![]() There is consensus among economists that proper management of the exchange rate is critical for ensuring export competitiveness and a superior export performance. In an economy where export is a key driver of growth, misalignment of the exchange rate could be disastrous for economic growth. If the real exchange rate is over-valued, it serves as a major disincentive to exports by stifling profits. Indeed, cross-country evidence reveals that economies that have successfully promoted export-oriented growth policies have not only avoided a real appreciation but instead have pursued policies of under-valuing their exchange rates at one time or the other. According to Dani Rodrik of Harvard University, China is the most recent example of an economy that under-valued its currency for a sustained period of nearly 30 years (1970-2000) to reap the benefit of accelerated export and GDP growth.

There is consensus among economists that proper management of the exchange rate is critical for ensuring export competitiveness and a superior export performance. In an economy where export is a key driver of growth, misalignment of the exchange rate could be disastrous for economic growth. If the real exchange rate is over-valued, it serves as a major disincentive to exports by stifling profits. Indeed, cross-country evidence reveals that economies that have successfully promoted export-oriented growth policies have not only avoided a real appreciation but instead have pursued policies of under-valuing their exchange rates at one time or the other. According to Dani Rodrik of Harvard University, China is the most recent example of an economy that under-valued its currency for a sustained period of nearly 30 years (1970-2000) to reap the benefit of accelerated export and GDP growth.

Over-valued real exchange rate: A review of Bangladesh's exchange rate trend reveals a mix of good news and bad news. The good news is that Bangladesh transited into a floating exchange rate system in 2003 without any consequential shocks. Since then the regime has been one of "managed float" that worked reasonably well for exports up until the financial crisis of 2007-08. The nominal exchange rate (Taka per US dollar) depreciated modestly leaving the real effective exchange rate (REER) stable (REER is the nominal exchange rate adjusted for inflation differences between Bangladesh and its major trading partners). Exporters got the benefit of more Taka (Tk) for every dollar ($) of exports.

Over-valued real exchange rate: A review of Bangladesh's exchange rate trend reveals a mix of good news and bad news. The good news is that Bangladesh transited into a floating exchange rate system in 2003 without any consequential shocks. Since then the regime has been one of "managed float" that worked reasonably well for exports up until the financial crisis of 2007-08. The nominal exchange rate (Taka per US dollar) depreciated modestly leaving the real effective exchange rate (REER) stable (REER is the nominal exchange rate adjusted for inflation differences between Bangladesh and its major trading partners). Exporters got the benefit of more Taka (Tk) for every dollar ($) of exports.

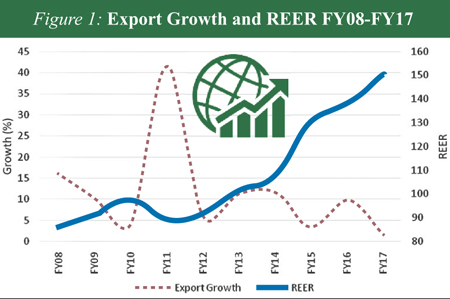

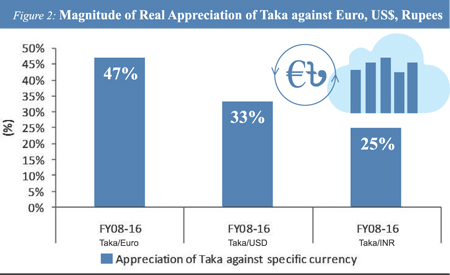

Things began to change since around the global financial crisis, particularly after fiscal year 2011. The REER estimated by Bangladesh Bank has been trending upward since FY2008 and, except for the export blip in FY2011, exports have been sluggish at best (Fig.1). The nominal exchange rate shot up from Tk.70 to Tk.80 per dollar by close of FY2012, then remained at that level for the next five years, while annual domestic inflation averaged at 7% during that period compared to barely 2% for EU and USA, and 6% for India. This inflation differential along with a fixed nominal exchange rate explains the significant appreciation of the real exchange rate against these countries (Fig.2).

Bangladesh's balance of payments has been stable for the past 25 years or so with the overall balance yielding positive reserve accumulation for several years in a row. Any rise in the merchandise trade deficit has been duly offset by remittance inflows to yield a modest current account surplus of 1-2 percentage of GDP in most years since 2001. Lately, a slowdown of remittances, sluggishness in exports, and a pickup in import volumes have combined to turn the current account surplus into a deficit. A negative current account is not something to be alarmed about if this is the result of robust import-intensive investment. This can be expected to yield employment and output growth that will be sufficiently rewarding for the economy. However, if this happens owing to slow down of exports, as seems to be the case in Bangladesh presently, then policy actions need to be swiftly taken to stimulate exports.

