Workers at an RMG factory in Bangladesh — FE Photo

Workers at an RMG factory in Bangladesh — FE Photo ![]() The county's export sector has confronted the second generation challenge, i.e. failure to diversify its export base beyond readymade garments (RMG) sector. Its US$45 billion worth of export is overwhelmingly dominated by RMG products (85.0 per cent of total export).

The county's export sector has confronted the second generation challenge, i.e. failure to diversify its export base beyond readymade garments (RMG) sector. Its US$45 billion worth of export is overwhelmingly dominated by RMG products (85.0 per cent of total export).

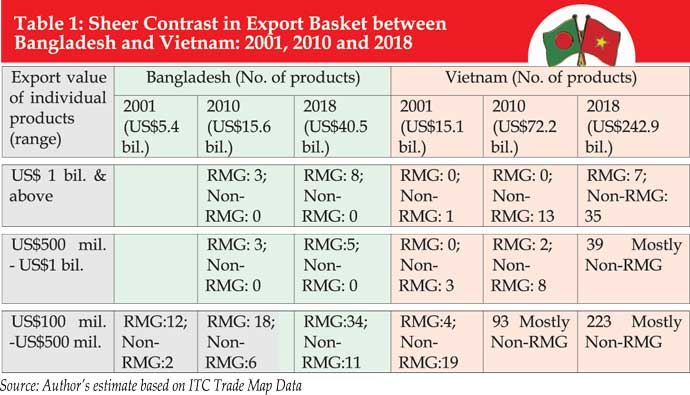

More specifically, there are only eight (08) products with an export over US$1.0 billion each and none of them are non-RMG products. Similarly, there are five (05) export products with export worth over US$500 million each and those are all related to RMG sector. Only 11 non-RMG products out of 45 products are found to have exported goods valued over US$100 million each. Majority of export products is within the range of US$1.0 million-100 million (430 products) and less than US$1.0 million (1808 products). Even as many as 2,125 products are found to have no exports.

Over the years, Bangladesh's export has increased from only US$5.4 billion in 2001 to US$45.1 billion in 2018 and the export base has been slowly diversified with higher number of products but most of those are RMG products.

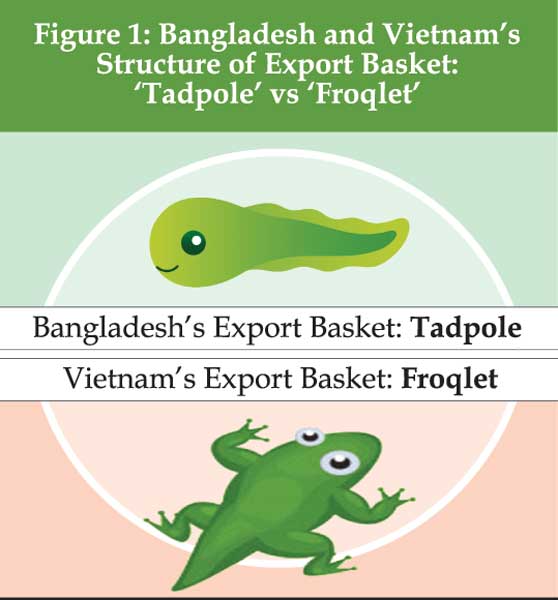

Structurally, Bangladesh's export basket looks like a 'tadpole' (Figure 1) - little frog with large head-like product basket based mostly on RMG products and a large long tail of small amount of export of different types of non-RMG products. The challenge for Bangladesh is to transform its tadpole-like export basket into a matured frog-like structure with balanced composition of RMG and non-RMG products.

Comparison between Bangladesh and Vietnam: From export diversification point of view

Bangladesh's export sector is often compared by stakeholders with different Asian exporting countries. However, Bangladesh is way behind one of its competing countries - Vietnam. Although Bangladesh's growth in export is often referred to as a 'success' case among least developed countries (LDCs) for becoming a major global exporter of RMG products, Vietnam's growth in export during 2001-2018 was much appealing, which increased from only US$15 billion to US$243 billion. Vietnam has higher number of products in all upper export categories vis-à-vis that of Bangladesh. A comparative assessment of growth of number of products in different range of export (in terms of value) indicates that Vietnam's export success depends mainly on non-RMG products such as petroleum, rice, footwear, coffee, shrimps and data processing machines, telephone parts, electronic circuits, transmission machines, and liquid crystal device, parts and accessories. RMG products have played a partial role in its growth in export over the years; more importantly, Vietnam's RMG export base is more diversified than Bangladesh's.

Overall, Vietnam should be the reference point for Bangladesh for export diversification, not for export concentration in RMG products. Interestingly, Vietnam's export basket is more matured than Bangladesh's and structurally, Vietnam's export basket looks like a 'froqlet' - young frog with balanced development of its body with little long tail having different export products and smaller amount of export of other products (Figure 1)

Bangladesh's challenge is to transform its export base from 'tadpole' to 'froqlet' by raising new export products with the range of US$1.0 billion, US$500 million - US$1.0 billion and US$100 million and US$500 million categories (Table 1). In this context, Vietnam could be a good reference point for Bangladesh mainly because of Vietnam's huge capacity of manufacturing export, diversity in export base, depth in intra-sectoral export products, availability of skilled workforce, competent domestic and foreign entrepreneurs and necessary infrastructural and logistic facilities.

