As a country progresses from a low level of development to higher levels, its people would naturally aspire to have a better standard of living, which, for many, would depend on what they do for living and how much they earn from that. In other words, they need better jobs. When an economy develops, jobs can get better (not just in the sense of incomes but also in terms of other qualitative aspects) where one is already working or one can move to a better job in a different field. It is in that context that the issue of structural transformation comes in.

From agriculture to industry and then to services: Whether one looks at the historical experience of the developed countries or at the experience of countries that have succeeded more recently in their development efforts, one finds a common pattern in structural transformation. First, the share of agriculture in output and employment declines and the share of industry increases. At a subsequent stage of development, the share of industry starts to decline and the share of services increases.

When structural transformation happens in the sequence mentioned above, it helps people move from jobs with low productivity and returns to ones with higher incomes. For example, jobs in industry are usually characterised by higher productivity compared to agriculture, and those who are employed there earn higher. Hence, in a country that attains high growth of both output and employment in industries, workers can move from sectors with low productivity and incomes to jobs in industries.

The share of agriculture in output and employment has been on the decline. — FE Photo

One might ask what explains the pattern of structural transformation described above and whether this is the only pattern that would help people move to better jobs or there could be alternative pathways. The answer to the first question lies in the pattern of people's consumption. At low levels of income, a large proportion of it usually goes for food and the remaining goes for other basic needs like clothing and housing. When income increases, the proportion spent on food starts to decline and the share of expenditure on items like clothing, furniture, other household goods, etc. increases. As the latter are produced in the manufacturing sector, a rise in the demand for such goods creates market for them. And if other conditions for investment are conducive, investment in manufacturing starts to increase.

Of course, in an open economy, a country can import some of the goods produced by industries. So, an increase in demand may not lead to increased production. But such an economy also creates opportunities for exporting industrial goods. And a country with abundant labour should have comparative advantage in producing and exporting goods that are more labour-intensive. Thus, conditions favourable to the growth of manufacturing emerge. In general, a rise in the demand for industrial goods creates the necessary condition for the growth in the sector.

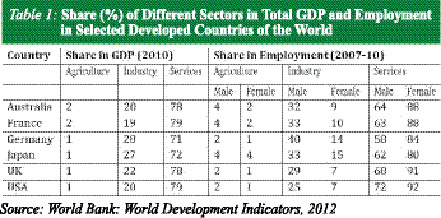

Experience of developed countries: The experience of the currently developed countries appears to fit well in the pattern of structural change outlined above. For example, structural change experienced by countries like France, Germany, the UK and the USA shows a roughly similar pattern: decline in the share of agriculture accompanied by an increase in the share of industries at the initial stages of growth, and a decline in the share of industries at a subsequent stage along with increase in the share of services. The share of agriculture in GDP ranged from a third to half in the UK, France and the USA during their journey towards development in the nineteenth century. This went down to about a fourth during the subsequent 75 to 100 years, and to around 5 per cent towards the end of the twentieth century. On the other hand, the share of industry went up to 50 per cent, and by the end of the twentieth century, declined to 30 per cent. By then, the share of services increased to 70 per cent. One notable feature of that structural change was a similar change in the structure of employment -- with the share of different sectors in total employment remaining close to that in output. This implies that economic growth did not result in a major difference in labour productivity in different sectors.

Figures in Table 1 show that the pattern of structural change described above continued during the past decade as well. The share of agriculture declined further to between 1 and 2 per cent, while that of services increased further to 78-79 per cent.

The change in the structure of employment also continued, although some gender-related differences are noticeable. In the manufacturing sector, the share of men is higher than that of women, while the opposite is the case in services. It seems that women are not being attracted to the industrial sector.

