Bangladesh has taken an important step toward strengthening its international financial architecture by introducing the Offshore Banking Act, 2024. The objective of this legislation is to facilitate cross-border financial transactions, support foreign investment, and create a globally competitive financial environment for enterprises operating in specialised economic zones such as Hi-Tech Parks.

However, despite the policy intent, some operational opacities remain. One issue is the interaction between Domestic Banking Units (DBUs) and Offshore Banking Units (OBUs), especially when companies in specialised zones generate revenues in local currency but must conduct foreign currency transactions.

Hi-Tech Park–based industrialisation and efforts to attract foreign investment in Bangladesh are not new. However, integrating OBU-centric commercial structures has added a new dimension. Multinational companies in the smartphone and electronics sector—such as OPPO, VIVO, OnePlus, and Realme—which are fully foreign-owned, now face a practical operational challenge.

The core issue is simple but significant. These companies import goods in foreign currency, while much of their sales revenue is in Bangladeshi Taka (BDT). As a result, they must settle import liabilities (LC payments) in foreign currency, while their income is mostly in local currency, creating a clear currency mismatch.

The core issue is simple but significant. These companies import goods in foreign currency, while much of their sales revenue is in Bangladeshi Taka (BDT). As a result, they must settle import liabilities (LC payments) in foreign currency, while their income is mostly in local currency, creating a clear currency mismatch.

Many of these companies use OBUs to open import LCs because they suit international trade and foreign currency transactions. However, once an LC is opened, its settlement requires foreign currency, which is not always available in the OBU since sales proceeds are deposited in DBUs in BDT. Companies also prefer OBUs due to their simplified operational procedures worldwide.

So, how can an effective operational linkage be established between these two platforms?

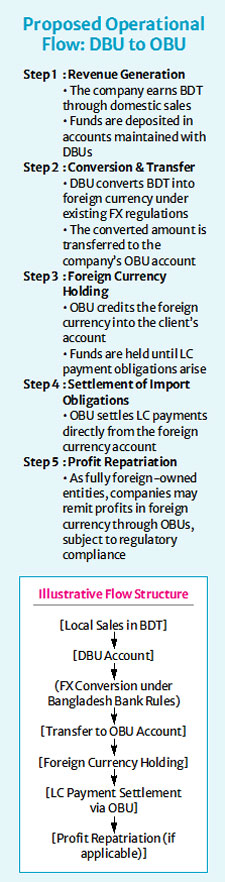

A practical and efficient model may be structured as follows. First, the company’s local sales proceeds are deposited in the DBU in BDT. Then, under foreign exchange regulations, the DBU converts these funds into foreign currency. The foreign currency is then transferred to the OBU, where it is credited to the company’s foreign currency (FC) account and held until LC settlement is due.

To ensure the effectiveness of OBU-based commercial activities, a well-defined funding mechanism between DBU and OBU is essential. Without such a mechanism, even if LCs are opened, timely settlement may become difficult, potentially disrupting supply chains and undermining business confidence.

Moreover, since these companies are fully foreign-owned, repatriation of profits in foreign currency is also critical. In this regard, the OBU can serve as an effective platform—provided that the conversion and transfer of funds from DBU to OBU are clearly defined and permitted within the regulatory framework.

While existing Bangladesh Bank guidelines have laid the foundation for OBU operations, operational gaps remain in DBU–OBU coordination. Clearer guidance is needed on BDT-to-foreign currency conversion, inter-unit fund transfers, and LC settlement mechanisms.

International experience suggests that building a successful Offshore Financial Centre (OFC) requires more than policy liberalisation—it demands operational integration. Financial hubs such as Singapore, Dubai, and India’s GIFT City have well-defined frameworks for coordinated fund movement between onshore and offshore units, ensuring a seamless financial environment for investors.

Bangladesh needs to adopt a similar approach. If Hi-Tech Parks and Special Economic Zones are to emerge as genuine global investment hubs, DBU–OBU coordination must be policy-clear, technologically efficient, and supported by robust risk management.

The Hi-Tech Park ecosystem in Bangladesh is expanding rapidly under the leadership of the Bangladesh Hi-Tech Park Authority. According to official data, more than 175 companies have been allocated space across various hi-tech parks, while over 148 startups are operating in incubation facilities. These parks have already created more than 22,000 direct jobs and contributed to the development of a growing pool of skilled ICT professionals.

Investment momentum is also encouraging. The Hi-Tech City, kaliakoir alone has attracted over $800 million in investments from around 50 local and foreign firms, with dozens of companies already in operation. Once fully operational, employment in the park is expected to reach approximately 50,000, highlighting the sector’s strong economic potential.

Government projections further indicate that cumulative investment in hi-tech parks could exceed Tk 24 billion by 2026, underscoring the sector’s growing importance in Bangladesh’s industrial transformation.

Many of these enterprises are fully foreign-owned and eligible to maintain accounts with OBUs. However, a significant portion of their revenue comes from domestic sales, so earnings are largely in BDT.

At the same time, these firms regularly import machinery, technology equipment, software solutions, and raw materials from foreign suppliers. To facilitate these transactions efficiently, companies often prefer to open LCs through OBUs.

From a financial perspective, the transaction structure is straightforward. A company receives sales proceeds in BDT through a DBU, purchases foreign currency with those funds, and transfers the converted amount to its OBU account. The OBU then uses these funds to open LCs and settle payments with overseas suppliers.

This is fundamentally a legitimate foreign exchange transaction. The purchase of foreign currency from authorised dealer banks for genuine import payments is already permitted under Bangladesh’s foreign exchange regulations. Additionally, these companies qualify as offshore clients due to their presence in specialised economic zones.

However, many commercial banks hesitate to process such transactions through OBUs due to the lack of explicit operational guidance from the central bank. This uncertainty discourages banks from facilitating legitimate transactions, even when the underlying business activities are fully compliant.

The hesitation stems more from compliance concerns than from legal restrictions. Bankers often prefer to avoid potential regulatory interpretation risks during inspection or audit by the Bangladesh Bank.

This situation highlights the need for clear policy direction. A simple circular or operational clarification from Bangladesh Bank could confirm that foreign currency purchased by DBUs against legitimate local currency earnings may be transferred to OBU accounts to settle permissible external transactions, including LC payments.

Such clarification would not introduce new financial risks. Rather, it would enhance transparency, improve operational efficiency, and ensure better regulatory compliance.

More importantly, improved clarity would significantly strengthen Bangladesh’s attractiveness to foreign investors. Hi-Tech Parks are intended to serve as innovation-driven industrial clusters that combine technology manufacturing, research, and digital services. Efficient, predictable banking operations in these zones would make Bangladesh a more competitive destination for technology-based investments.

As Bangladesh moves toward a knowledge-based economy and prepares for its post-LDC transition, strengthening the financial ecosystem supporting high-tech industries is essential. Clear policy support for practical offshore banking operations can play a pivotal role in accelerating foreign direct investment and expanding the country’s technology sector.

Bangladesh has already laid the foundation for a modern offshore banking regime. With targeted regulatory clarifications and operational alignment between DBUs and OBUs, the system can become significantly more effective in supporting high-tech industries.

A coordinated and practical approach will ensure that OBUs evolve not merely as parallel banking structures, but as integral components of a dynamic, investor-friendly financial ecosystem—positioning Bangladesh as an emerging hub for technology-driven investment in South Asia.

Md. Saidul Islam CDCS, Vice President & Head of OBU Business, One Bank PLC. Email: sayedcdcs@gmail.com

© 2026 - All Rights with The Financial Express