Mohammad A. Razzaque and Syed Mortuza Ehsan | April 16, 2019 00:00:00

Very recently, the world economy has witnessed escalated trade tensions between the world's two largest trading nations, China and the USA, amid an already prolonged and severe crisis in trade multilateralism, and the protectionist measures that threaten to derail the rules-based multilateral trading system.

The recent bout of trade crises surfaced as global trade flows showed some encouraging sign of gaining momentum in trading activities not seen for the last several years now. Indeed, after six long years since 2011, a strong recovery in global trade flows was registered in 2017 with the world's total merchandise exports of goods and services rising by US$1.7 trillion over the previous year to reach $17.7 trillion. Yet, the value of global trade remained lower than that achieved in 2011 ($18.3 trillion). Last year's buoyant performance helped sub-Saharan African countries increase their exports by nearly $50 billion to just over $300 billion, which was still $150 billion less than their export earnings in 2011.

The world economy is badly in need of reviving and sustaining trade growth to help recoup the lost export receipts, continue with undisrupted gains from trade and bring back on track the 'trade engine' to drive economic growth and development in many low-income and vulnerable developing countries. However, in the backdrop of ensuing trade tensions between the USA and its major trade partners, the prospect of an improved trade and investment momentum appears to be quite bleak. The growth of trade in 2018 is reported to have moderated and is projected to slow down in 2019-20 as global investment decelerates. The implications of USA-China trade war have been the subject of intense policy discussions with recent estimates showing the cost of heightened protectionism could result in forgone trade of more than $600 billion.

After three decades of rapid expansion under an increasingly liberalised global environment, international trade and cross-border capital flows have experienced a prolonged period of deceleration. Globalisation and free trade policy regimes are at a crossroads as countries aim to alter their comparative advantages and fail to appreciate the overall gains from trade because of populist policy stances. Triggered initially by the global financial crisis of 2008, this dismal state of affairs intensifies as the benefits of globalisation have been called into question, causing political upheavals in Europe and the USA. In particular, the trade policy reversals under President Trump threaten the world economy with a protectionist agenda that has widespread global ramifications. The globalisation backlash and associated policy reversals have shone a new spotlight on the role of trade in development. Over the past two decades, international trade as a driver of economic growth became established not only in the economics literature but also in the development strategies of many developing countries. The United Nations-led global development initiative Transforming Our World: The 2030 Agenda for Sustainable Development recognises international trade as a means for achieving various Sustainable Development Goals (SDGs). Therefore, one question is how the unfolding developments on the international trade front are going to affect the poorest, smallest and most vulnerable developing countries.

-fi.jpg) RECENT TRENDS: As mentioned above, world exports of merchandise goods and services exhibited a strong recovery in 2017, reaching US$22.7 trillion and registering a rise of more than 10 per cent over the previous year (Figure-1). Despite this improved performance, world exports remained below the level of 2012. When measured in real terms, world trade growth in 2017 was 5.0 per cent, the highest since 2012, and significantly higher than the 3.0 per cent annual average growth rate achieved during 2012-16. Nevertheless, the reinvigorated trade growth of 2017 remained lower than that of the pre-global financial crisis long-term (1980-2007) average growth of 6.1 per cent. In fact, global trade did not for a single year since 2012 grow faster than the average growth of 1980-2007. If International Monetary Fund (IMF) projections (IMF 2018) turn out to be correct, global trade expansion will see even slower momentum in the coming years. Therefore, 2012-2021 could be the slowest decade of trade expansion (3.8 per cent per annum) since World War II. The highest average rate of growth in world trade was registered in the decade of the 1990s at 6.6 per cent per annum. Despite the global financial crisis, the average rate of trade expansion in the 2000s was more than 5 per cent. Largely because of a sharp recovery in 2011 following the impact of the global financial crisis, the annual average trade growth during 2010-12 was very high. But since 2012 global trade slowdown has persisted. Although the global financial crisis-led trade collapse in 2009 was quite straightforward to explain, declining global trade in 2015 and 2016 was unprecedented in nature. After the global financial crisis, the world GDP (gross domestic product) growth rate was relatively quick to return to the long-term average rate. However, international trade flows were subject to further shocks. Measured in value terms (using US dollars), world merchandise exports fell by a staggering $2.7 trillion in 2015 (from the previous year) and then again declined by more than $500 billion in 2016. As many as 183 countries experienced reduced export earnings in 2015 (compared with the previous year) and for 112 countries export earnings similarly declined in 2016 (Commonwealth Secretariat 2016). Therefore, the robust global trade growth of 2017 was largely attributable to the fact that it was recovering from an already low base. It can be estimated from United Nations Conference on Trade and Development (UNCTAD) data that against the fall in global exports by more than $3.2 trillion (between 2014 and 2016), the recovery that took place in 2017 was of $2.1 trillion.