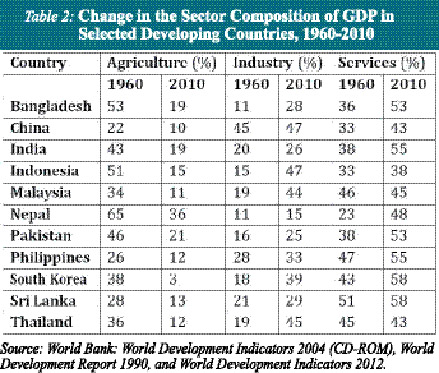

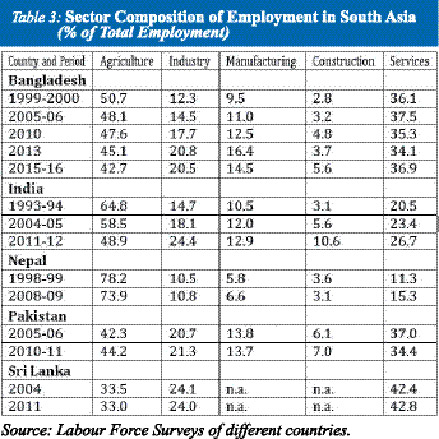

How developing countries doing: Turning to the currently developing countries, development in some of them seems to have followed a pattern like that of the developed countries mentioned above. Data for some Asian countries presented in Table 2 show such pattern for the Republic of Korea, Indonesia, Malaysia and Thailand. In these countries, the decline in the share of agriculture and increase in that of industries have been quite notable. Clearly, manufacturing in these countries has acted as the engine of growth. But the experience of the countries of South Asia has been different. In Bangladesh and India, for example, the decline in the share of agriculture has not been followed by a similar increase in the share of industry; the increase has been more than proportionate in services. This is particularly the case when one looks at the structure of employment (Table 3).

In order to understand the pattern of structural change in South Asian countries (and their contrast with countries of East and South-East Asia), it would be useful to look more closely at their growth rates and pattern. In Bangladesh, there has been a steady acceleration in economic growth since the 1990s: from an annual GDP growth of less than 5 per cent per annum, the country reached 6 per cent growth in a decade. In 2003-04, growth rate exceeded 6 per cent, and since then, hovered around that mark for some years. But growth rate exceeded 7 per cent in 2015-16.

Economic growth in India has been more impressive, especially since the mid-1990s. GDP growth rate started accelerating since 1994-95, and ranged between six and nine per cent per annum in most years thereafter. The annual average GDP growth in India has increased from six per cent during the 1990s to 7.6 per cent during 2000-2014.Sri Lanka also witnessed an acceleration in growth from 5.3 per cent during the 1990s to 6.1 per cent per annum during 2000-2014. Nepal and Pakistan's growth record is not so impressive, but Pakistan was able to raise its economic growth during the first half of the 2000s.

Despite such impressive rates of GDP growth, the slow rate of structural transformation in employment observed from Tables 2 and 3 is something to take note of. To understand this, one would have to look at the pattern of growth and its drivers. One important question is whether manufacturing has acted as the driver of growth (as mentioned above).

In Bangladesh, there has been very little difference between overall GDP growth and growth in manufacturing between 1995-96 and 1999-2000. The ratio increased to about 1.5 during 1999-2000 to 2005-06, but then declined to 1.23 during 2005-10. In India also, industry has not emerged as the driver/engine of economic growth. The elasticity of manufacturing growth with respect to GDP growth declined from 1.14 during 1990-2000 to 1.09 during 2000-2010. In Nepal, this elasticity has been declining steadily since mid-1990s and was negative after 2005. In Pakistan, the figure has fluctuated -- declining from 1.34 during the 1980s to 1.04 during the 1990s and then rising to 1.54 during the 2000s. In Sri Lanka, the elasticity varied from 1.6 during the 1980s to 0.7 during 2000-05.

In contrast to the South Asian countries mentioned above, in the Republic of Korea, the corresponding figure was over 2 during the 1960s, 1.8 during 1970-80 and 1.4 during 1980-90. In Malaysia also, the figure was between 1.5 and 1.8 during the 1970-96. In those countries, manufacturing played the role of engine of growth during the early phase of their growth. Moreover, the sector was dominated, at least initially, by labour-intensive industries. As a result, not only was the growth of output high, employment also expanded rapidly.

