A bank staffer checking notes at a counter of her commercial bank in Dhaka — FE photo

A bank staffer checking notes at a counter of her commercial bank in Dhaka — FE photo ![]() At present, development policies pays increasing attention to the importance of the financial sector in economic and social development and to creating economically sound and stable financial institutions, especially in the middle income countries (MICs) such as Bangladesh. A developed financial system mobilises productive savings, allocates resources efficiently, improves risk management, and reduces information asymmetry, all of which facilitate innovation and entrepreneurship.

At present, development policies pays increasing attention to the importance of the financial sector in economic and social development and to creating economically sound and stable financial institutions, especially in the middle income countries (MICs) such as Bangladesh. A developed financial system mobilises productive savings, allocates resources efficiently, improves risk management, and reduces information asymmetry, all of which facilitate innovation and entrepreneurship.

The financial sector of Bangladesh is still underdeveloped. The hypothesis is strong in Bangladesh that the underdevelopment of the financial sector is due to the fact that the financial institutions are unable and/or unwilling to overcome the incentive-related problems associated with financing and there exist poor risk diversification, inadequate loan evaluation, and corruption and fraud. A key element in any strategy for development for the middle income Bangladesh therefore is to extend the 'frontier of finance'.

The major institutional challenges for financial sector management emerge from striking the right balance to achieve the triple aims of financial stability, growth, and equity. These relate to the links between the financial sector and inclusive and sustainable development. This may include issues such as the desirable size and structure of the financial sector and regulatory challenges to maximise the likelihood of achieving financial stability, while safeguarding inclusive and more sustainable growth.

Finance-led Growth and Growth-led Finance: Theoretical underpinnings of the link between financial development and growth stem from the insights of endogenous growth models. The finance-led growth hypothesis is based on the notion that finance causes economic development through the transfer of scarce resources from savers to investors. The supply-leading finance transfers resources from traditional sectors to modern high-growth sectors and stimulates entrepreneurial response in the modern productive sectors. The hypothesis assumes a causal relationship from financial sector development to economic growth, meaning that the establishment of financial institutions and markets increases the supply of financial services leading to economic growth.

The growth-led finance (demand-following), on the other hand, stipulates that economic growth creates demand for financial instruments and enterprises lead and finance follows, so the relationship starts from growth to finance, hence the demand following hypothesis. The theory points out that financial development and innovative products are engineered in a passive response to the demand of a growing economy. As the economy grows, demand for financial services grows and the demand forces the financial system to respond by providing new products and services, specifically meant for new needs. The feedback hypothesis is based on the view that there is a bi-directional causal relationship between financial growth and economic performance.

In practice, both hypotheses may work in Bangladesh. Over the years, Bangladesh's financial system, particularly banking and microfinance, has grown and developed. The banks' total assets and private credit ratios to GDP have increased; and bank deposits, as a percentage of GDP, are comparable to other South Asian countries. Private domestic banks now hold a majority of bank assets; the shares of state-owned commercial banks (SCBs) and specialised banks (SBs) have declined correspondingly. Bank branches, access to banking, and microfinance services have expanded substantially.

Non-banking financial institutions have also grown but remain small; banks still account for over 90 per cent of financial institutions' assets. Equity market listings and capitalisation have grown substantially; market capitalisation in recent years is around 15 per cent of GDP. A government bond market is developing.

Further sound financial development in the various parts of the financial sector, and increased access, will lead to further improvement in fundamentals: better credit information and improved legal and judicial enforcement of creditors' rights and collateral execution.

.jpg)

Bangladesh Bank headquarters in Dhaka — FE photo

Price Stability: Although maintaining price stability is a predominant objective of Bangladesh's macroeconomic policy, Bangladesh refrains from the conservative stance of 'inflation targeting', which has been widely adopted in many countries. The Monetary Policy Statement (MPS) of the Bangladesh Bank usually aligns with the overall macroeconomic objectives of the economy, and adopts 'monetary policy stance and monetary program…. with dual objective of maintaining price stability and supporting inclusive, equitable and environmentally sustainable job rich economic growth in tune with the government's strategies and goals for sustainable growth and development' (Bangladesh Bank, Monetary Policy Statement, Fiscal Year 2019-20: 10).

