![]() The experience of economic growth shows that it is associated with structural transformation of the economy, which gets reflected in the structure of output as well as employment. When one talks about growth and structural transformation of an economy like that of Bangladesh, it would be important to bear in mind another important matter. Such economies are characterised by the existence of dualism. A large part of the economy, especially agriculture and other rural activities, is conducted along traditional lines, and is characterised by the existence of surplus labour and disguised unemployment (or underemployment). On the other hand, a small part of the economy consisting of manufacturing and other such sectors is conducted along modern lines. Investment in the modern sectors leads to growth and expansion in their share in the economy - in both output and employment. Such sectors can continue to employ labour without raising the real wages and thus grow in size as long as surplus labour exists in the traditional segment of the economy. As this process continues, surplus labour gets exhausted at some point, and further employment after that point leads to a rise in real wages.

The experience of economic growth shows that it is associated with structural transformation of the economy, which gets reflected in the structure of output as well as employment. When one talks about growth and structural transformation of an economy like that of Bangladesh, it would be important to bear in mind another important matter. Such economies are characterised by the existence of dualism. A large part of the economy, especially agriculture and other rural activities, is conducted along traditional lines, and is characterised by the existence of surplus labour and disguised unemployment (or underemployment). On the other hand, a small part of the economy consisting of manufacturing and other such sectors is conducted along modern lines. Investment in the modern sectors leads to growth and expansion in their share in the economy - in both output and employment. Such sectors can continue to employ labour without raising the real wages and thus grow in size as long as surplus labour exists in the traditional segment of the economy. As this process continues, surplus labour gets exhausted at some point, and further employment after that point leads to a rise in real wages.

The process of economic growth in dual economies described above is normally associated with structural transformation in both output and employment. At the initial stages of growth, the share of agriculture declines and that of manufacturing increases. After a certain stage, the share of manufacturing does not increase further; at that point, the share of the service sector starts rising.

The pattern of structural transformation described above is reflected quite well in the experience of the currently developed countries like the UK, the USA, France, and Germany. The experience of the countries in the developing world that have been successful in attaining development, e.g., Republic Korea, Taiwan, Malaysia, is also similar to those of the developed nations. During the early stage of economic growth, the share of manufacturing in GDP and total employment increased. And surplus labour available in the traditional sector was productively employed in the manufacturing sector because of high growth in both output and employment in the latter. If one looks at the level and pattern of growth of the manufacturing sector in these countries, one can see that it played the role of the engine of overall economic growth. A couple of other countries of Southeast Asia, viz., Indonesia and Thailand, have also made good progress in this respect.

During the 1960s, South Korea not only attained high rate of GDP growth, growth in its manufacturing sector was about twice that of economic output. In other words, when GDP growth was 8.0 per cent growth of manufacturing was 16 per cent. During the 1970s, growth of manufacturing was 1.8 times GDP growth too. In Malaysia, for more than two decades, during 1970 to 1996, growth of manufacturing output was between 1.5 and 1.8 times that of GDP growth. In those countries, not only did manufacturing output grew at high rates; during the early stages, the foundation was provided by export-oriented labour-intensive industries. And that pattern of industrialisation was key to the high rate of growth of productive employment.

The experience of Bangladesh shows that although there has been acceleration in economic growth, it cannot be said that manufacturing is its engine in the same way as in countries like Korea and Malaysia. During 1970s and 1980s, industrialisation took place along traditional lines, mostly through import substitution. GDP growth rates were low - didn't cross 5.0 per cent, and growth in manufacturing was also not remarkable. Growth of the manufacturing sector was not only low; in some years, it was negative.

During the nineties, growth of the economy as well as of the manufacturing sector started rising. The annual average growth of manufacturing output during 1992-96 was 8.21 per cent. But growth faltered in the subsequent years - going down to 5.64 per cent per annum during 1997-2001. But the situation started to improve after that, and the rate of growth crossed the two-digit mark in 2006.

