![]() Openness of an economy is measured by the sum of import and export expressed as a percentage of gross domestic product (GDP). In 1980-81, Bangladesh's openness stood at around 21.0 per cent, but rose steadily, and in 2018-19 the proportion was around 38.9 per cent.

Openness of an economy is measured by the sum of import and export expressed as a percentage of gross domestic product (GDP). In 1980-81, Bangladesh's openness stood at around 21.0 per cent, but rose steadily, and in 2018-19 the proportion was around 38.9 per cent.

Openness can be taken as a measure of efficiency of the economy. Since imports are usually procured from the least cost source, higher import of inputs and capital machinery contributes towards greater production efficiency in the economy. By the same reasoning, higher imports of finished goods mean greater level of consumer welfare.

Exports, on the other hand, are the evidence of competitiveness of the economy. Higher levels of export indicate success of the economy in outcompeting other producers in the international market. As Table 1 shows, Bangladesh's export grew at an average annual compound rate of 11.23 per cent during past 38 years 1980-81 to 2018-19.

In a developing country like Bangladesh, trade balance (export-import) is usually negative as our import need exceeds our export capacity. In national income accounting, trade balance is also interpreted as the resource balance and shows the gap between domestic savings and investment. Negative resource balance means that our investment needs are greater than our domestic savings capacity.

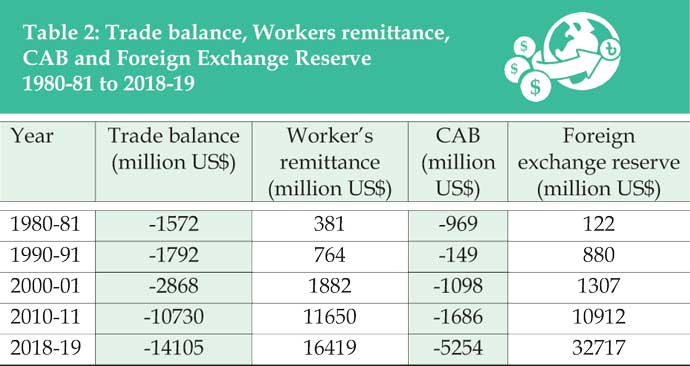

Current account balance (CAB) is defined as the sum of trade balance and net remittance, where net remittance consists of net factor income (primary) and net factor income (secondary), the latter consisting mainly of net worker's remittance. In Bangladesh, net factor income (primary) involving external inflow and outflow of rent, interest, profit income etc. is almost always negative.

Current account balance (CAB) is defined as the sum of trade balance and net remittance, where net remittance consists of net factor income (primary) and net factor income (secondary), the latter consisting mainly of net worker's remittance. In Bangladesh, net factor income (primary) involving external inflow and outflow of rent, interest, profit income etc. is almost always negative.

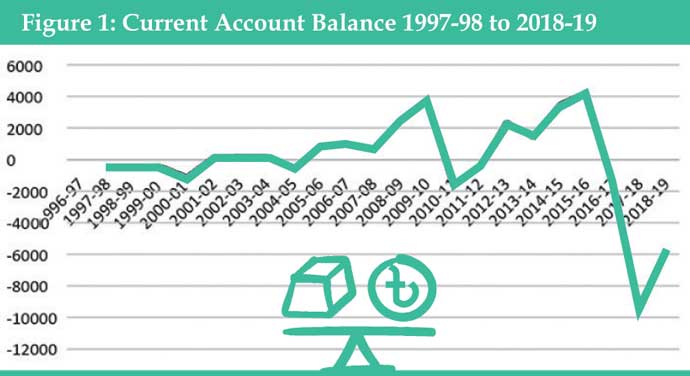

In contrast, worker's  remittance, as shown in Table 2, has been steadily growing which contributed towards bridging the gap between import and export. Inflow of workers' remittance grew at an annual compound rate of 10.4 per cent from a paltry $381 million in 1980-81 to $16,419 in 2018-19. Despite this impressive growth in workers' remittance, Current account balance (CAB) in Bangladesh, as evident from Fig 1, shows a mixed picture of both surplus

remittance, as shown in Table 2, has been steadily growing which contributed towards bridging the gap between import and export. Inflow of workers' remittance grew at an annual compound rate of 10.4 per cent from a paltry $381 million in 1980-81 to $16,419 in 2018-19. Despite this impressive growth in workers' remittance, Current account balance (CAB) in Bangladesh, as evident from Fig 1, shows a mixed picture of both surplus  and deficit. CAB was negative in 10 of the last 22 years (1997-98 to 2018-19), while it was positive in the other 12 years.

and deficit. CAB was negative in 10 of the last 22 years (1997-98 to 2018-19), while it was positive in the other 12 years.