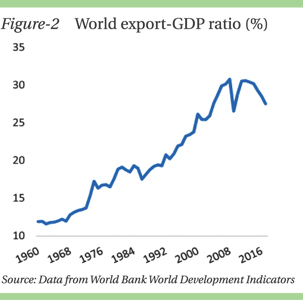

RECENT TRENDS: As mentioned above, world exports of merchandise goods and services exhibited a strong recovery in 2017, reaching US$22.7 trillion and registering a rise of more than 10 per cent over the previous year (Figure-1). Despite this improved performance, world exports remained below the level of 2012. When measured in real terms, world trade growth in 2017 was 5.0 per cent, the highest since 2012, and significantly higher than the 3.0 per cent annual average growth rate achieved during 2012-16. Nevertheless, the reinvigorated trade growth of 2017 remained lower than that of the pre-global financial crisis long-term (1980-2007) average growth of 6.1 per cent. In fact, global trade did not for a single year since 2012 grow faster than the average growth of 1980-2007. If International Monetary Fund (IMF) projections (IMF 2018) turn out to be correct, global trade expansion will see even slower momentum in the coming years. Therefore, 2012-2021 could be the slowest decade of trade expansion (3.8 per cent per annum) since World War II. The highest average rate of growth in world trade was registered in the decade of the 1990s at 6.6 per cent per annum. Despite the global financial crisis, the average rate of trade expansion in the 2000s was more than 5 per cent. Largely because of a sharp recovery in 2011 following the impact of the global financial crisis, the annual average trade growth during 2010-12 was very high. But since 2012 global trade slowdown has persisted. Although the global financial crisis-led trade collapse in 2009 was quite straightforward to explain, declining global trade in 2015 and 2016 was unprecedented in nature. After the global financial crisis, the world GDP (gross domestic product) growth rate was relatively quick to return to the long-term average rate. However, international trade flows were subject to further shocks. Measured in value terms (using US dollars), world merchandise exports fell by a staggering $2.7 trillion in 2015 (from the previous year) and then again declined by more than $500 billion in 2016. As many as 183 countries experienced reduced export earnings in 2015 (compared with the previous year) and for 112 countries export earnings similarly declined in 2016 (Commonwealth Secretariat 2016). Therefore, the robust global trade growth of 2017 was largely attributable to the fact that it was recovering from an already low base. It can be estimated from United Nations Conference on Trade and Development (UNCTAD) data that against the fall in global exports by more than $3.2 trillion (between 2014 and 2016), the recovery that took place in 2017 was of $2.1 trillion.  Therefore, global export of goods and services in 2017 was still more than $1.0 trillion less than that of 2014. The weak performance of trade has also been reflected in the global export and trade orientation. After a continuous rise over the past five decades, the ratio of world export to output has slowed down, and since 2008 has been falling (Figure 2). Following a sharp recovery in the period immediately after the global financial crisis, the world export-GDP ratio has been declining since 2012. The export share of the world GDP in 2017 was 27.5 per cent - more than two percentage points lower than in 2012 (Figure 2). In the immediate aftermath of the global financial crisis, major economies specially developed and large developing countries started to embark on protectionist measures, undertaking on average more than 800 protectionist interventions every year.

Therefore, global export of goods and services in 2017 was still more than $1.0 trillion less than that of 2014. The weak performance of trade has also been reflected in the global export and trade orientation. After a continuous rise over the past five decades, the ratio of world export to output has slowed down, and since 2008 has been falling (Figure 2). Following a sharp recovery in the period immediately after the global financial crisis, the world export-GDP ratio has been declining since 2012. The export share of the world GDP in 2017 was 27.5 per cent - more than two percentage points lower than in 2012 (Figure 2). In the immediate aftermath of the global financial crisis, major economies specially developed and large developing countries started to embark on protectionist measures, undertaking on average more than 800 protectionist interventions every year.

One of the most prominent features of the 1990s' and early 2000s' global trade was the expansion of global value chains in which production processes fragmented, with each country concentrating only on certain specific tasks rather than producing the whole product and providing the associated services. Combined with open trade policies, the global value chain led to the relocation of an increasing share of domestic production abroad. However, during the post-financial crisis period, because of the slowing down of the global value chain, major economies such as the USA and China started sourcing intermediate inputs more often from their respective domestic economies.

LDCS, SMALL STATES AND SUB-SAHARAN AFRICA: A decade of lost gains from trade since 1980, world exports have grown by more than 10 times (to about US$23 trillion in 2017). During the same period, developed and developing countries' total exports expanded by about 8 and 14 times respectively. Increasing global integration and a rapid rise in trade flows resulted from the widespread trade liberalisation of the 1980s and 1990s. From the late 1990s to 2012, the economic groups of the LDCs and sub-Saharan Africa (SSA) managed to reverse the trend of their marginalisation in global trade with their share in total global exports of goods and services increasing quite noticeably. Interestingly, the global financial crisis of 2008 did not cause sustained declines in the relative significance of these groups of countries. However, they were affected by the trade slowdown of 2015-16 as their share in world exports fell. Indeed, it seems that the most recent trade crisis has reinforced the marginalisation of the poorest, smallest and most vulnerable economies of the world.