Bangladesh's challenge is to transform its export base from 'tadpole' to 'froqlet' by raising new export products with the range of US$1.0 billion, US$500 million - US$1.0 billion and US$100 million and US$500 million categories (Table 1). In this context, Vietnam could be a good reference point for Bangladesh mainly because of Vietnam's huge capacity of manufacturing export, diversity in export base, depth in intra-sectoral export products, availability of skilled workforce, competent domestic and foreign entrepreneurs and necessary infrastructural and logistic facilities.

Export of non-RMG products of Bangladesh

Bangladesh's non-RMG sector's current export is about US$6.4 billion which accounted for about 15.8 per cent of total export in 2019. Major non-RMG export products include shrimps, dry food, pharmaceuticals, plastic products, leather, leather products and footwear, cotton products, raw jute, jute yarn, home textiles (kitchen, toilet lines), caps, iron steel, engineering equipment, optical, photographic and medical equipment and furniture. Only a few of these products have an export value over US$100 million and they include frozen shrimps, footwear, single yarn jute, hats, synthetic tents, toilet/kitchen linen, multiple folded jute yarn, footwear, jute textiles, bed linen and tobacco.

None of these products reached the US$1.0 billion mark till date. In other words, exploring the potential of US$1.0 billion worth of non-RMG products and developing them as 'next to RMG' products should be the priority of the concerned stakeholders.

Challenges for export diversification - A different narrative

Bangladesh's export sector has confronted a number of weaknesses and challenges towards diversifying its export base beyond RMG products. This author has tried to revisit those challenges from a non-conventional perspective. A set of alternate narratives of those challenges are presented below.

Bangladesh's export sector has confronted a number of weaknesses and challenges towards diversifying its export base beyond RMG products. This author has tried to revisit those challenges from a non-conventional perspective. A set of alternate narratives of those challenges are presented below.

a) Limited number of competent exporters in non-RMG sectors

Unlike the RMG sector, most of the non-RMG sectors have been dominated by few competent manufacturers and exporters. Often these exporters are found to be large-scale manufacturers with exposure to other sectors as well. The non-RMG sectors are often recognised by operations of few big local brand names, whether it is in case of leather products, or ceramic products, or plastic, textiles, home textiles, frozen shrimps or pharmaceuticals. These manufacturers/exporters usually work as suppliers of limited number of buyers/brands of major developed and developing countries and produce different categories of export products at a targeted amount. Under such circumstances, it is difficult to raise overall export of particular products at a higher level by this limited number of exporters (for example, reaching export value US$1.0 billion or above).

According to the experience of other countries, an industry becomes successful in the export market (having high export values) when it could ensure competition with the presence of large number of suppliers and buyers in different segments of the value chain. Unfortunately, most sectors fail to ensure participation of large number of suppliers in the domestic market which is a major weakness in terms of competition, product development, and capacity building for different products, technological development and overall entrepreneurship development in a particular sector.

b) Absence of SMEs in non-RMG value chains

A successful global value chain develops with participation of small and medium sized enterprises (SMEs) in different segments of the value chains, such as raw materials, intermediate products, main products and marketing of finished products. Most of the non-RMG sector value chains have provided limited opportunities for SMEs to participate in different segments of the value chain as large scale enterprises build their own value chains with huge investment from raw material development/procurement towards the end of marketing of products. Consequently, such investment in backward and forward linkage parts of the value chain constrained these large enterprises to investment and to put more focus on key production-related activities. Better access to SMEs in the value chains is crucial for developing backward and forward linkages of different non-RMG value chains.

c) Dual market-focus limits enterprises to concentrate in the export market

Most of the non-RMG sectors have been developing with dual market focus identity - domestic market and export market. As a result, enterprises of non-RMG sectors develop their products targeting both domestic and export markets. Consequently, enterprises often fail to put sufficient emphasis on market specific compliance requirements in terms of labour standards, decent wages, workplace safety and security, waste management and industrial pollution, sanitary and phyto-sanitary standards, level of CO2 emission and other physical standards. Such examples are found in sectors such as leather and footwear, plastic, ceramic, textiles and pharmaceuticals.

Since domestic consumers are less aware about compliance standards, and there is limited pressure from enforcement agencies for maintaining compliances, enterprises often try to avoid maintaining standards as per national rules and standards. That perverse attitude at the enterprise level adversely affects maintaining required standards and compliance for products manufactured for export-markets.

d) 'Openness' in policy statement but 'Restrictive' in practices in attracting FDI

Foreign investors are often disheartened in investing in domestic tariff areas (DTAs usually called non-EPZ areas) as the domestic businesses do not practice what are mentioned in the FDI-related policy documents (FDI Act, 2008, Industrial Policy 2016). Most of the business associations related to manufacturing sector are not so welcoming to FDI with fear of competition from outside.