The manufacturing sector of Bangladesh faces two more problems: instability in growth (i.e., fluctuations in growth from one year to the other), and concentration in one or two major sub-sectors. The problem of instability has been overcome in recent years - to some extent at least. But the problem of concentration in a narrow range of products remains. Only one industry, viz., ready-made garments - accounts for a very high proportion of the total output and employment of the sector. And there is very little sign of any change in that respect. A few other industries have come up in recent years; but their share in total output and employment of the sector is very low. On the other hand, the condition of most of the traditional industries like jute goods, paper, sugar, cement, fertilisers, etc., has deteriorated over time.

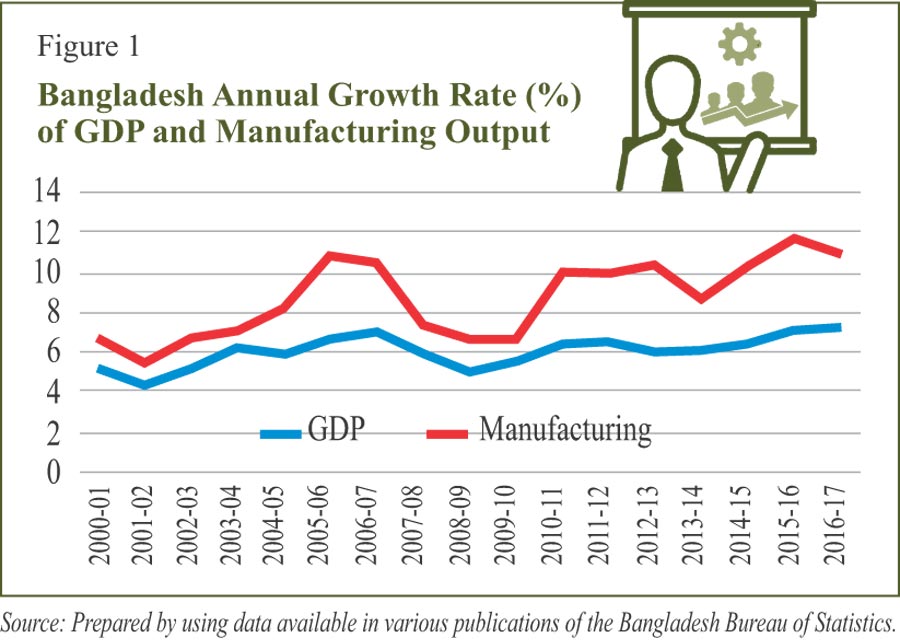

There was an acceleration in economic growth since the 1990s which attained further momentum during the 2000s. Figure 1 shows the trend in the growth of both GDP and manufacturing since 2000. It can be seen from this figure that the fluctuation in the growth of manufacturing continued during the recent years as well. One thing that is notable is that GDP growth exceeded 6.0 per cent in 2010, and crossed the 7.0 per cent mark in 2015-16. But growth of manufacturing was never even close to twice that of GDP growth - as was the case in South Korea during the early stage of their economic growth. In fact, growth of manufacturing was not even 1.8 times the GDP growth - something that Malaysia attained. Looked at this way, it can be said that manufacturing has not become the real engine of economic growth in Bangladesh.

There was an acceleration in economic growth since the 1990s which attained further momentum during the 2000s. Figure 1 shows the trend in the growth of both GDP and manufacturing since 2000. It can be seen from this figure that the fluctuation in the growth of manufacturing continued during the recent years as well. One thing that is notable is that GDP growth exceeded 6.0 per cent in 2010, and crossed the 7.0 per cent mark in 2015-16. But growth of manufacturing was never even close to twice that of GDP growth - as was the case in South Korea during the early stage of their economic growth. In fact, growth of manufacturing was not even 1.8 times the GDP growth - something that Malaysia attained. Looked at this way, it can be said that manufacturing has not become the real engine of economic growth in Bangladesh.

If one looks at the share of sub-sectors in the manufacturing sector's total output and employment, one can see that there has been very little change in the structure. For example, in 1999-2000, the share of the ready-made garment industry in the total output was about 37 per cent, which went down to 35.6 per cent in 2010-11 (the last year for which industrial survey data are available). The share of another important sub-sector - food processing - has also remained nearly static. And the shares of other industries like textiles, paper, pharmaceuticals and furniture have declined. Although there has been a rise in the shares of basic metals and non-metallic minerals, no new major industry is emerging.

