![]() For the first time since the Great Recession of 2008, spring has come to the global economy. This year, the International Monetary Fund (IMF) revised its short-term expectations for global economic growth upward for the first time in six years -- in both vintages of its semiannual report, the "World Economic Outlook". The month of October saw policy-makers and leading economists of the global financial and economic system gather in Washington for the Annual Meetings of the IMF and World Bank. For once economists concurred -- which is a rarity in itself -- that the world economy has not experienced such a period of strong and synchronised growth for the last 10 years. Not surprisingly, the question floating around Washington is whether this upswing is sustainable, or is it just another flash in the pan only to be derailed by some unprecedented shock?

For the first time since the Great Recession of 2008, spring has come to the global economy. This year, the International Monetary Fund (IMF) revised its short-term expectations for global economic growth upward for the first time in six years -- in both vintages of its semiannual report, the "World Economic Outlook". The month of October saw policy-makers and leading economists of the global financial and economic system gather in Washington for the Annual Meetings of the IMF and World Bank. For once economists concurred -- which is a rarity in itself -- that the world economy has not experienced such a period of strong and synchronised growth for the last 10 years. Not surprisingly, the question floating around Washington is whether this upswing is sustainable, or is it just another flash in the pan only to be derailed by some unprecedented shock?

By and large, the world economy has sprung along undeterred since the summer of 2016. American stock index, the S&P 500, which is widely considered a harbinger of world economic health is breaking through the roof, reaching record highs every other week. Investor confidence remains sky-high despite two of the biggest political upheavals the world has ever seen - Brexit and Donald Trump's ascension to American presidency.

So why are investors so confident? For one thing, US economic performance has improved steadily for the last few years. Corporate earnings continue to grow, while wage growth is still low, signalling higher corporate profitability. Unemployment rate is at historic lows, less than 4.5 per cent compared to almost 10 per cent during the peak of the financial crisis. Many also believe that the economy will accelerate further if the new American administration can carry out some of its promises made during presidential campaign.

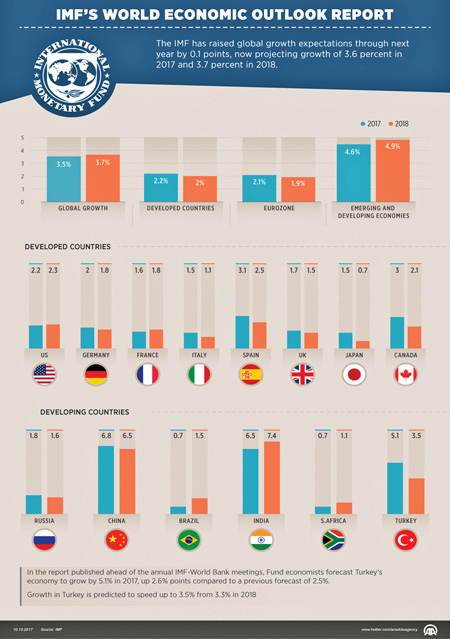

Economic activity has also gained momentum on the other side of the Atlantic. This year, the IMF expects the Eurozone economy to grow at its fastest pace since 2007. Unemployment rate fell to 9.1 per cent in June, the lowest level in eight years. The European Central Bank's chief economist, Peter Praet, is among those who believe that growth in the single currency area is not only more broad-based, but also resilient to political and external shocks. That Brexit did little to derail growth, serves as a good pointer. Inevitably, both the US and the European central banks recently announced an end to years of ultra-loose monetary policy (albeit the American Federal Reserve is tightening at a fast pace than its European counterpart). Essentially, these central banks are telling the world that their economies are back on firm footing.

Economic activity has also gained momentum on the other side of the Atlantic. This year, the IMF expects the Eurozone economy to grow at its fastest pace since 2007. Unemployment rate fell to 9.1 per cent in June, the lowest level in eight years. The European Central Bank's chief economist, Peter Praet, is among those who believe that growth in the single currency area is not only more broad-based, but also resilient to political and external shocks. That Brexit did little to derail growth, serves as a good pointer. Inevitably, both the US and the European central banks recently announced an end to years of ultra-loose monetary policy (albeit the American Federal Reserve is tightening at a fast pace than its European counterpart). Essentially, these central banks are telling the world that their economies are back on firm footing.

Buoyancy is back in the world's third largest economy as well - Japan. Stronger private consumption, investment and external demand propelled growth momentum in the first half of the year. To put it in context, Japan's growth in the second quarter of this year marked its longest streak of unbroken economic expansion (that is one without any quarter of growth below zero) in more than a decade!

To cap it off, even some big emerging markets (EM) have cause for celebration. Higher external demand, particularly from advanced economies, supported growth for several economies in East Asia. Brazil returned to positive growth trajectory in 2017 after arguably its worst recession in history. Growth in Mexico picked up despite lingering uncertainties about trade relations with America.

There are several possible factors that could explain this broad-based improvement in global economic activity after almost a decade of anemic growth. For starters, the emergency actions taken by the big central banks (US Federal Reserve, European Central Bank, Bank of Japan) has helped speed up the recovery. It's not difficult to imagine that pumping in zero-interest credit and telling the world that borrowing costs will remain low for a long time will eventually encourage people to borrow and spend. Improvements in financial regulation, particularly in America, may have had something to do with it. Commodity prices have stabilised somewhat. Or maybe this is simply a cyclical recovery -- advanced and big emerging markets do tend to have periodic episodes of booms and busts.

