![]() Like Bangladesh, Vietnam is an old country and a new nation. Like Bangladesh, it has a checkered history of political subjugation. Bangladesh was politically liberated in 1971 while Vietnam was liberated in 1975, marking the end of the almost two-decade long Vietnam war. This paved the way for reunification of North with South Vietnam, and the establishment of the Socialist Republic of Vietnam.

Like Bangladesh, Vietnam is an old country and a new nation. Like Bangladesh, it has a checkered history of political subjugation. Bangladesh was politically liberated in 1971 while Vietnam was liberated in 1975, marking the end of the almost two-decade long Vietnam war. This paved the way for reunification of North with South Vietnam, and the establishment of the Socialist Republic of Vietnam.

In the 1970s, when the two countries started their economic journeys, they were both extremely poor and at the bottom of the economic pile of nations. Populous and highly disaster-prone, Vietnam and Bangladesh are ranked among the top countries likely to be most affected by climate change.

Reform in Vietnam: Bangladesh initiated market-oriented reforms, along with privatisation of its nationalised industries in the late 1970s while Vietnam began its economic reform programme, known as Doi Moi -- meaning renovation -- to transform the centrally planned economy to a regulated market economy in 1986. Besides the extreme poverty and the highly agrarian nature of the country, the other factors that contributed to the urgency of this reform were the spectre of poor economic growth, famine, large budget deficits, hyperinflation, a trade embargo from the United States, and drastic cuts in Soviet aid.

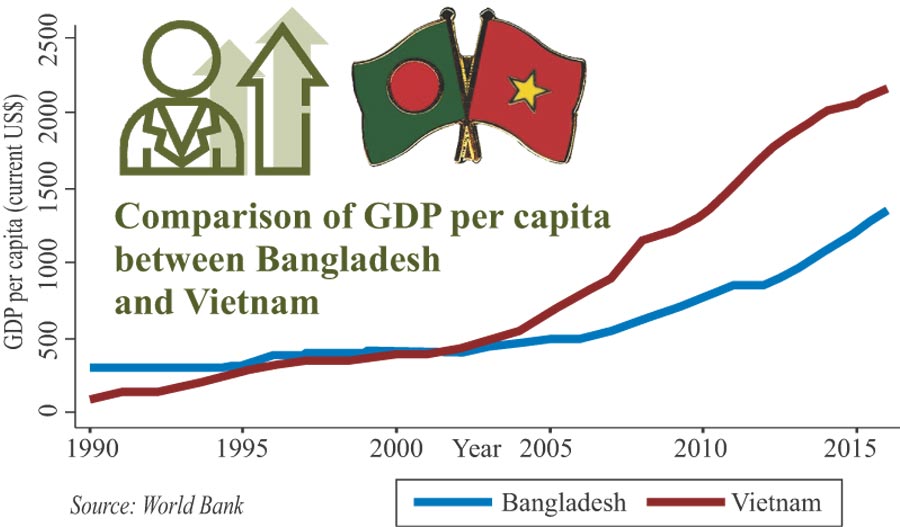

Figure 1. GDP of Bangladesh and Vietnam(1990-2015)

The reform programme was comprehensive, cutting across all sectors of the economy. Prior to reform, agriculture in Vietnam was organised through collectives, which were particularly inefficient. The reform replaced collectives with household farms, where households received long-term leases with the right to exchange, transfer, lease , inherit and mortgage lease rights. During the 1990s, there was further reform to relax restrictions on internal and external trade of agriculture goods -- in particular, rice -- and inputs such as fertilizer. The government also increased the quota on rice exports and removed restrictions on internal trade. Following the successful implementation of these reforms, there was a dramatic conversion of the Vietnam economy: it was transformed from being a subsistence economy -- perennially dependent on import of rice -- to a top exporter of rice.