The conclusion that follows from the figures mentioned above is that in South Asia, manufacturing has not been the driver of economic growth the same way as it has been in countries like Korea and Malaysia during the early stages of their growth. But does manufacturing need to be the driver in all situations irrespective of their specific characteristics? To this question, we now turn.

Alternative pathways to structural transformation: The debate and some examples: Like in many areas of economic and development policies, the rationale for one-size-fits-all approach to structural transformation has also come into question. One line of argument in this context is: given the variation in resource endowment and circumstances faced by different countries and the current global economic environment, it may not be realistic to expect all developing countries to be able to follow the same path of economc growth and labour absorption. While the question may be quite relevant in the context of Africa where many countries faced declines in their manufacturing industries during the 1980s and 1990s and the service sector started showing good prospects of growth, the debate was extended to countries like India as well. Participants in this debate (including the likes of Dani Rodrik) take India's growing -- and somewhat premature -- dependence on the service sector for growth and employment as a sign of de-industrialisation. But this comes at a much earlier stage of development than that of developed countries, and hence, it is essential to see if services could indeed act as the driver of growth in countries like India (as well as Bangladesh). It would also be important to examine whether the alternative pathways to structural transformation would enable transfer of labour from low-productivity to higher-productivity activities.

Alternative pathways to structural transformation may include the service sector as well as diversification of agriculture itself. ICT-based economic activities in India, rural non-farm activities in Bangladesh, diversification of agriculture towards fruits and vegetables in Nepal, and tourism in Nepal and Sri Lanka are examples of such possibilities. In the rest of this article, we shall only look at the case of ICT in India and rural non-farm activities in Bangladesh. Based on these albeit limited experiences, some tentative conclusions about the potentials for alternative pathways to structural transformation will be drawn.

Take the case of ICT in India. During the couple of decades from around early 1990s, the ICT sector (defined as the total information technology and IT-enabled services) emerged as the fastest-growing sector and a major source of exports in India. The share of this sector in total GDP increased from about 3.0 per cent in 2000-01 to 9.5 per cent 2014-15. With an export worth nearly 75 billion US Dollars, the share of the sector in total exports was 15 per cent in 2014-15. That this is a highly export-oriented sector is indicated by the share of exports in the sector's output -- increased from 49 per cent in 2000-01 to 81 per cent in 2014-15. In 2015, the sector employed a total of 3.5 million people of whom 1.2 million were women. If one remembers that in 2004-05, the sector was employing just about one million people, it is easy to see the phenomenal growth attained, not only in terms of revenue and exports but also in terms of employment.

Although there is a perception that the ICT sector is urban-oriented, one survey (by NASSCOM) found that between a third and a half of the employees are from either non-metro or rural areas. As for education level of the employees, 75 per cent of the indirectly created jobs are filled by those with HSC or lower level of education. Proportion of women in total employment is also high, although they are over-represented in the low-skill end of the spectrum. The jobs in the sector offer flexibility in terms of working hours and the possibility of working from home. Thus, this sector would seem to have good growth potential and ability to generate much-needed jobs for the growing educated workforce.

However, when it comes to the question of an alternative pathway for structural transformation of a vast economy like that of India (with its regional variations), a few sobering remarks may be in order. First, growth rate attained by the sector seems to have slowed down in recent years. One calculation shows that ten-year annual average growth declined from a massive 40 per cent in 2002 to about 20 per cent in 2014. In fact, growth rate slowed down sharply in 2008-09 and became negative in 2009-10. Since then, growth has resumed, but has not gone back to the levels seen before 2008-09. Likewise, export growth has also declined and fluctuated in recent years -- although growth remained at a double-digit level. Second, even though the number engaged in the sector has increased several-fold, its share in total employment (or labour force) of 472 million (in 2011-12) remains rather small. Third, while the number of job-seekers with paper qualifications meeting the requirements of the sector may be well over its demand, many of them may not meet the standards in terms of technical ability and language skills.

