The inflow of concessional loans for financing the national budget has remained lower than the original targets over the years, according to budget documents.

Such inadequate foreign funding for the budget leaves a negative impact on the government's ability to finance deficit.

The deficit is estimated at 5.0 per cent of the country's gross domestic product.

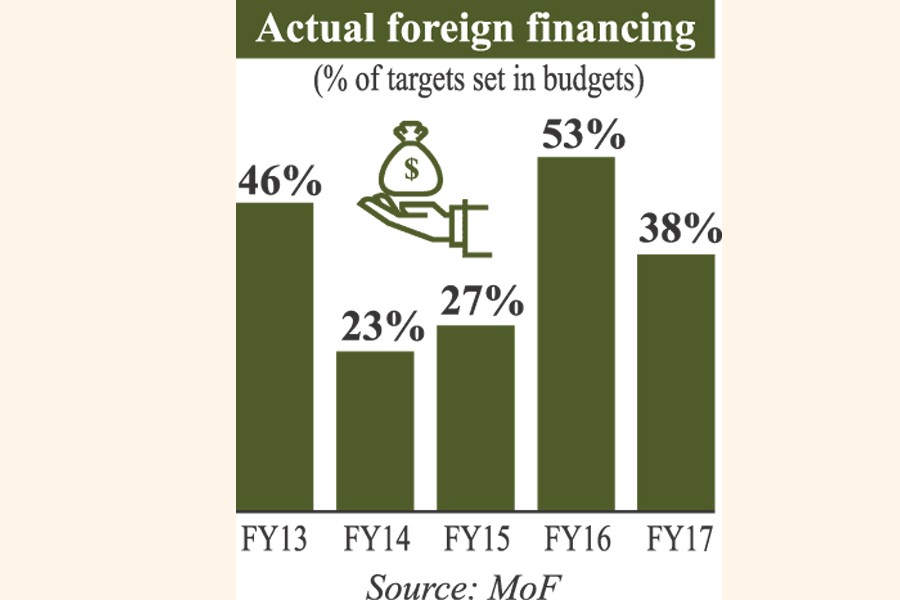

The average net inflow of the external aid for financing the budget is less than 40 per cent of the forecast made during the past five fiscal years (FYs), ending in the FY, 2016-2017, the documents show.

The actual foreign funding averaged 37 per cent, compared with the original estimation in the beginning of FY 2013, according to the documents.

In FY 2014, the actual inflow of foreign assistance for financing the budget was 46 per cent.

The percentage was 23 per cent in FY 2015, 53 per cent in FY 2016 and 38 per cent in FY 2017.

In the FY 2015, the projection for foreign financing for the budget was Tk 307.89 billion but the actual inflow was far lower at Tk 116.03 billion.

In FY 2016, the government expected Tk 243.35 billion but the actual funding was Tk 128.66 billion.

In FY 2015, the projection was made at Tk 180.69 billion and the actual inflow was Tk 49.09 billion.

In FY 2014, the foreign financing was expected to reach Tk 143.98 billion, but the actual receipt was just Tk 33.49 billion.

In FY 2013, the external fund was estimated at Tk 125.40 billion, whereas the inflow was Tk 58.12 billion.

Economists say the fund meant for different development projects is a reflection of the poor implementation capacity of the government agencies.

The World Bank, the Asian Development Bank (ADB), and the Japan International Cooperation agency (JICA) mostly pledged to provide the funds.

Dr. Zahid Hussain, lead economist at the Dhaka office of the World Bank, told the FE this lower inflow of foreign financing to the budget reflects the weakness on the part of the implementing agencies.

"Aid comes for projects and if projects get stuck, the financing gets slower," Dr Hussain said, explaining.

But he said this does not happen in case of food aid.

Officials at the finance division told the FE that the gap in budget financing is usually offset by domestic borrowing.

Domestic borrowing comes mostly through the national saving schemes.

Dr Mirza Azizul Islam, a former finance adviser, told the FE the only reason behind the situation is poor implementing capacity.

"If we cannot implement projects, then the disbursement will be poor," he said.

Dr Islam said the implementation rate of the annual development programme (ADP) also shrank in recent years.

This only highlights the rate of poor implementation of foreign-funded projects.

He said the implementing agencies should be held accountable for their failures in executing projects timely.

Referring to the Tk 500 billion estimate of external financing for the upcoming fiscal year, he said, "The disbursement target is unlikely to be reached."

The actual figures relating to external loan inflow meant for FY 2019 will be available two years later.

jasimharoon@yahoo.com

© 2026 - All Rights with The Financial Express