Prior to Doi Moi, state-owned-enterprises were the dominant means of production outside agriculture. As in agriculture, the Doi Moi reforms introduced a decentralised decision making and gave enterprises autonomy over production, pricing, and trading. The government also implemented policies to introduce further competition by allowing the easy entry of private enterprises, including foreign-owned firms. Its foreign investment law of 1987 opened all sectors of the economy except defence to foreign investors; it allowed 100 per cent foreign ownership of firms, and offered foreign investors generous tax concessions and duty exemptions. Foreign investment was further encouraged by creating export-processing zones and industrial parks. These zones often offered firms reduced tax rates and exemptions from import and export duties. In addition, a number of other reforms were introduced to level the playing field among various types of enterprises -- such as state-owned enterprises (SoEs), foreign enterprises, and private enterprises. These reforms included uniform rules of taxation, the freedom for enterprises to form their own trading relationships, and exposure to foreign competition.

Another important reform for the private sector has been the 2000 Enterprise Law, which made it easier for private enterprises to register and operate across most industries. This law, which reduced the time required to register an enterprise, led to the registration of thousands of new enterprises, following the enactment of the law. Most of the newly-registered enterprises were privately-owned firms. The new firms started operations in the enterprise sector, opposed to in the household business sector, thereby helping formalisation of the economy which was beneficial to both firms and workers.

The rapid changes that took place in manufacturing in the form of restructuring of SoEs, expansion of private enterprises, inflows of new investment and technology, and improved incentive structures for production decisions have all contributed to higher labour productivity in manufacturing.

Along with domestic reforms in agriculture and manufacturing, Vietnam undertook a programme of extensive reform to open up the economy in 1989. Prior to those reforms, foreign trade in Vietnam was subject to central decisions and was carried out by a small number of state trading monopolies. Exports were discouraged through the overvaluation of the exchange rate and the use of export duties; imports had to proceed through an extensive system of quotas and licences; and exports had to fulfill partner obligations within the Council for Mutual Economic Assistance before they could be sold to the convertible currency area . If those obstacles were not enough, Vietnam also faced a trade embargo with the United States that was lifted only in 1994.

The trade reform programme of 1989 had to address a broad swathe of issues including: unifying and devaluing the exchange rate, relaxing import and export quotas, eliminating all budget subsidies for exports, simplifying licensing procedures for import and export shipments, and delisting items from export duties and reducing the rates for remaining products. In 1991, Vietnam allowed private enterprises to engage directly in international trade, and in 1995, removed all import-permit requirements for most remaining items.

These domestic reforms were quickly followed by international trade agreements and partnerships. In 1992, Vietnam signed a preferential trade agreement with the European Economic Community. In 1995, Vietnam became a member of the Association of Southeast Asian Nations (ASEAN) and its associated ASEAN Free Trade Area, which compelled Vietnam to reduce tariffs on imports from ASEAN members to 5.0 per cent or less by 2006 for the vast majority of goods. In December 2001, the U.S.-Vietnam Bilateral Trade Agreement came into effect, leading to a huge increase in Vietnamese exports to the United States, predominantly in light manufacturing products. In 1995, Vietnam also initiated the application process to join the World Trade Organisation (WTO) and won its membership in 2007. In addition to the above, Vietnam had signed free-trade agreements with a number of countries or a group of countries, including Japan (2009), Chile (2011), Korea (2015), European Union (2018) as well as Comprehensive and Progressive Agreement for Trans-Pacific Partnership (2018). As part of ASEAN, it had been a signatory to a number of free-trade agreements with such countries as India, Australia, New Zealand, Korea, Japan and China.

The policy of outward-orientation of Vietnam played an important role in changing the structure of trade as well as in changing allocation of workers from agriculture to manufacturing, as agricultural exports became relatively less important over time. During 1997 to 2010, manufacturing employment grew at an average annual rate of 7.5 per cent. Additionally, the liberalisation of foreign investment and SOE reforms interacted in important ways with trade reforms and affected the composition of ownership of firms involved in international trade. By 2010, foreign-invested firms were responsible for more than 50 per cent of all exports, compared with only about 25 per cent of exports in 1995, while imports by foreign firms rose from 18 to 44 per cent of total imports during the same period. Thus, Vietnam's trade reforms directly and in important ways impacted the structure of the workforce across firms of different ownership type.