One set of numbers that are rough and ready and yet could be illustrative may help put the above-mentioned issue in perspective. In India, if growth in labour force is taken to be 2.0 per cent per annum, over 9 million members may be expected to be added to the workforce of 472 million (as of 2011/12). The number engaged in manufacturing that year was over 60 million. If growth in output in manufacturing could be raised to, say, 12 per cent per annum (which is not at all unrealistic), and if elasticity of employment growth is assumed to be 0.5, the sector can generate around 3.6 million jobs per year. On the other hand, the ICT sector currently employs a total of about 3.5 million workers, and the growth in revenue in the sector has been slowing down in recent years. Even if the sector continues to grow at 15 per cent per annum (growth in 2014-15 was 13 per cent), given the current employment-generating capability of the sector, it will perhaps not generate more than 50 to 60 thousand jobs per year. And qualifications required for those jobs will perhaps range from a minimum of HSC to first degree in a technical subject.

The service sector in India accounts for more than a quarter of the currently employed population. But the sector is not an employment-intensive one, as is the case in many countries; and the employment intensity of the major components like trade and transport has been on the decline. Hence, even with the growth potential that exists in the sector and in components like the ICT sub-sector, the extent to which they can serve as a real alternative pathway for structural transformation of employment remains a question.

What about Bangladesh? Data presented in Table 3 indicate that structural transformation in employment has been rather slow in the country, especially if increase in the share of manufacturing is taken as the indicator. Of course, that does not mean that there has been no change in the structure of the economy and employment. On the one hand, there has been considerable diversification in the sources of income, especially in rural areas -- dependence on agriculture declining substantially. Alongside that change, development in physical infrastructures (e.g., roads, availability of electricity) has improved connectivity of rural areas with urban areas and rural centres of economic activities. That, in turn, has created necessary conditions for the growth of non-farm activities within rural areas.

The countryside of Bangladesh today offers a landscape that is very different from that of a few decades ago in that in many areas the difference between rural and urban areas gets blurred. It is true that in many instances, it is remittances received from workers working abroad that have transformed the lives and livelihoods of people. But there are also villages where cottage industries, small businesses, or non-traditional agricultural products like vegetables, fruits, flowers, etc. have contributed to some structural transformation in the economy. However, the important question to ask is whether such transformation is sufficient to move the overall economy to a stage where people engaged in low-productivity activities can move to sectors and activities where productivity and incomes are higher.

What kind of change has taken place in the structure of employment in the rural areas of the country? The share of manufacturing remained almost unchanged till 2010 and increased after that. But what kind of industries are they? They are basically very small and cottage industries where productivity is not very high. An indication of that is provided by the level of wages in the sector relative to that of agriculture. In 2013, wages in rural manufacturing were 21 per cent higher than in agriculture. On the other hand, the shares of construction, trade, and transport in total rural employment declined. And wages in those sectors are also not much higher than in agriculture -- the differences range from 7 per cent for construction to 25 per cent in trade. Given such small differences, it does not seem that rural Bangladesh is witnessing a transformation towards jobs that are better than the previous ones.

And that brings one back to manufacturing.

It is true that Bangladesh has not yet been able to launch a full-fledged drive towards export-oriented industrialisation; only one such industry (ready-made garments) has grown, and in that industry, not much additional employment has been created during the last few years. But even with the current limited degree of industrialisation, the manufacturing sector creates some 400,000 jobs annually, absorbing over a fifth of the annual addition to the labour force. The sector has the potential to grow at substantially higher rate than at present.

If its growth could be raised to 14-15 per cent per annum, and if its composition can be diversified with more labour-intensive industries, employment in the sector could grow at 8-9 per cent annually. And that would mean some 600,000 jobs per year -- or about a third of the additional labour force. The upshot seems to be that manufacturing remains the best hope for transferring people from jobs characterised by low productivity and incomes to better jobs.

The above is not to suggest that all manufacturing jobs are good jobs. That there are big quality deficits in many manufacturing jobs all over the developing world is by now well-known. But the point that is being made here is that from an economy wide-perspective, industrialisation seems to offer a more promising pathway for structural transformation towards better jobs.

Rizwanul Islam is Former Special Adviser, Employment Sector, International Labour Office, Geneva. rizwanul.islam49@gmail.com

© 2026 - All Rights with The Financial Express