What is encouraging though is a rebound in world trade growth. For much of the last 10 years, world trade volume failed to rebound in line with GDP. But this long and disappointing trend may finally have come to an end. Gavyn Davis, former chief economist of global investment bank Goldman Sachs, identified growth in world trade volume recently outstripped that in world output for the first time during the recovery.

To be sure, the era of zero-interest rates may be coming to an end, but rates will still remain relatively low (say, 1-2 per cent for benchmark rates). The upshot is that income and demand are rising across the world, confidence is high and people will still have access to affordable credit to buy whatever they want. One would be tempted to think perhaps this time, after 10 painful years, a new age of global economic prosperity is about to begin.

If only that was true. The world has a new enemy: rising protectionism in trade and migration policies. For a world that was led by free-flow of goods and labour for decades, protectionist measures will undoubtedly hurt growth in jobs and reduce potential output (a measure of how fast an economy will grow if it runs at full capacity). The reverberations of such policy blunders will be felt across the world -- developed and developing - reducing confidence and possibly pulling the world back into the age of lacklustre economic performance that it has seen for much of the last 10 years.

It was inequality that led to this new world of protectionist sentiment, and inequality is here to stay. Unless the leadership in advanced economies muster the political will to strengthen labour force participation, reform product markets, improve tax policy, boost infrastructure and incentivise skill development. We are yet to see any serious reforms in that direction. If the current recovery is in part cyclical, then the lack of such structural reforms in major economies will eventually pull down economic activity once again. Combined with relatively low interest rates, one can easily envisage inflated goods and asset markets that can again lead to a crisis when the bubble bursts, as it has to eventually.

And the foundations for a painful asset market correction may already be in place. Take the United States stock market for instance. All major stock indices are at historic highs. True, investors have some reason to feel confident, given this synchronised global recovery. Yet this belief appears disconnected from certain ground realities. For instance, the US administration's plans for massive tax cuts will escalate national debt, ultimately diminishing growth. Protectionist trade policies will have similar damaging effects. In either case, investors will have to reassess their outlook on long-term growth prospects and reduce expectations. While a selling-spree will first hurt financial markets, loss of confidence will eventually dent real economic activity. The spillover effects on the rest of the world, particularly in terms of trade and financial flows, could undo much of the recovery.

Ironically, stock markets have become almost insensitive to geopolitical events (Brexit, Donald Trump's rise to American presidency) as well as global security threats. So much so that markets are almost completely ignoring risks of a military conflict between the United States and North Korea. It's been more than 50 years since the United States and the Soviet Union banned atmospheric nuclear tests. And now, Kim Jong-Un's government is stoking global fears of such nightmares. Mike Pompeo, director of the Central Intelligence Agency (CIA), was recently quoted by the Financial Times that North Korea could be just 'months away' from developing the capacity to strike the US with a nuclear-armed ballistic missile. It goes without saying that such catastrophic military development could inflict severe damage to global confidence and stability. And the American administration's threatening retaliations does little to manage what is fast becoming a calamitous scenario.

If that's not enough, a debt bubble is brewing in the world's second largest economy: China. In the aftermath of the Great Recession, China's manufacturing and export-dependent economy was hit hard. In a bid to protect their rule, political leaders unleashed a wave of monetary easing never seen before in history: gigantic volumes of easy loans channelled through the country's state banks. The economy's total debt sky-rocketed from $6.0 trillion at the time of the crisis to around $28 trillion at the end of last year. That's 250 per cent of China's GDP. The effectiveness of this debt-financed growth is fading rapidly as well. Before the crisis, analysts estimated that one additional unit of debt (say in terms of Chinese Yuan) generated one additional unit of GDP. Now, four units of additional debt are needed to generate that same one unit of output. So it's no surprise that bad loans have doubled in the last two years while around 40 per cent of new debt is used to repay interest on existing loans.

History reminds us that this kind of debt binge is usually followed by a financial crisis, and for China it is now a question of when, not if. Some argue these fears are overdone since much of the debt is state-owned, so it is manageable. But that does not necessarily mean a solution will pop out of thin air if authorities do not take hard (and perhaps politically painful) but much-needed reforms to reduce its debt-dependence. Just like the US, an abrupt slowdown in China will be felt hard throughout the entire world.

So the preceding story encapsulates the idea that it was political short-sightedness that bred these global risks over time. And the lack of effective political leadership might again be the difference between sustainable global economic recovery, and a brief spell of euphoria. While it is easy to talk about 'financial inclusion', 'inclusive growth', 'jobs-for-all' and other such grandiose visions, the grit needed to make that a reality remains, by and large, absent. The world may strut along for now, but without this sort of leadership, it will remain unprotected from financial, political and economic shocks. When that hits, it's back to square one.

The writer is former Research Analyst at the International Monetary Fund, Washington D.C. and currently a Doctoral student in Economics at the University of North Carolina, USA.

shaque4@jhu.edu

© 2026 - All Rights with The Financial Express