The great divergence: The programme in Vietnam, Doi Moi, encompassing privatisation, liberalisation and international openness, had a dramatic impact on the growth and dynamism of the country. Between 1990-2000, the country grew at 7.9 per cent annually, compared to 4.7 in Bangladesh. In the subsequent years, between 2000-2017, Vietnam grew at 6.3 per cent compared to 6.0 per cent in Bangladesh. These differentials in the pace of growth translated into significant differences in per capita incomes, although Bangladesh started with an advantage in 1990. In 1990, Vietnam had about one-third of the per capita income, in terms of current US dollars, of Bangladesh, but by 2017 Vietnam's income exceeds that of Bangladesh by more than 50 per cent (see Figure 1). A similar disparity exists if viewed in terms of purchasing-power-parity dollars.

The accomplishment of Vietnam in terms of poverty reduction was equally spectacular. The incidence of poverty, measured with reference to the international poverty line at $1.90 a day ( 2011 PPP dollars), was 2.6 per cent in 2014 while the corresponding rate of poverty for Bangladesh was 14.8 per cent in 2016.

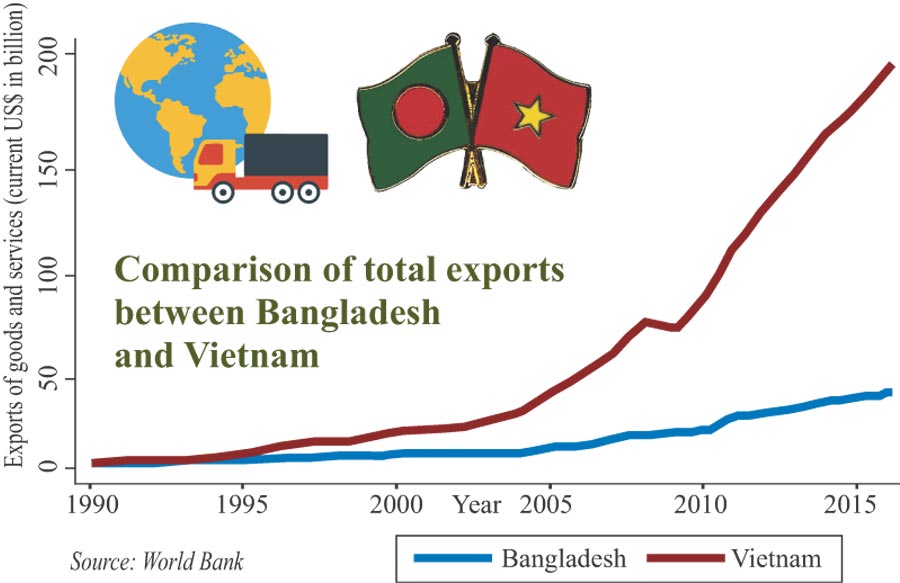

An important objective of the reform programme was to open the economy to international trade and investment. From this objective, the programme was a resounding success. The drastic reduction of tariffs as well as abolition of quotas and licences in conjunction with a plethora of free-trade agreements catapulted the economy into an export power-house. In 1990, both Bangladesh and Vietnam had meagre export earnings that hovered around $2.0 billion. Although Bangladesh exhibited robust export growth over time, its performance fell far short of that of Vietnam. In 2017, Bangladesh's export earnings reached around $38 billion whereas those of Vietnam crossed $227 billion (about six times that of Bangladesh) (see Figure 2).

Figure 2: Export Earnings of Bangladesh and Vietnam ( 1990-2016)

The growing importance of trade in the economy can also be seen from the trade-GDP (gross domestic product) ratios of the two economies. In 2017, it was 200 for Vietnam while it was around 35 for Bangladesh.