For an upper middle income Bangladesh, the price stability challenge is complex and requires a careful review of what should be realistic short-run inflation, how low it should be, and how it is calibrated through potential inflation-growth trade-off. It is also important to trace the multiple causes of inflation, and the policy instruments that are traditionally applied to contain inflation. There are only few empirical studies on inflation-growth trade-offs in Bangladesh and monitoring of such trade-offs.

In Bangladesh, available evidence shows that the volatility in inflation comes from factors affecting both non-food inflation and food inflation. There are various factors behind food price fluctuations e.g. supply disruptions due to floods and other natural disasters, price distortions by market intermediaries, and rise in food import prices, among others. Clearly, controlling inflation in Bangladesh requires other interventions to complement the monetary instruments. Long-term public investments and other measures would be needed to address structural factors and food price volatility. It may be noted that, over the last two decades, the rate of inflation in Bangladesh has fluctuated, and the level of fluctuation was much higher in the 1990s than in the 2000s. Thus, volatility of inflation has not been a major concern during the past two decades in Bangladesh.

Furthermore, monetary policy seems to have limited power to control inflation in Bangladesh. The instruments at the disposal of Bangladesh Bank are often not effective to respond to inflationary tendencies. The Bank rate (the policy rate) has been held constant almost since FY2003-04 (Bangladesh Bank uses the repo rate as a proxy policy rate); instead, it addresses price stability largely through the credit/deposit channel, often by maintaining a closely monitored relationship between broad money (M2) and reserve money (RM). The use of control over money aggregates (credit channel) provides a pseudo control over the credit flow to the private sector. The credit channel, however, has its limitations, and may miss the inflation target. On the other hand, the policy rate channel cannot be made effective since the 'transmission mechanisms' are very weak, and financial infrastructure is underdeveloped.

For an upper middle income Bangladesh, reforms for greater market competition in the financial sector will have to be broadened and deepened. This will place increasing responsibility on the Bangladesh Bank's 'policy rate', the effectiveness of which will depend on, among others, greater financial deepening, strengthening of credit and debit markets and interbank transactions and integration-all within an efficient regulatory and accountability framework.

A major concern is to increase the efficiency of the existing monetary and financial system, along with its ability to control inflation and exchange rate stability in the near future, when the economy will be poised towards a higher growth pathway which may require greater external interaction. There are other potential threats to price stability that can trigger inflation uncertainties, such as fiscal dominance. Bangladesh's projected growth for transition to upper middle income status would require much higher public expenditure to meet infrastructural and social needs. Increased borrowing, especially from the banking sector, in case there is a revenue shortfall, will then likely cause price instability.

Another potential source is the exchange rate volatility. Although in principle, Bangladesh maintains a market-based, free-floating exchange rate regime, Bangladesh Bank periodically intervenes to buy/sell foreign currency to reduce volatility and support international competitiveness of Bangladesh's exports. In the growing Bangladesh economy, growth of export capacity to meet future import surge and sustained growth in remittance flows are important determinants of external stability.

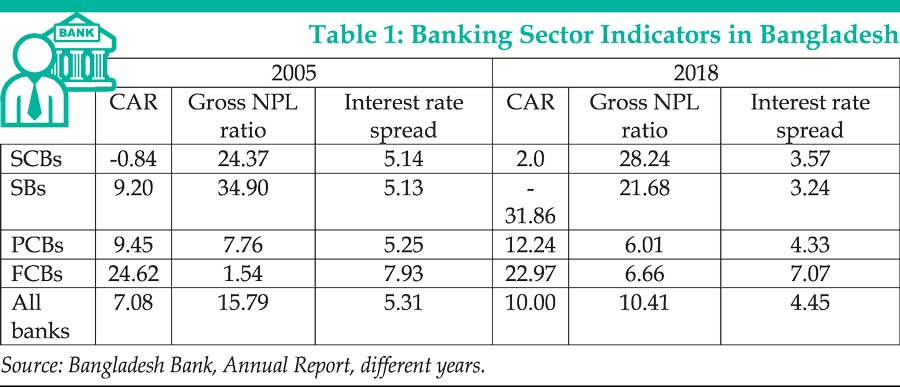

In short, the working of the monetary policy at present remains constrained by serious shortcomings of several factors as reflected in the persistently unacceptable level of non-performing loans (NPLs) and capital adequacy ratios (CARs), high interest rate spreads, and the huge proportion of classified loans, especially in the SCBs.