Foreign investors who expressed interest to invest and registered for making investment, are found to be with a small share of their registered investment finally realised. In case of Bangladesh, rate of realisation of FDI registered, is about one fourth of total registration of FDIs. It appears that local investors particularly those of large scale investors have reached a level where they intend to maintain their market share with limited focus to broaden the market base by offering adequate diversified products from other investors. In this context, inflow of FDI which could offer new technologies, ideas and product development in different non-RMG sectors, need to be welcome by the government and the private sector.

e) Limited global exposure of non-RMG products

Unlike RMG products, Bangladesh is little branded by non-RMG products at the global level. Given the large number of RMG buyers/their representatives visited Bangladesh every year in assessing performance of suppliers, attending trade shows organised in Bangladesh and abroad, and interacting with local suppliers on a regular basis, it wouldn't be difficult to introduce local non-RMG products to these brands/buyers in due course.

Bangladesh's export of non-RMG products in most cases did not happen through first-party buyers/brands/ retailers, rather those are exported through third party buyers/buying houses who usually avoid such compliance standards for buying at lower prices. Without developing products with buyers' specification and standards, it would be difficult to raise export basket with non-RMG products. In this context, non-RMG products need to provide more exposure to the global trade/fashion shows organised by the EPB in different important cities.

f) Policy support promotes 'export concentration' instead of promoting 'export diversification'

The government in principle promotes export diversification which is reflected in different policy documents such as 10-year Perspective Plan, Seventh Five-Year Plan, the ruling party's election pledges (2018), and different targets of SDGs. In contrast, the government's operational fiscal and budgetary measures usually announced with the national budgets incentivise export of only few products/sectors (i.e. RMG). Given the limited resources available for disbursement among export sectors, the government could provide miniscule share of resources to non-RMG sectors. In other words, the government's fiscal measures appeared to be 'anti export-diversification'.

More importantly, whether the fiscal expenditure accrued to support the most important sector – RMG sector – ensures the targeted benefits, is questionable since despite those support measures the performance of the sector is modest particularly in the recent past. There is scope for restructuring of resources for RMG sector. Most importantly, fiscal incentives for the RMG sector should promote intra-RMG diversification for which fiscal measures need to be restructured and redesigned. The overall fiscal expenditures for industries need to be reversed where higher share of fiscal expenditure should be directed to non-RMG sectors with targeted measures. The Ministry of Finance in collaboration with the Ministry of Commerce and other relevant ministries and departments and business bodies and think-tanks could redesign fiscal incentive structures for the industrial sector.

Conclusion

Over the past several years, a number of international development partners along with the Ministry of Commerce have identified a number of non-RMG sectors which have potential to develop as 'next to RMG'. Some of these sectors are shipbuilding, jute-based products, non-leather footwear, bicycles, IT-enabled services, and pharmaceuticals, (The World Bank, 2016). There are potentials in other non-RMG sectors as well, such as plastics, ceramics, electrical and electronics, chemical and equipment.

However, diversification could also be explored within RMG sector in terms of developing non-cotton, synthetic products and man-made products. Besides, export diversification should be encouraged beyond traditional sectoral support measures to encourage small scale non-traditional exporters in the export market.

A number of non-traditional measures need to be ensured for promotion of non-traditional industries in the export market.

First, each export-oriented non-RMG industry must ensure participation of 'critical minimum' number of entrepreneurs in the value chain, particularly those of SMEs in different segments of the value chains, starting from raw materials to intermediate products and finished products. Second, the government should ensure clear separation of enterprises targeted to domestic market and export market. Enterprises working in the export market must comply with local and global standards and compliances. Third, Business associations should ensure necessary services at the 'pre-establishment' phases for foreign investors interested to invest not only in EPZ areas but also in non-EPZ areas. Efforts should be made to attract FDI under joint-venture initiatives in different RMG and non-RMG manufacturing sectors. Fourth, the Ministry of Commerce particularly through the EPB will ensure participation of non-RMG export products in their key global trade/fashion shows. If necessary, the EPB should extend necessary financial support to ensure participation of those exporters. Fifth, the Ministry of Finance should revisit the fiscal incentives provided to different industries for promotion of export. Major share of fiscal incentives will target non-RMG industries. Sixth, fiscal incentives and supports could be extended to potential entrepreneurs with good track record in export to promote export of non-traditional products. Seventh, the government needs to ensure growth and development of different non-RMG sectors through time-bound sectoral and strategic trade policy and therefore, targeted fiscal instruments and trade facilitation measures need to be ensured.

Dr Khondaker Golam Moazzem is Research Director at Center for Policy Dialogue (CPD).

moazzem@cpd.org.bd

© 2026 - All Rights with The Financial Express