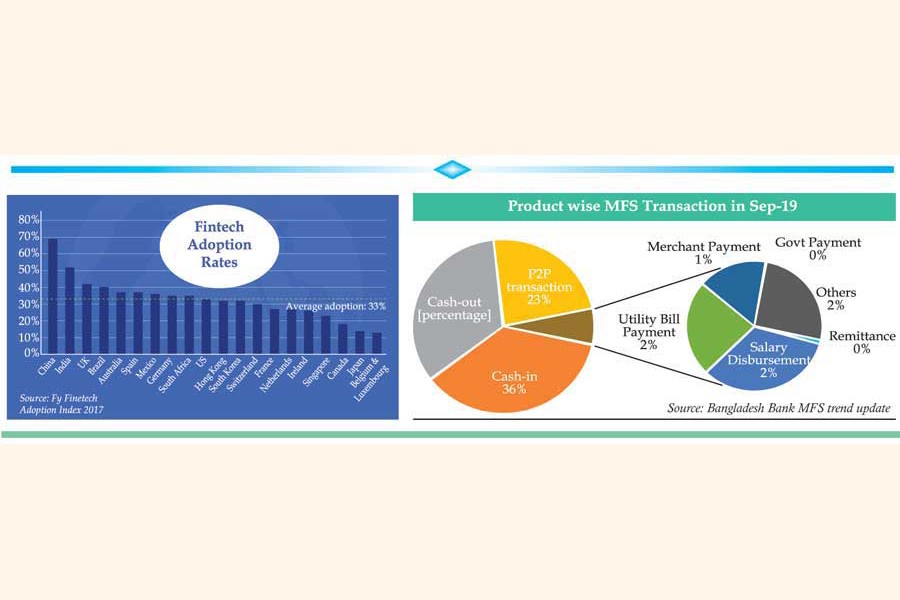

![]() In 2017, EY studied 69 major economies and found the average fin-tech adoption rate at 33 per cent with China, India, and the U.K. retaining top-three spots in the list:

In 2017, EY studied 69 major economies and found the average fin-tech adoption rate at 33 per cent with China, India, and the U.K. retaining top-three spots in the list:

Gartner Inc., an S&P 500 listed research institute, predicts that by 2030, 80% of financial firms will either go out of business or be rendered irrelevant by the new competition if they continue to maintain 20th century business and operating models. We have seen large Chinese banks reducing the number of employees while increasing investments in fin-tech development to offer their customer smart offline services, online banking and mobile banking solutions for the past couple of years. In first six months of 2019 alone, the Bank of China's replacement rate of electronic channels to branch businesses reached an astounding 93.73%. Imagine having access to credit, fund transfer, customized financial consultant and portfolio management facility all in your fingertips- ready to serve you at anytime and anywhere while not compromising security- no wonder you would switch to a fin-tech making these a reality than your brick and mortar banks in a heartbeat. The global fin-tech giant Alipay does more. Supporting transactions in 27 currencies, Alipay enables lifestyle expenditure, health checkups, tax payments and purchase of wealth management products, all within its app for its over 1.0 billion users in 50+ major economies. Betterment, a NY-based online investment firm with $15 billion in assets under management, enables robotic advisors to provide investment consultancy and individual tax management services. Circle, a 2014 Blockchain US-based startup, is already offering insane accessibility (like using a chat app to transfer funds) to transfer cryptocurrency along with usual major currencies. Security features- one of the major concerns involving financial transactions, are quickly shifting to newer technologies. An 8-digit or 20-digit long password is rendered almost obsolete in developed economies. Forrester finds that 61% of Singaporean financial institutions have already incorporated biometrics, such as fingerprints, iris and voice scan. Fin-tech has gone even further. PayPal finds iris scans "too old" and offers silicone chips beneath user's skin that can scan glucose level, vein patterns, heartbeat and more to provide multi-factor authentication for any activity that requires additional security. These explain the USD 122 billion in funding that went into fin-tech deals globally, 22 billion of it in just first 6 months of 2019.