A negative CAB implies that national saving is not big enough to finance our investment. The implication for the external sector is that current account outflow of foreign currency exceeds inflow of the same. Financing of the excess outflow is made out of foreign exchange reserve. However, when CAB is negative, it may or may not result in decline in foreign exchange reserve as net inflow in capital account can more than offset current account deficit. In fact, on the last 10 occasions when CAB was negative, foreign exchange reserve actually went up in four instances. Even if foreign exchange reserve declines temporarily, it may not be a matter of great concern because foreign exchange reserves are built up to face this kind of eventuality. A persistent decline in reserve is of course worrisome, which does not seem to have been the case in Bangladesh.

Even when there is no decline in foreign exchange reserve, a worsening CAB may call for corrective policy measures if it is due to one or more of the following three reasons - (i) slowdown in remittance inflow, (ii) slowdown in export earnings, and (iii) increase in non-essential imports such as luxury items or substitute foreign goods displacing quality domestic products.

Even when there is no decline in foreign exchange reserve, a worsening CAB may call for corrective policy measures if it is due to one or more of the following three reasons - (i) slowdown in remittance inflow, (ii) slowdown in export earnings, and (iii) increase in non-essential imports such as luxury items or substitute foreign goods displacing quality domestic products.

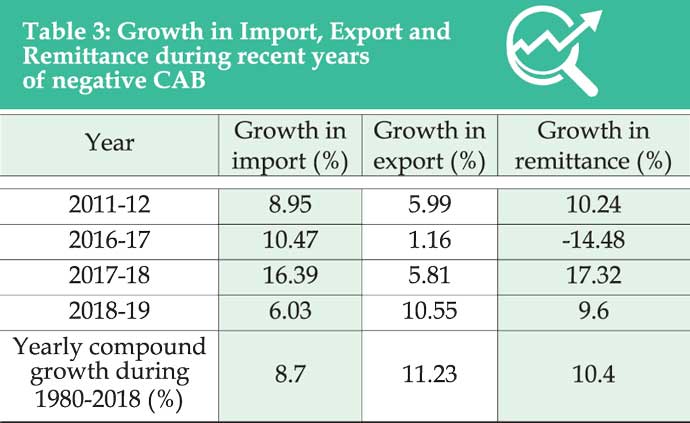

In Table 3, we have tried  to examine the proximate cause of negative CAB during the last four occasions. As can be seen from the Table, the main factor contributing to negative CAB in 2011-12 was sluggish growth in export while both import and remittance growth were close to their long-term yearly average.

to examine the proximate cause of negative CAB during the last four occasions. As can be seen from the Table, the main factor contributing to negative CAB in 2011-12 was sluggish growth in export while both import and remittance growth were close to their long-term yearly average.

In 2016-17, export was almost stagnant and for the first time in many years, remittance inflow declined in absolute terms. The year 2017-18 experienced very high growth in imports pulling down CAB in the negative range. Although import growth slowed down and both export and remittance posted respectable growth, the CAB continued to be negative albeit by a smaller amount in 2018-19 due to public investment related imports.

If increase in import is triggered by rising private/public consumption or displacement of local products by imports, it may call for corrective policy measures restricting non-essential imports and taking austerity measures. However, if increase in import relates to productive expenditure involving import of industrial raw material, intermediate and capital goods, we have a different story.