An important dimension of trade relates to the composition of exports -- the concentration of the export basket is in terms of products. In the case of Bangladesh, the export-basket has been dominated by readymade garment (RMG). On the other hand, Vietnam has over time remarkably diversified its economy in terms of both the range of goods produced as well as export partners. Vietnam now exports to a wider range of markets than ever before, and has rapidly expanded exports in the manufacturing and electronics sectors, countering its once-heavy reliance on exporting agricultural products. Table 1 provides estimates of the concentration ratio of exports of the two countries. The concentration index, also named Herfindahl-Hirschman Index, is a measure of the degree of export concentration. An index value closer to 1 indicates a country's exports are highly concentrated on a few products. On the other hand, values closer to 0 indicates that exports are highly diversified across many products.

Using the 1992 revision of the HS (Harmonised System) classification, the diversity of Vietnam exports is also evident from the fact that the top exports of Vietnam in 2017 were broadcasting equipment ($34.1 billion); integrated circuits ($14.9 billion); telephones ($9.9 billion); textile footwear ($7.94 billion) and computers ($6.36 billion). The corresponding list for Bangladesh includes non-knit men's Suits ($5.98 billion); knit T-shirts ($5.5 billion); knit sweaters ($4.47 billion); non-knit women's suits ($4.06 billion); and non-knit men's shirts ($2.5 billion). All the five items on Bangladesh's top exports list were ready-made garments of various types.

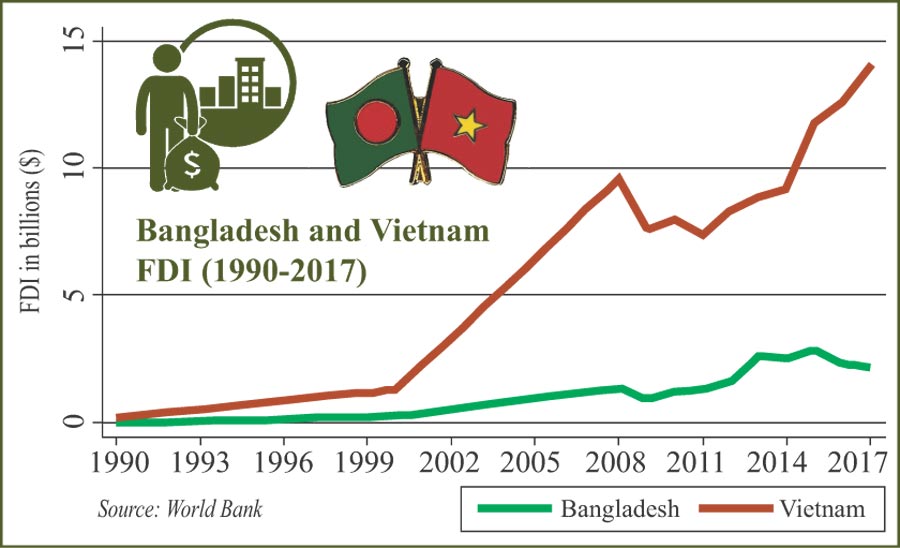

Similarly, in the area of foreign direct investment (FDI), Vietnam was remarkably successful in attracting FDI. Prior to 1990, both Bangladesh and Vietnam received little FDI. However, since 1990, FDI flows to Vietnam had been increasing by leaps and bounds, reaching $14 billion in 2017. On the other hand, the volume of FDI flows to Bangladesh has been mostly tepid and even in the best of recent years, not exceeding much above the 2.0 billion-dollar mark (see Figure 3).

Figure 3: Foreign Direct Investment in Bangladesh and Vietnam (1990-2017)

Most FDIs in Vietnam come from South Korea, Singapore, Japan and Taiwan, countries in which manufacturing costs are much higher than in Vietnam. FDI also played a critical role in changing the composition of exports of Vietnam. The share of high-tech in total exports from Vietnam went from 5.0 per cent in 2010 to 25 per cent in 2015 and kept on increasing with few signs of abating. Investments by electronics giants Hon Hai Precision, Intel and Samsung -- worth billions of dollars -- have been instrumental in causing the shift in composition. Electronics are replacing traditional manufactured products such as garments and shoes.