Bangladesh's balance of payments has been stable for the past 25 years or so with the overall balance yielding positive reserve accumulation for several years in a row. Any rise in the merchandise trade deficit has been duly offset by remittance inflows to yield a modest current account surplus of 1-2 percentage of GDP in most years since 2001. Lately, a slowdown of remittances, sluggishness in exports, and a pickup in import volumes have combined to turn the current account surplus into a deficit. A negative current account is not something to be alarmed about if this is the result of robust import-intensive investment. This can be expected to yield employment and output growth that will be sufficiently rewarding for the economy. However, if this happens owing to slow down of exports, as seems to be the case in Bangladesh presently, then policy actions need to be swiftly taken to stimulate exports.

Export growth can be stimulated through various policies of which a proper exchange rate management is crucial. Without pushing the case for an under-valued real exchange rate, there is no justification for letting the REER appreciate for too long as is the case for Bangladesh. For example, Fig.1 shows clearly that the REER has appreciated by 50% between 2008 and 2017. Such appreciation is hurting the exporters. Country's export performance has also been sluggish in recent years. A fixed rate of Tk.79-80 for a US dollar of export proceeds for almost five years when global competition has depressed export prices and higher local inflation has increased the cost of production, has shaved a good chunk off the already razor thin margins that exporters eke out on the world market. No wonder exporters are searching for relief out of this conundrum.

The policy dilemma: Exporters would love to see the nominal exchange rate depreciate significantly (i.e. yielding more Taka per dollar of exports) to compensate for the loss on the inflation front. But Bangladesh Bank has avoided letting the exchange rate slide for the fear of fueling inflation. Is there a way out?

A way out: compensated depreciation. A policy of 'compensated depreciation' could be an option for policymakers to consider. This involves an exchange rate depreciation that is counterbalanced by downward tariff adjustments. Such a measure might

a) prove to be an incentive to exporters,

b) help maintain protection level for import substitute producers,

c) have neutral effect on the price level and

d) be revenue neutral.

Here is how it works. In principle, a 10% depreciation of the exchange rate (say, from Tk.80 per dollar to Tk.88) is equivalent to a 10% subsidy on exports, a 10% increase in effective protection on import substitutes (because it raises tariffs on output and inputs equally). It also raises the value of imports by 10% to yield extra revenue. But this would also affect prices of imports and import substitute products upward by 10%, which leads to the fear of currency depreciation fueling inflation. That is where the compensation principle kicks in. If tariffs are then reduced by 10%, the price effect of the currency depreciation would be neutralized. The net result is a 10% uniform (i.e. non-discriminatory) incentive to all exports but without increasing the prices of imports. Effective protection and revenues will remain unchanged. We have worked with 10% hypothetical depreciation in order to explain the principle. The actual applicable rate will have to be determined after careful simulation of exports, imports and revenue impacts.

A better export performance is an absolute imperative if the targets of the 7th Five-Year Plan on industrial and GDP growth are to be achieved. Whereas cash subsidies on exports can create budgetary pressure and risk violating WTO rules, the depreciation would be a WTO-compliant trade measure that could stimulate exports for an economy that is a price-taker in the world market and, theoretically speaking, faces limitless markets for its exports, if it can produce competitively. That is what explains the fact that the world market for readymade garments is still open and Bangladesh's share could be much higher than the 6% that it currently commands.

Implementation issues: In a 'managed float' environment, depreciation is not the same as devaluation under the old fixed exchange rate regime when the central bank could simply fix the exchange rate. Under the present system depreciation could come from some liberalization of imports or other current account transactions (e.g. raising the foreign exchange limit for foreign travel for business, health or education). Regarding compensated reduction in tariff, in principle, it is possible to uniformly shave off 10% from all tariffs that will, for example, result in a 2.6% reduction in our average nominal tariff (including protective supplementary duties) of about 26%, in FY2018. Expert advice is locally available on how to rationalize the tariff structure to counterbalance any rate of depreciation without undermining the existing rate of effective tariff protection. And of course the across-the-board tariff cut would have to wait till the formulation of the next budget.

Concluding remarks: From the perspective of long-term incentives for exports, along with compensated depreciation to offset the real exchange rate appreciation, the government may wish to consider two other policies. First is to reconsider its inflation target of 6% and instead aim at reducing inflation to 3-4% level with a view to aligning better with inflation in partner countries. Second, it may want to reform its complex system of international trade taxes that seriously distorts incentives against exports and favors production for domestic sales. Evidence shows that trade protection has not contributed systematically to the growth of the manufacturing sector. Instead the manufacturing sector has benefited most from the export-oriented RMG industry. The justification for continual trade protection on grounds of nurturing manufacturing growth continues to remain very weak.

Sadiq Ahmed is Vice Chairman of the Policy Research Institute. sadiqahmed1952@gmail.com

Zaidi Sattar is Chairman of the Policy Research Institute.

zaidisattar@gmail.com

© 2026 - All Rights with The Financial Express