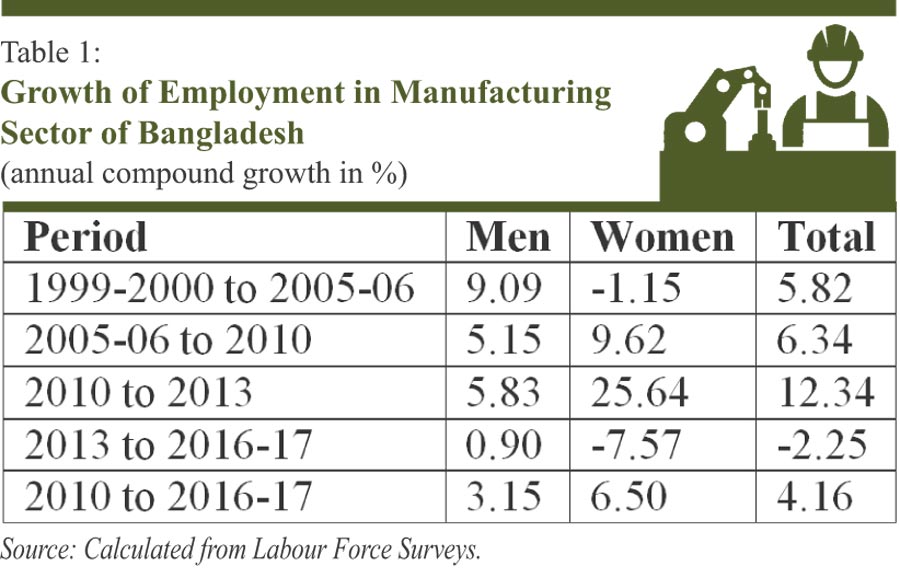

As there has not been much of a transformation in the structure of output, one cannot expect to see any notable change in the structure of employment. The shares of RMG and food processing remained virtually unchanged over the years mentioned above. And the share of textiles declined. Of course, the shares of basic metal and non-metallic minerals increased - as in the case of output. In sum, when one talks about manufacturing employment, the RMG industry remains the major source. Even in that industry, there has been a stagnation in employment in recent years. But before going into the details of that, it may be useful to go into some more details about manufacturing employment as a whole. Although the last survey of industries was carried out in 2010-11, data on employment in various sectors are available from labour force surveys - the last of which was carried out in 2016-17. A few remarks may be made on the basis of data presented in Table 1.

First, there was a notable acceleration in the growth of employment until 2013. And that was more so for women. But the picture changed completely after 2013. While the rate of growth of total employment was negative, the rate of decline was sharper for women. For men, although there was a decline in the rate of growth, it remained positive. In sum, between 2013 and 2016-17, women's employment declined sharply; and as a result, despite some growth in men's employment, overall employment declined.

First, there was a notable acceleration in the growth of employment until 2013. And that was more so for women. But the picture changed completely after 2013. While the rate of growth of total employment was negative, the rate of decline was sharper for women. For men, although there was a decline in the rate of growth, it remained positive. In sum, between 2013 and 2016-17, women's employment declined sharply; and as a result, despite some growth in men's employment, overall employment declined.

There is one view that the negative growth of employment between 2013 and the subsequent years is due mainly to an overestimation of employment in the survey of 2013. Although this author does not find much justification for this view, in order to take out any possible effect of the 2013 figures in the estimation of the growth of employment after 2010, growth rate between 2010 and 2016-17 has been calculated and shown in the last row of Table 1. If one compares those figures with the growth rates of earlier periods, one will note the decline in the rate of growth of employment over time. Conventional thinking on this might be that this is quite normal in the context of economic growth. At some stage of growth, labour productivity increases, and as a result, the rate of employment growth declines.