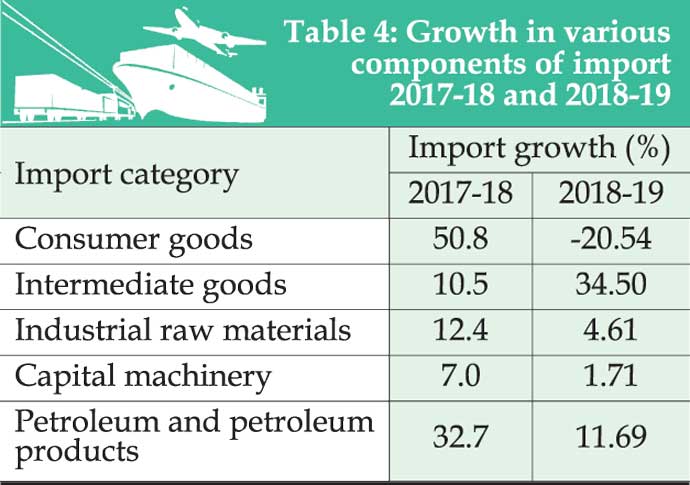

During 2017-18, import of consumer goods increased significantly due to rise in import of rice necessitated by flood damage of crop. This was a one shot increase in import and declined during 2018-19 (Table 4). Growth in import of intermediate goods has been persistent. These imports relate mainly to mega infrastructure projects of the government and are likely to level off in the coming days. Slowdown in the import of capital machinery and industrial raw material during 2018-19 may have been due to liquidity crisis in the banking sector leading to slower growth of credit to the private sector, and it may be a while before credit growth to the private sector picks up in full swing. Persistent growth in petroleum imports are due to rising international price and increased imports by private power plants. Given the above picture of import trend, barring unforeseen natural calamities or unusual rise in world commodity price, escalating imports destabilising balance of payments in Bangladesh seem unlikely in the near future.

During 2017-18, import of consumer goods increased significantly due to rise in import of rice necessitated by flood damage of crop. This was a one shot increase in import and declined during 2018-19 (Table 4). Growth in import of intermediate goods has been persistent. These imports relate mainly to mega infrastructure projects of the government and are likely to level off in the coming days. Slowdown in the import of capital machinery and industrial raw material during 2018-19 may have been due to liquidity crisis in the banking sector leading to slower growth of credit to the private sector, and it may be a while before credit growth to the private sector picks up in full swing. Persistent growth in petroleum imports are due to rising international price and increased imports by private power plants. Given the above picture of import trend, barring unforeseen natural calamities or unusual rise in world commodity price, escalating imports destabilising balance of payments in Bangladesh seem unlikely in the near future.

The negative growth in remittance inflow in 2016-17 was caused by several factors. At around that time, sluggish investment and import demand kept Taka temporarily appreciated while currency of most pertinent countries depreciated vis-à-vis US $. The hundi operators took advantage of this and made unauthorised use of mobile financial services such as bkash to divert remittance away from legal channel. Some Bangladeshi businessmen are also known to have mopped up remittance abroad offering higher exchange rates to finance their investment in foreign countries.

However, during 2017-18, import demand picked up and Taka depreciated. Also, at the instruction of Bangladesh Bank, bkash authority cancelled the license of 214 agents suspected of involvement in such hundi business. Consequently, 2017-18 saw 17.3 per cent growth in remittance inflow. In 2018-19, remittance growth declined slightly to 9.6 per cent. To gear up efforts towards attracting remittance inflow through official channel, the government declared 2 per cent cash incentives in the budget for FY20. Initial response seems quite positive and this policy support is expected to contribute significantly to shift in remittance inflow away from the hundi channel in the coming days.

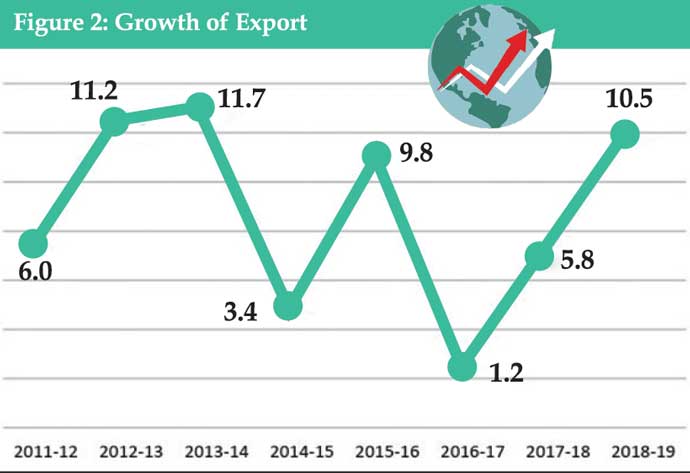

In contrast, Bangladesh's export sector seems to have been on a bumpy ride in recent years (Fig 2). Yearly export alternated between single—and double-digit growth varying from a low 1.2 per cent to a high 11.7 per cent during the last eight (08) years.

Constraints and challenges facing the export industries of Bangladesh can be grouped under two broad heads — (a) problems faced by specific industries, and (b) constraints that affect industries across the board.

The dominant export of Bangladesh, readymade garments (RMG), is currently beset with major structural malice. Following the Rana Plaza incidence, compliance requirement along with rising labour wage, has significantly raised their cost of production. This has induced RMG entrepreneurs to opt for labour saving technology. The resulting higher productivity and cost efficiency of units with improved technology have put those with traditional technology at a competitive disadvantage. Such expansion of capacities with new technology has thus created a certain amount of structural imbalance in the industry causing significant idle capacity to show up. The buyers are taking full advantage of the situation bargaining for low price and many RMG producers are succumbing to this pressure and accepting bare minimum price for the sake of survival.

