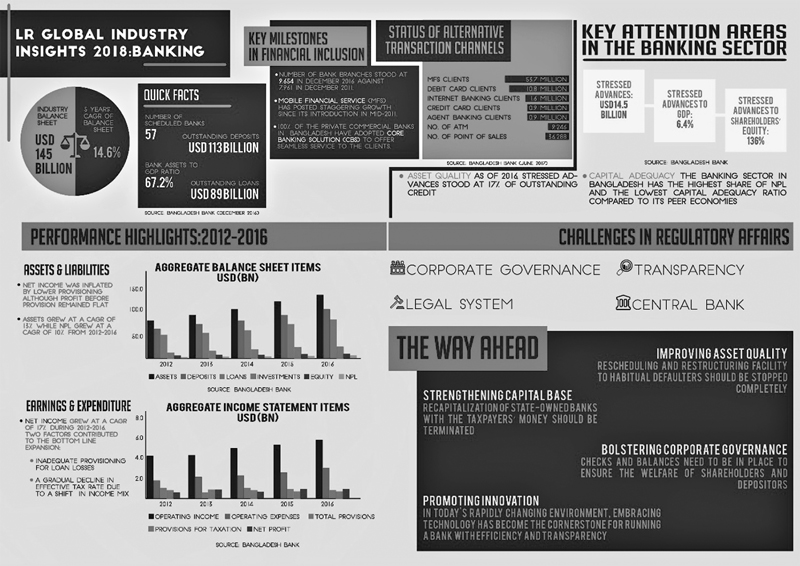

A s of 2016, the country's banks' stressed advances -- the summation of non-performing, restructured and rescheduled loans -- stood at 17 per cent of their total outstanding loans, according a research study conducted by LR Global Bangladesh, an affiliate of the New York-based LR Managers Investments.

s of 2016, the country's banks' stressed advances -- the summation of non-performing, restructured and rescheduled loans -- stood at 17 per cent of their total outstanding loans, according a research study conducted by LR Global Bangladesh, an affiliate of the New York-based LR Managers Investments.

In absolute terms, the size of NPL stood at USD 7.8 billion and that of restructured and rescheduled loans at USD 6.7 billion. At the same time, provision coverage exhibited a declining trend, indicating enhanced vulnerability of the entire banking sector.

"Although the NPL scenario in the SCBs gained more attention from different corners, the asset quality in the PCBs has also deteriorated to a serious level," the research paper noted.

In the last five years, it mentioned, the load of NPLs at PCBs grew at a faster pace than that of the SCBs.

As such, the study listed poor risk assessment of credits, subdued demand in the economy, rescheduling facilities to known defaulters, and mostly the culture of borrowers' unwillingness to repay loans as the major reasons behind the deterioration in the asset quality in Bangladeshi banks.

It also pointed out the futility of government dollops for feeding the capital-deficient banks, because of the snowballing of such bad loans.

"Despite the generous recapitalization of SCBs for the past nine years with taxpayers' money, there has been no material improvement in these banks' capital position, asset quality and profitability."

Only 20 per cent of the loans written off by the Bangladesh's banks have been recovered in the last 12 years, reveals the study.

Given the high level of non-performing loan in the system, the capital buffer to withstand any sudden deterioration in asset quality is lacking in Bangladesh, noted the research study.

Highlighting the recent amendment to the country's Bank Company Act, the research also bears a note of warning that the situation may lead towards further consolidation of power in the hands of too few as an outcome of asset concentration.

"The banking sector in Bangladesh has the highest share of NPL and the lowest Capital Adequacy Ratio compared to its peer economies," says the LR Global research report, adding that non-performing loans in the country's banking system have outpaced the credit growth in the last five years.

The study also observes that while the PCBs have maintained sufficient capital above the regulatory requirement, the major risk to their capital position is the solvency of the top borrowers at these banks.

"According to a stress test done by the Central Bank, default of top 3 borrowers in each of the banks would make 50% of the banks non-compliant in maintaining the minimum regulatory capital," said the research.

The LR Global research also noted that compared to the banking sector of its peer economies, the banking sector in Bangladesh is highly fragmented.

"Burdened with unrealistic 'business targets', banks involve in unhealthy competition and often provide cheaper credit to an already- struggling customer," the study says.

In addition, the research also observed that the pace of innovation remains 'strikingly low' in the banking sector of the country.

"Although 17 banks were granted license to operate Mobile Financial Service (MFS) in the country, the number of full-fledged MFS providers remains far below that," it said.

"Further problems have been created by the new banks, some of which are already under special observation just within four years of commencement," the study observed.

The researchers of the agency noticed that specialized banks created to foster agricultural lending and mobilizing investments from non-resident Bangladeshis put up a disappointing performance in achieving their respective targets.

In terms of regulations, the study says that while Bangladesh Bank has been very successful in terms of monetary-policy management, curbing inflation and building healthy forex reserves in the past few years, the regulator's success was limited in terms of curbing non-performing loans in the system.

"At the institutional level, deficiency in analytical capacities such as assessing macroeconomic risks and forecasting major indicators undermines the regulator's ability to take proactive policy measures," the research paper says.

In many cases, despite having an apt guideline, the implementation of the regulation remains a challenge.

The study also noted that while most of the banks in Bangladesh are already controlled by families or related businesses, a recent amendment to the Bank Company Act further exacerbated the situation.

As per the aforementioned amendment, PCB boards can have four members from the same family while the tenure of the directors has been extended from six to nine years.

"Although the policy move was aimed towards increasing the accountability of the directors, considering the current status of the industry, such a policy can backfire," the report has cautioned.

Noting a lack of transparency in the country's banking sector, the study focused on discrepancies among the banks in terms of disclosing the names of top borrowers, information on rescheduled and restructured loans, sector-based loan exposure and capital market exposure.

"The lack of such information often paints a distorted picture of the health of a bank and gives rise to information asymmetry among different groups of stakeholders, especially the common shareholders," the study says.

The LR Global research also blamed the stalemate in the recovery of assets on what it calls 'archaic legal environment' of the country.

"The absence of a strong legal system encourages the practice of willful defaults," the study said.

Besides, the duration and costs associated with liquidation and recovery of insolvent businesses slow down the recovery of impaired assets.

Citing the example of India, the research noted that Bangladesh's neighbouring giant, when faced with similar challenges, overhauled its bankruptcy code to reduce the time to resolve cases to 180 days from 4.3 years and create a pool of insolvency professionals to ensure a smooth transition and liquidation of insolvent firms.

While noting that in Bangladesh, the macroeconomic scenario is still resilient, the study forewarned that challenges, nevertheless, might+ emerge from rising inflation, subdued exports and remittances, rise in real interest rate due to increased government borrowing, devaluation of BDT and, finally, massive capital outflow due to "political uncertainty".

"Thus, the regulators cannot afford further denial and must take preemptive actions when there is still time," the US-based agency suggests.

mehdi.finexpress@gmail.com

© 2026 - All Rights with The Financial Express