Of course, it is important for labour productivity to improve, because otherwise it would be difficult to justify increases in real wages. But as long as there is surplus labour in the economy, increases in labour productivity and employment should go together. That would make it possible to combine economic growth with improvements in labour productivity and employment growth. The experience of countries of East and Southeast Asia who were able to combine high growth with productive employment and succeeded in absorbing surplus labour quickly shows that this is possible. As the economy of Bangladesh still has surplus labour in its traditional sectors, the sharp decline in employment growth in the manufacturing sector is a matter to worry about.

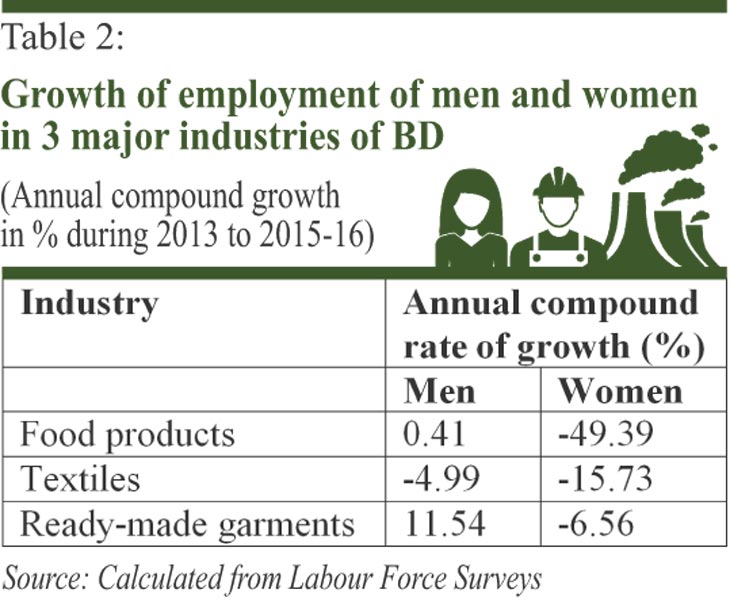

Data on the growth of employment in various industries shows that there was negative growth in food, textiles and basic metals. In the RMG industry, annual growth was only 1.84 per cent. Data presented in Table 2 shows that between 2013 and 2015-16, women's employment declined in three major industries, viz., food, textiles, and RMG. Men's employment in the RMG industry has increased substantially, but in food, their employment increased very little. In textiles, employment declined for both men and women.

Data on the growth of employment in various industries shows that there was negative growth in food, textiles and basic metals. In the RMG industry, annual growth was only 1.84 per cent. Data presented in Table 2 shows that between 2013 and 2015-16, women's employment declined in three major industries, viz., food, textiles, and RMG. Men's employment in the RMG industry has increased substantially, but in food, their employment increased very little. In textiles, employment declined for both men and women.

One naturally wonders why the employment situation in the manufacturing sector is so disappointing. This could be due to several reasons. First, if there is no growth in output, employment may not grow. Second, if labour-saving technology makes inroads in a big way, employment growth may be low even with output growth. Third, if the sector composition of the manufacturing sector changes in such a way that the weight of industries requiring less labour per unit of output increases, total output may grow without much increase in employment.