Vietnam's determined policy of openness to trade and investment paved the way for significant gains in export competitiveness. Growing on the backbone of global value chains (GVCs), Vietnam has emerged as an Asian manufacturing powerhouse specialising in assembly functions by primarily foreign firms. According to the General Statistical Office of Vietnam, FDI accounted for 71.5 per cent of total exports in 2016 (up from 47 per cent in 2000), while the contribution from foreign companies towards the overall GDP increased to 18 per cent from 13 per cent over the same period. Many domestic electronics and automotive companies in Vietnam have also successfully integrated into GVCs. In general, Vietnam has emerged as an assembly platform, specialising in final production stages, including information and communications technology hardware and textiles and apparel as well as a supplier of low-value added intermediate inputs into GVCs.

The Vietnam government continues to focus on attracting FDIs, especially in sectors that facilitate technology transfer, increase skill sets in the labor market, and improve labour productivity, help it to move up the GVCs.

Key to Vietnam's evolving economic miracle: Both Bangladesh and Vietnam experienced significant structural changes since the 1990s. However, from the perspective of pure structural change, the performance of both the countries are in many ways comparable (though from the pure metric of structural change, Bangladesh appears to be slightly ahead of Vietnam in tertiarising the economy). However, Vietnam has had a much better success than Bangladesh in modernising its economy, achieving both rapid growth and poverty reduction.

How does one explain this success of Vietnam? First, though Vietnam and Bangladesh both have the advantage of low wages and favourable demographics, Vietnam has leveraged its favourable demographics through effective investment in its people, which has includes promoting access to quality primary education and ensuring minimum standards. Vietnam has a better educated workforce (90 per cent literacy versus around 70 per cent for Bangladesh) than Bangladesh. Vietnam is also politically stable and geographically close to major GVCs. However, this is not the central element of the story, which lies in its strong underpinning of good policies.

First, Vietnam embraced trade liberalisation with a vengeance. These trade agreements brought about dramatic reductions in tariffs, helped lock difficult domestic reforms, and opened the economy to foreign investments. It is estimated that more than 10,000 foreign companies operate in Vietnam today, mostly in export-oriented, labour-intensive manufacturing.

Second, Vietnam complemented its programme of external liberalisation with its relentless pursuit of domestic reforms to enhance its international competitiveness and improve the investment climate. This is reflected in such indices as the Global Competitiveness index 2018 ( Vietnam ranks 55th while Bangladesh ranks 99th among 137 countries) and the World Bank's Ease of Doing Business (World Bank 2018), which ranks Vietnam 66th out of 190 countries --ahead of Indonesia (72), China (78), India (100) and Bangladesh (177).

Finally, Vietnam is at a relative vantage point compared to its comparator countries in infrastructure development. The country invested heavily in infrastructure, especially in the power sector and trade connectivity. According to Asian Development Bank, Vietnam spends 5.7 per cent of GDP on infrastructure -- the highest figure in Southeast Asia and also ahead of India -- but still falls short of China's 6.8 per cent. Due to high public investment, the country was able to expand its capacity in power generation, transmission, and distribution to meet the rapidly growing demand of industrialisation. Similarly, to keep pace with rapidly growing container trade -- which expanded at a staggering average annual rate of 12.4 per cent between 2008 and 2016 -- Vietnam also developed its connective infrastructure, particularly seaports and marine terminals.

Even though a former communist country, Vietnam appears to have learnt the fundamentals of rapid growth in a market economy faster than Bangladesh and many other emerging market economies. By zealously pursuing policies that combine privatisation, openness, competition and market incentives, along with appropriate investments, it has evidently outperformed Bangladesh in the dynamics of economic development.

...............................................

Dr. Quibria, a former Senior Adviser, Asian Development Bank Institute, is a Distinguished Fellow at the Policy Research Institute of Bangladesh (PRI) and Professor of Economics at Morgan State University, USA. This article is adapted from a forthcoming book, Bangladesh's Road to Long-term Economic Prosperity: Risks and Challenges ( Palgrave, Macmillan).

mgquibria.morgan@gmail.com

© 2026 - All Rights with The Financial Express