A strong recovery in 2017 led SSA's exports to rise by US$50 billion over the previous year to reach $373 billion. The comparable increases for LDCs and small states were $25 billion and $1.0 billion respectively. But still, these country groups' total exports in 2017 were just about at the same level as in 2008. During 2000-08, LDC exports grew nearly five-fold, from $43 billion to about $200 billion, which is just about the same size as in 2017. For the group of African, Caribbean and Pacific (ACP) countries, including SSA and small states, their combined exports of goods and services during 2000-08 rose by more than three times, from $146 billion to $482 billion as against their corresponding exports of $448 billion in 2017. From this perspective, the period 2008-2017 can be seen as a lost decade of gains from trade for the world's poorest, smallest and most vulnerable countries. The global trade crisis was to deal an early blow to one SDG target as stated under SDG 17.11. Having adapted from the other United Nations (UN)-led initiative - the Istanbul Programme of Action (IPOA) for LDCs for the Decade 2011-2020 - this target stipulated a doubling of the LDC share of global exports by 2020. At the start of IPOA implementation, the corresponding LDC share was 1.05 per cent and thus fulfilling this SDG target would require LDC share to rise to 2.1 per cent. However, the share has actually declined to 0.92 per cent in 2017. Therefore, achieving the target of doubling LDC share now appears to be an almost impossible task given current trends in global trade.

As Western developed countries recovered from their prolonged recession following the 2008 financial crisis, their average output growth during 2013-17 of 1.88 per cent per annum was comparable with that of 2.17 per cent during 2000-08. In contrast, the output growth for LDCs in the most recent period (2013-17) was recorded at 4.7 per cent, which is much lower than the 6.6 per cent achieved during 2000-08. For SSA, the comparable figures are 3.18 per cent during 2013-17 and 5.73 per cent during 2000-08. Small states have experienced the most remarkable decline in their average GDP growth rate: from 4.68 per cent in 2000-08 to 1.72 per cent in 2013-17. Turning to exports, global trade slowdown affected the overall world economy and developing and developed country groups, but the impact has been most severe for LDCs, SSA and small states. Small states and SSA saw their exports during 2013-17 on average decline by close to 6.0 per cent and more than 4.0 per cent respectively. The corresponding decline in LDCs' exports was 0.6 per cent. Small states are more dependent on international trade for their economic activities. Therefore, it is their dismal export performance that contributed to weaker GDP growth. During 2012-17, out of 45 Commonwealth LDCs, SSA and small states, as many as 28 had experienced a lower rate of economic growth than the pre-financial crisis years of 2000-08. As many as 23 countries (i.e. more than 50 per cent) registered lower average annual economic growth rates in 2013-17 than in 2009-2012. For 16 countries, economic growth seems not have been affected by the global financial crisis, as their annual average GDP growth during the post-financial crisis years 2009-2012 remained almost the same as or higher than that of the pre-financial crisis years of 2000-2008. Out of these countries, five Commonwealth countries - Brunei, Gambia, Fiji, Bangladesh and Tanzania - experienced an annual average GDP growth rate that was almost the same as it was during the pre-financial crisis period and recovery years of 2000-2012. However, Brunei's economic growth was severely affected by the global trade slowdown during 2013-17, whereas Fiji, Bangladesh and Tanzania's economic expansion continued. Ghana, Lesotho, Solomon Islands, Swaziland and Zambia are the five countries that experienced higher average annual GDP growth during 2009-2012 than during 2000-08. However, their average growth during 2013-17 declined to lower than the pre-crisis 2000-08 average rate of economic growth. Considering international trade performance, 36 Commonwealth LDCs, small states and SSA economies (out of a total of 45; more than 80 per cent) suffered lower export growth during 2013-17 than during the pre-crisis period (2000-08), as Figure 10 shows. For nine countries, export growth was not affected by the global financial crisis. Of these countries, other than Dominica and Tonga, all others - namely Bangladesh, Botswana, Ghana, Guyana, Malawi, Seychelles and Solomon Islands - experienced lower average annual export growth during the global trade slowdown period of 2013-17 than during both the pre-financial crisis years 2000-08 and the immediate post-financial crisis period 2009-2012. Of the 12 Commonwealth LDCs, Rwanda managed to achieve a relatively high (13.5 per cent) average annual export growth rate during 2013-17, while Kiribati and Zambia posted negative growth rates. Out of the 10 most adversely affected Commonwealth countries from the global trade slowdown period 2013-17, six were from SSA. The largest two SSA economies, Nigeria and South Africa, which account for almost half of SSA exports, experienced negative trade growth.

Dr Mohammad A Razzaque, is Senior Fellow for International Trade and Globalisation at Bloomsbury Institute London, UK, and Director, Policy Research Institute of Bangladesh (PRI).

Dr Syed Mortuza Ehsan is Assistant Professor, Department of Economics, North South University, Dhaka

Excerpted and slightly abridged from The Commonwealth International Trade Working Paper titled ''Global Trade Turmoil: Implications for LDCs, Small States and Sub-Saharan Africa' written by the authors.

© 2026 - All Rights with The Financial Express