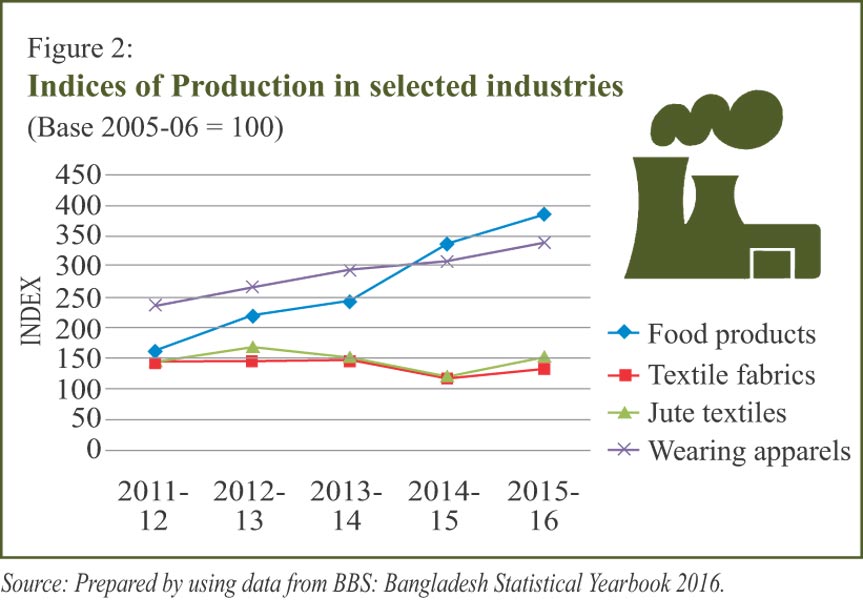

It is easy to argue that the first reason mentioned above is not applicable to Bangladesh because there has been healthy growth of output in the manufacturing sector. This point becomes stronger when one looks at output growth in different industries. It can be seen from figure 2 that the indexes of production in both RMG and food show substantial growth in output during 2011-12 -- 2015-16. In the case of jute goods, there was fluctuation in growth, but there was no noticeable downward trend. Production declined only in the textile industry.

On the other hand, we saw from Table 2 that there was a big slide in women's employment in both food and RMG industries. For men, there was good growth in the RMG industry but in food, growth was small. In textiles, there was negative employment growth for both men and women. And it is only for this sector that one could associate the decline in employment with a fall in output. In other industries, employment growth was disappointing despite output growth. Before addressing this question, we take a look at the data on employment and exports that are available from the website of BGMEA. Table 3 provides the data.

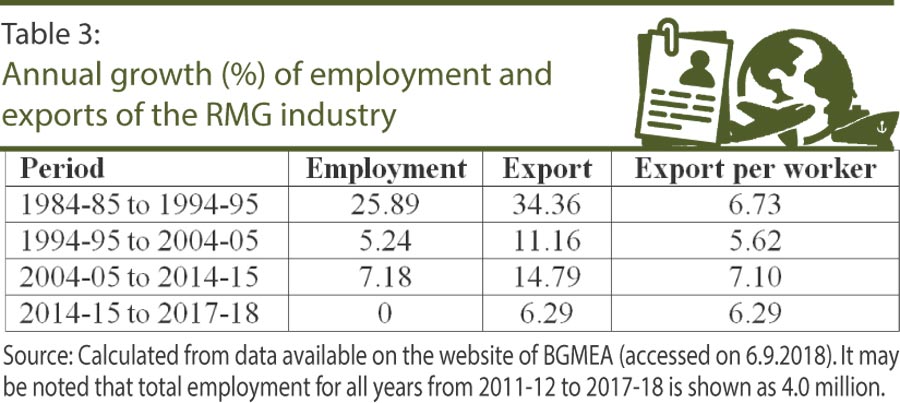

It can be seen from the data in Table 3 that although there was a decline in growth after 2014-15, export of RMG has continued to show substantial growth. Despite that, employment in the industry has not increased. In fact, the website of the BGMEA has been showing the same figure for employment since 2011-12. As exports continued to grow with employment remaining unchanged, export per worker has registered continued growth over time. In other words, labour productivity in the industry has increased.

It can be seen from the data in Table 3 that although there was a decline in growth after 2014-15, export of RMG has continued to show substantial growth. Despite that, employment in the industry has not increased. In fact, the website of the BGMEA has been showing the same figure for employment since 2011-12. As exports continued to grow with employment remaining unchanged, export per worker has registered continued growth over time. In other words, labour productivity in the industry has increased.

One other point to note is the decline in the number of factories in the RMG industry - from 5,876 in 2012-13 to 4,296 in 2014-15. Of course, the number increased to 4560 in 2017-18. It is well-known that after the Rana Plaza disaster in 2013, the industry faced a host of problems, the most notable among them being a concern about the safety situation of the factories. In the wake of the steps and programmes undertaken to improve the situation, a number of enterprises, especially the smaller ones were not able to meet the requirements and undertake necessary measures to upgrade their factories. That led to the closure of many factories. There is no data on how many workers lost jobs as a result of that. In view of the situation faced by the industry and the BGMEA showing unchanged figures for employment, one may naturally ask what is the real number employed by the industry at this moment.

