital market ecosystem.

-Rolling out a structured economic reform framework in the near term to set the runway right. Despite some improvement, inflation is still high, private investment lags at around 22 percent of GDP, and export and product diversification are weak. Small businesses have received limited targeted support over the last 15 months.

We now want a good election to happen. A stable democratic government allows people to engage in dialogue and work towards setting a long-term policy, which in turn boosts business confidence. Once a democratic government is in place, the law-and-order situation is also expected to improve. In fact, it is supposed to an 'one way traffic' for the new government.

Mamun Rashid is an economic analyst and chairman at Financial Excellence Ltd.

© 2026 - All Rights with The Financial Express