The other major export industry "leather and leather products" is also passing through a crucial transitional phase following relocation from Hazaribagh tannery to Savar. The scandal surrounding setting up of the CETP in Savar seriously compromised the realisation of the export potential of this industry. The industry is now eagerly waiting for Leather Working Group certification once the CETP finally gets installed.

Frozen food, another important export industry of Bangladesh, is currently facing displacement threat of local black tiger shrimp by low priced Vannamei shrimp from other countries, especially India. The Bangladesh government does not allow cultivation of Vannamei shrimp because of its greater disease proneness. Export sales of black tiger shrimp from Bangladesh dropped 21 per cent year-on-year to $189 million in the first four months of the 2018-19 fiscal year. The Bangladesh government is now undertaking a feasibility study to allow farmers to grow Vannamei without risking cultivation of traditional black tiger shrimp.

How likely is it for the export industries of Bangladesh to circumvent these challenges? If past experience is any guide, the resilience of our entrepreneurs provides hope that our export industries facing these challenges will be ultimately bailed out.

In July 1997, the European Commission imposed a complete ban on imports of shrimp from Bangladesh into the EU on the ground that exports of this commodity did not meet the provisions of their HACCP (Hazard Analysis Critical Control Point) regulations. Following that, there was massive revamping of health and hygiene standards in the shrimp processing plants in Bangladesh and the ban was ultimately lifted.

When the Multi-Fiber Arrangement (MFA) was phased out at the beginning of 2005, the IMF predicted that 50 per cemt RMG units in Bangladesh would close down. In reality, Bangladesh's RMG export thrived by diversifying into newer products and newer markets in the period following MFA phase out.

The World Bank, in a detail technical study during 1980s, resolved that upstream textile industry would not be viable in Bangladesh because of its high capital intensity and the high cost of capital in Bangladesh and advised Bangladesh to concentrate instead on downstream industry such as dyeing and finishing and RMG, which are more labour-intensive. This pessimistic prediction has also been negated by Bangladeshi entrepreneurs and today state of the art textile mills in Bangladesh are successfully competing in the export of yarn with countries who are the very source of raw material for yarn production in Bangladesh. A significant amount of deemed export also takes place out of these industries through their supply of yarn and fabric to export oriented RMG enterprises.

The USA withheld GSP facility to Bangladesh in 2015 while it extended trade facilities to African and Caribbean least developed countries (LDCs). Bangladesh could withstand the competition well and her export to USA, if anything, has grown during the past years.

The Rana Plaza incident was a major shock that put the RMG industry in a serious image crisis. However, the industry has managed to overcome this crisis and today Bangladeshi RMG enterprises are amongst the most compliant and environment-friendly units in the world. Also, the subsequent switch to higher technology by bulk of the RMG enterprises have rendered them more efficient and productive. The industry is now well-poised to compete in the international market effectively.

Bangladesh has also registered remarkable success in pharmaceutical export. Despite being a third world country, Bangladesh exports sensitive health product like medicine to 144 countries including USA and some European countries and the volume of export is steadily rising. Bangladesh's medicine export soared 25.6 per cent year-on-year to $130 million last fiscal year.

The agro-processing industry of Bangladesh has made significant foothold in the international market and is gaining access, even to developed country markets. Other upcoming success stories include export of bi-cycles and local brand electronics.

But the export performance of Bangladesh remains way below its potential because of constraints relating to infrastructure, port and energy that critically affect competitiveness of the production sector of the economy. However, the ongoing intensive efforts of the present government towards resolving these problems is likely to pave ways for greater success in export in the coming days.

A critical macro policy, which is adversely affecting the external sector of the economy, is the current misalignment of the exchange rate. The fact that Real Effective Exchange Rate (REER) indicates exports becoming nearly 7 per cent more expensive between 2015-16 and 2018-19 despite nearly 5 per cent depreciation of the nominal exchange rate during the same period provides a handy explanation of why Bangladesh has been falling behind the export performance of her major competitors.

If the efforts of the present government towards resolving infrastructure related constraints are coupled with supportive fiscal, monetary and exchange rate policy, then the resilience of our external sector will be once again vindicated. Some economic analysts have expressed apprehension about the "cloud gathering around" the external sector of Bangladesh. Hopefully, the underlying strength of our external sector will prove, as did in the past, such concerns to be outcome of blurred visions.

Dr Zaid Bakht is Chairman, Agrani Bank and former Research Director, BIDS.

zaidbakht@gmail.com

© 2026 - All Rights with The Financial Express