The Banking System: In the post-reform period, the structure of the banking system has changed significantly. As part of the reform programme, some SCBs were privatised, foreign ownership of banks was opened up, and additional new commercial banks were allowed to start and operate in the private sector. At present, six SCBs, two specialised banks (SBs), 40 private commercial banks (PCBs), and nine foreign commercial banks (FCBs) operate in the country. Besides, the Investment Corporation of Bangladesh (ICB) also plays a vital role as an investment bank.

Despite the reforms and expansion of different types of institutions, a strong, competitive and efficient banking system has not as yet emerged. The banking system is mired in corruption, mismanagement, and direct interference from the government. The banks do not follow the practice of determining the interest rate under competitive conditions. Both lending and deposit rates are set under oligopolistic conditions, possibly following collusive or cartel type behaviours.

It may be noted that the banking sector is still the dominant financial intermediary in Bangladesh's financial system due to the underdeveloped money and capital markets, limited availability of financial instruments, and lack of confidence in the financial system as a whole. Bangladesh Bank faces significant limitations in following an independent monetary policy consistent with its objectives. The government still plays an important role in the financial sector as a major borrower from the banking system.

There is very limited scope for individuals to invest in the capital market and the lack of alternative opportunities for investment compel many to invest mainly in bank deposits, post office saving certificates and government savings bonds. Banks operate with old and outdated banking procedures, lack of coordination between proper manpower planning and bank schemes, lack of market research for customer analysis, scarcity of financial derivatives, inefficient banking services, and lack of long term planning creates bottlenecks preventing banks from adopting modern banking practices.

Further, overall stability and performance of the banking sector is not satisfactory due to high NPLs, lack of good governance, and other factors. As Table 1 shows, there exists a huge variation in CARs and the NPLs amongst various groups of commercial banks. The better performance in these indicators by the foreign banks allows them to maintain a higher interest rate spread. The interest rate spread is still high, and is often attributed to loan defaults (and scams), but also to alleged 'collusive, oligopolistic fixing' of lending rates. Some of these factors are linked to political and vested interest groups. There also persist serious governance deficits, which constrain any move to bring the financial institutions towards the best-practice standards. The current turmoil in the banking and financial sector could increase rapid exposures to investment risks.

Further, proper assessment of risks and costs of alternative sources of funds is often acute in decision making by financial administrators. Lack of ethics in the banking sector is a part of a wider and persistent socioeconomic and political culture in the country. Unhealthy competition among different banks displays lack of ethics in doing banking business.

Further, proper assessment of risks and costs of alternative sources of funds is often acute in decision making by financial administrators. Lack of ethics in the banking sector is a part of a wider and persistent socioeconomic and political culture in the country. Unhealthy competition among different banks displays lack of ethics in doing banking business.

In Bangladesh, where financial inclusion has taken the centre stage, the role of banks cannot be over-emphasised. The question remains whether the collective efforts around banking sector development translate to economic growth. A developed banking sector plays a pivotal role in ensuring access to basic financial services such as savings, payments and credit which contribute positively towards improving poor people's lives.

A strong and stable banking system is the backbone of an effective economy. While the financial sector is comprised of the financial markets, financial institutions, banks, bond markets, insurance sector, securities sector, stock exchanges and microfinance sector all of which play a secondary role in providing access to finance, they do not optimally contribute to the resource mobilisation for economic development. Many countries largely rely on the banking sector which serves as a bridge between savers and borrowers among other functions.

A strong and stable banking system is the backbone of an effective economy. While the financial sector is comprised of the financial markets, financial institutions, banks, bond markets, insurance sector, securities sector, stock exchanges and microfinance sector all of which play a secondary role in providing access to finance, they do not optimally contribute to the resource mobilisation for economic development. Many countries largely rely on the banking sector which serves as a bridge between savers and borrowers among other functions.