As mentioned above, if employment does not increase despite increase in output, one reason could be the use of labour-saving technology. The present author is not aware of any research on this issue focusing on the recent experience of Bangladesh. However, based on some anecdotal information available from media reports and reports of international agencies, one can say that such technology is making inroads into the RMG industry of Bangladesh, and that could be one important reason for the decline in the use of labour. For example, a report in the Wall Street Journal (22 February 2018) mentions that their reporter found the use of machines made in Germany and Japan which require comparatively less labour than conventional machines. Not only that, some factory owners told the reporter that this trend is likely to continue. Likewise, in a report published in 2016, the International Labour Organization mentioned that labour use in the RMG industry of a number of Asian countries is going to decline due to automation.

As mentioned above, if employment does not increase despite increase in output, one reason could be the use of labour-saving technology. The present author is not aware of any research on this issue focusing on the recent experience of Bangladesh. However, based on some anecdotal information available from media reports and reports of international agencies, one can say that such technology is making inroads into the RMG industry of Bangladesh, and that could be one important reason for the decline in the use of labour. For example, a report in the Wall Street Journal (22 February 2018) mentions that their reporter found the use of machines made in Germany and Japan which require comparatively less labour than conventional machines. Not only that, some factory owners told the reporter that this trend is likely to continue. Likewise, in a report published in 2016, the International Labour Organization mentioned that labour use in the RMG industry of a number of Asian countries is going to decline due to automation.

Even if one leaves out the period before the independence of the country and the first decade after independence, one can say that industrialisation in Bangladesh now has a history of four decades. Even though this may not be long period in the history of a nation, for economic development and industrialisation, the period is not very short. Of course, the achievements of the country during this period are not insignificant. But what can be said about industrialisation? Yes, around four million people are employed in the RMG industry. And it is a major source of the country's exports and foreign exchange earnings. But what is there after this? One could mention pharmaceuticals, ceramics, bicycle, shipbuilding, etc. But their shares in the total output and employment of the manufacturing sector are rather small. The same remark can be made about their contribution to exports. On the other hand, the older industries like jute goods, paper, cement, fertilisers, etc., are merely surviving. What comes to mind when the term export-oriented industrialisation is mentioned - a number of labour-intensive industries growing simultaneously and contributing substantially to employment and exports - does not appear to have happened in Bangladesh.

While the RMG industry was able to generate employment for a large number of workers, the picture seems to have changed already. It has become important to undertake an in-depth research on what has happened to the employment situation of the industry and what has led to the recent changes. It is natural for technology to change any economic activity. When the use of new technology leads to changes in labour use, it is not possible to prevent the use of such technology. Nor would that be desirable. But it is important to see that the process is not encouraged by wrong policies.

The decline in women's employment in the manufacturing sector is definitely a matter to worry about. In that context, it would be important to analyse why their employment is declining in the RMG industry where men's employment has not declined. If the introduction of new technology has resulted in a decline in labour use, the impact should have been similar for both men and women. Hence, it would be important to ask why only women's employment has declined.

There is no alternative to structural transformation in the manufacturing sector - as also in the economy as a whole. Bangladesh has passed the stage of development where growth of a single industry was considered a matter of satisfaction. It is high time we look at the possibility of a broad-based export-oriented industrialisation based on the comparative advantage that the country possesses. In fact, such an investigation should start from why export-oriented industrialisation in the country has remained limited to only one industry and why other industries in which the country has potential have not grown. As mentioned at the outset, there are success stories in this respect. On the one hand, there are examples of countries like South Korea, Malaysia and Taiwan. There are examples of countries like Vietnam on the other. It should not be difficult to formulate appropriate strategies for lifting our manufacturing sector to a higher level by combining the lessons from the success stories mentioned above and from our own experience. What is necessary is the right vision and willingness, and of course, an ability to rise above parochial interests.

The author, an economist, is former Special Adviser, Employment Sector, International Labour Office, Geneva. rizwanul.islam49@gmail.com

© 2026 - All Rights with The Financial Express