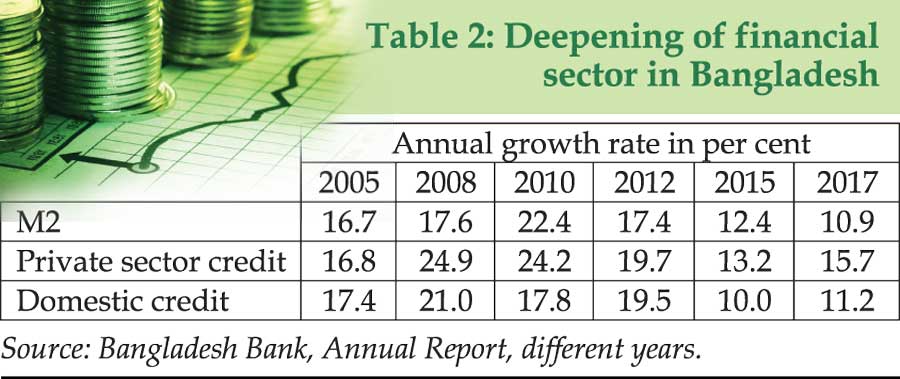

A strong financial system and an appropriate financial infrastructure are essential to sustain price stability, encourage savings and investment, and foster growth and employment generation. More specifically, the financial sector needs to cater to the needs of the country's growing economy, such as through mobilisation of savings and credit growth to the private sector. No doubt, Table 2 shows a growing trend of the key indicators of financial sector deepening in Bangladesh, but the pace has to be stepped up for financial resource mobilisation and credit utilisation by the private sector. Financial structure development also needs to be geared towards greater inclusion and participation through broadening the lending base, and diversification of credit allocation.

Further, the rapid introduction of digital technology in the banking system, such as mobile banking, e-banking, modernisation of payment systems, regulations, guidelines and supervision--are likely to bring about greater transparency and accountability, and a reduction in the costs of delivery of financial services. The challenge for the government would be to develop appropriate institutional and regulatory framework to provide new intermediation initiatives between bank profitability and financial inclusion within a broader monetary policy framework.

The Capital and Equity Market: For stimulating economic growth and development, Bangladesh requires long term funding, far longer than the duration for which most savers are willing to commit their funds. In this regard, the capital market provides an avenue for mobilisation and utilisation of long-term funds for development and hence it is referred to as the long term end of the financial system. An upsurge in capital market activity as a tool for fast-tracking economic progress is therefore extremely important for upper middle-income Bangladesh.

Bangladesh is still at a nascent stage of capital market development although a well-functioning capital market is of great significance for Bangladesh for channeling domestic savings to productive investments, attracting foreign investors to the market, and allocating the national savings most efficiently, among others. However, the Bangladesh equity market is small, it is thin and non-transparent, and it is inefficient as well.

One should, however, be aware that the capital market may face serious challenges in countries like Bangladesh and may not perform efficiently since capital market development requires huge costs and strong financial structures. These problems are magnified by weak regulatory institutions and macroeconomic volatility. High price volatility in stock markets reduces the efficiency of the price signals in allocating investment resources.

According to orthodox theory, a stock market can contribute to development through a variety of channels: it could raise savings and investment by making it possible for individuals and households to purchase a fraction of an enterprise, thereby spreading the risk, without which investment may not occur. Similarly, the monitoring function is performed automatically by the stock market and, from the perspective of an entrepreneur, this helps raise investment. A well-functioning stock market allocates resources more efficiently through its normal pricing process, which would accord, other things being equal, higher share prices to efficient firms and lower prices to inefficient ones.

Further, the take-over mechanism ensures that not just the new investment resources but also the existing capital stock is efficiently utilised. Inefficient use of existing resources is penalised by the market for corporate control through disciplinary takeovers. In practice, how effectively the stock market can perform the above tasks depends on the efficiency of two critical market mechanisms, namely (i) the pricing mechanism; and (ii) the take-over mechanism.

In the case of share prices, it is suggested that, in the face of highly uncertain future, share prices are likely to be influenced by the so-called 'noise traders', and by whims, fads and contagion. In developing countries, apart from the normal mis-pricing, which is particularly likely to be severe as the firms are not likely to have a long track record, share prices are more volatile than in advanced countries. Share price volatility is a negative feature of stock markets for several reasons. First, it reduces the efficiency of the price signals in allocating investment resources. Secondly, it increases the riskiness of investments and may discourage risk-averse enterprises from financing their growth by equity issues, and indeed from seeking a stock market listing at all. Thirdly, at the macroeconomic level, a highly volatile stock market may lead to financial fragility for the whole economy.

Bangladesh's stock markets are characterised by large volatility with recurrent periods of boom and bust that represent a destabilising force for the economy. For example, following a bull run during 2010, the Dhaka index fell by about a half from its December 2010 all-time high, corresponding to a loss of about 22 per cent of GDP by October 2012. The market correction wiped out $27 billion in market capitalisation and, with it, bankruptcies, savings, and jobs, triggering a wave of social discontent. The ensuing liquidity crunch led to heightened solvency risks. Given the interconnectedness between banks and equity markets, such incidents can result in a negative feedback loop from the financial sector to the real economy.

.jpg)

Motijheel-Dilkusha area is the country's main financial centre — FE photo

The market for corporate control is often considered as the evolutionary endpoint of stock market development. An active market for corporate control presents a credible threat that inefficient managers will be replaced to maximise shareholder value and thereby raise corporate performance. This consideration is particularly important for developing countries like Bangladesh where there are large, potentially predatory, conglomerate groups. These could take over smaller, more efficient firms and thereby reduce potential competition to the detriment of the real economy.

At present, Bangladesh like most other developing countries does not have a well-functioning stock market. Not only is there inadequate government regulation, efficient private information gathering and disseminating firms are also absent. The markets suffer from significant regulatory and informational deficits: the markets remain 'immature' (i.e., riddled with insider trading and lack of transparency) and relatively illiquid. Most trading takes place in a few blue-chip shares. The regulator also finds it difficult to regulate the stock markets, as is indicated by frequent scams in the stock market.

Therefore, along with developing the banking sector, Bangladesh needs to take appropriate measures and regulations to ensure that the stock markets do not become a source of instability or short-termism in the economy. For this reason, Bangladesh also needs to discourage the emergence of a market for corporate control. Bangladesh should find other institutional ways of replacing inefficient managements which are reliable and cheap compared with the takeover device on the stock markets.

For the middle income Bangladesh, regulation of the financial sector needs to be counter-cyclical--to prevent boom-bust cycles which can lead to developmentally costly crises--and comprehensive, to include all institutions that provide credit. Capital flows should also be prudently managed, and where appropriate, capital account regulations should complement domestic financial regulation. Furthermore, borrowing on the international bond markets could lead to future problems; and needs careful monitoring.

The fact that Bangladesh's financial system is still relatively small in relation to the size of its economy allows more space for the policy-makers and regulators to try to shape the financial systems to serve well the needs of inclusive and sustainable growth (e.g. much needed lending to MSMEs), as well as desirable structural change. Furthermore, since the financial sector is smaller as proportion of GDP, it may imply it is less powerful politically; thus, potentially this gives more autonomy to the regulators to shape the financial sector to serve the real economy.

However, a key issue is not just the size, but also the structure of the financial sector. Because the financial sector is riddled with market imperfections and market gaps, it is important to have government intervention to correct these market imperfections (e.g. the pro-cyclical nature of private lending) and institutional arrangements to fill market gaps (e.g. sufficient long-term finance for helping finance private sector investment). In addition, it is useful for the government to have institutions and mechanisms to help finance development of particular sectors to implement the adopted vision and the strategy of development.

In this context, it is important to design instruments and institutions that can perform such functions. Public development banks have worked well in several countries (e.g. Japan, South Korea, and others) with appropriate regulations. Often it is argued that smaller, more decentralised banks may be more appropriate in developing countries, especially to lend to MSMEs, partly because they know their customers better, reducing both asymmetries of information and transaction and default costs.

Overall, a more diversified banking system, with large and small banks, as well as private and public development banks seems to offer benefits of diversification; and thus less systemic risk, complementarities in serving different sectors and functions, as well as providing competition for providing cheaper and appropriate financial services to the real economy.

It is well known that a growing economy in need of new forms of financial intermediation to finance investments that are either too long-term or too risky for commercial banks is one of the most important drivers of capital market growth.

The development of local capital market can increase access to local currency financing and thereby help manage foreign exchange risk and inflation better. For investors and savers, capital market offers more attractive investing opportunities--with better returns--than bank deposits, depending on risk profile, liquidity needs, and other factors. Further, with a wider range of securities and instruments offered, capital market can help investors diversify their portfolios and manage risk.

Through the use of derivatives, well-developed capital market provides risk management tools not only to the market participants, but also to end users. Well-developed capital markets also provide benefits at the macroeconomic level by supporting monetary policy transmission, which is facilitated through liquid securities market. Further, they can serve as a 'spare tire' for the financial sector, enhancing financial stability and reducing vulnerabilities to exchange rate shocks and sudden interruptions of capital flows.

An essential condition for a well-functioning financial system--with both banks and capital markets--is the existence of sound macroeconomic and relevant policy frameworks. The institutional framework is also critical, as markets depend on investor confidence and strong institutions provide the basis for investor and creditor protection.

However, capital markets are not without risks. In a country like Bangladesh, these may include the potential for asymmetric information between savers and users; non-transparency and lack of adequate regulation and monitoring of issuers; lack of adequate and efficient market infrastructure for issuing, trading, clearing and settlement; and the potential for increased volatility due to liquidity, interest rate and rollover risks. To reliably extract the benefits of well-functioning markets, adequate regulation for issuers, investors, and intermediaries in addition to robust supervisory arrangements to protect investors, promote deep and liquid markets, and manage systemic risk are critical. Such a framework in turn needs to be anchored in a good investment climate that includes a sound taxation and accounting framework, reliable and quality accountancy, creditor rights, property rights, and bankruptcy and competition law.

Finally, markets need an infrastructure--exchanges and trading platforms, clearing houses, and custodians. Typically, capital market offerings of debt securities start with the highest credit quality issuer which is typically the government, and government bond markets--beginning with short term money market instruments and extending to longer tenor bonds--form a basis for further market development by establishing price points along a yield curve and providing instruments for liquidity management. They also provide a critical mass of securities to support market infrastructure development.

Banks are often the next issuers able to come to the market. While banks may benefit from including capital market instruments in the funding mix to better match liabilities to assets, they tend to have a ready source of liquidity from deposits available to service their obligations. Utilities, which typically have long-term capital investment needs but steady and predictable cash flows, may follow and then other corporates.

In parallel, it is critical that efforts be focused on developing the investor base. The most reliable and stable investor base is local. Nurturing domestic investible asset pools via pensions, insurance, and savings vehicles for individuals to deploy into the capital market is critical for local sustainable capital market development. Pension reform, development of the local insurance industry, and an increase in household savings are often part of a comprehensive capital market development programme.

Experience shows that the development of the local capital market and making greater use of it to fund private investment and strategic economic needs tends to happens in stages in a developing country like Bangladesh. Therefore, some sequencing of policies is essential. This is particularly true for debt markets, which require well-functioning money markets to create government bond markets, and they in turn are essential for corporate bond markets. Understanding the linkages between different segments of the market and their building blocks is critical to ensuring a proper sequencing of policy and regulatory reforms. Capital market development is a gradual process requiring strong leadership from the government as well as a significant commitment of time and resources. If done correctly, the payoffs can be substantial and long-term. The strategic imperative, however, is to develop strategies that fit the particular circumstances of Bangladesh.

Concluding Remarks: Both theoretical reasoning and empirical evidence suggest that a well-developed financial system plays a positive growth-inducing role in development. For transiting towards an upper middle-income Bangladesh, a developmental approach to financial sector growth is necessary, while at the same time attending to prudent regulations. The country's progressive financial system must ensure a sound financial structure with varieties of financial products and services, including electronic trading system to trade derivatives in stock exchanges, a carefully outlined series of regulations that govern the market judiciously and allows market participants to contain systemic risks.

The development of the country's capital and equity markets will occur only as a part of a comprehensive endeavour that addresses all the factors that affect the profitability and attractiveness of private enterprises. The challenge is to ensure a delicate balance between a system that assures adequate protection of the investors and one that does not deter market growth.

However, for a successful journey, Bangladesh should not wait for the market to bring development. For example, since market outcomes of human capital are likely to be sub-optimal; a strong justification exists for state intervention. The need is to have 'smart' interventions. Instead of the top-down approach, the 'developmental state' approach is needed which uses 'market-following' policies, such as supporting the availability of skilled labour to attract enterprises towards greater productivity and value addition.

Bangladesh, having successfully completed the journey from low income to lower MIC, now faces the more perilous journey to upper middle income status and then to a high income country. While the first leg of the journey provides grounds for optimism, Bangladesh must become more innovative and productive in order to successfully complete the second and the third stages, a journey in which the financial sector needs to play a more supportive role to bring higher levels of prosperity.

...................................................

Dr Mustafa K. Mujeri is Executive Director, Institute for Inclusive Finance and Development.

mujeri48@gmail.com

© 2026 - All Rights with The Financial Express