Bangladesh's response to fin-tech

According to recent Financial Inclusion Insights (FII) data (2018), around 47% of Bangladeshi adults are financially included with 17% having a registered mobile money account. Although this country got introduced to fin-tech solutions in 2010 with the emergence of Bkash, as of September 2019 we have 16 operators and 75 million registered Mobile Financial Services (MFS) accounts conducting roughly 7 million transactions worth BDT 12 billion per day. Government is already working to enable transactions for mobile financial services from one operator to another within 2020. Digital wallet solution iPay, launched commercially in 2018, already has bagged 100,000+ downloads of its app in PlayStore. Although MFS and Wallet providers offer a wide range of facilities, cash-in and cash-out account for 70% of the transactions:

Identifying awareness issues as the biggest challenge to mobile services expansion, BRAC, the largest NGO in the world, is presently offering hands-on teaching to community members on DFS usage and has local Customer Service Assistants (CSAs) to assist in account opening and other issues. With these interventions, currently around 200,000 users are availing monthly savings deposit services and over 12,000 BRAC credit officers are using tablet devices for loan recovery management. With all these encouraging statistics, the Bangladesh fin-tech story has begun its journey beautifully and still has miles to go.

How banks can response

to the shift

Fin-tech is certainly disrupting many avenues in finance. Tech adopting consumers want solutions matching and encompassing their busy lifestyle. It is now much cheaper for a Non Resident Bangladeshi to transfer money internationally through Transfast than through a brick and mortar exchange house. An apparel worker can receive his or her wages, send it to their family residing miles away all in seconds and close to a million people are receiving these benefits now through combined efforts of fin-tech providers and apparel suppliers. All this is putting pressure on banks. But it is hard to see fin-tech replacing banks even if banks continue to operate following their traditional model. First, traditional banks as financial institutions have developed a strong heritage of procedures not only in terms of compliance, and products but also in their corporate culture. With their hundreds of years of expertise in lending and managing cash flows, banks will continue to have an edge over fin-tech startups in credit profiling. Also, fin-tech companies are growing fast but they are still tiny. Lending Club, the biggest fin-tech lender, has arranged USD 9 billion in loans since 2007-compared to USD 885 billion of credit-card debt in America alone.

Obviously, this does not mean that the traditional banks should ignore this phenomenon as growth of fin-tech solutions result from their own shortcomings. As fin-tech catchup to banks in size and scale, there are a number of opportunities open to banks to skew the benefits to their advantage:

Rethink brand (and value)

positioning

For a traditional bank, the focus should not be on a fin-tech closing a successful round of financing but rather its ability to present itself as a "bank without commissions" when in reality, their freemium service is very limited. The idea that those same customers who protest their banking charges and commissions every day may consider paying those amounts because "they are not a commission but an extra service" should be very interesting. This should evoke some questions about how effectively banks are reaching out to their consumers on issues' value propositions, customer centricity etc.

Cooperation beyond tech

The growing presence of customer-centric companies has just begun, but banks might consider cooperating with Fin-Tech companies beyond the need for synching their IT systems while learning from each other's strengths. While banks can provide fin-techs with credibility and trust factor, fin-techs can enable banks to explore new consumer data points, cut down on transaction time and cost and embed agility in their long established workflow.

Outsourcing, and not in housing

The fin-tech industry at the moment accounts for not just startups but also established financial institutions trying to implement Fin-Tech solutions. Banks also invest in, or even acquire Fin-Tech to use their technology internally or offer the service to their customers exclusively. J.P Morgan in 2018 acquired a payment startup WePayto that provides their 4 million small business clients with WePay's fast and rapid payment technology, thus adding to their service portfolio. Interesting when it comes to investing, banks outsource the expertise to fin-techs rather than building in house solutions. US banks alone have invested a staggering USD 3.6 billion in 56 different fin-tech startups and only 7% of banks have done the hardest job of setting up their proprietary solutions.

Although the adoption rate is encouraging, fin-tech is not capable of entirely replacing the banking and finance industry. But it is capable of steering it into the way of innovation and let it evolve naturally to a sphere where frustration over money transfer time and fees, 20-digit passwords and manual management of petabytes of information will be just a memory of the past. The smart thing for banks to do would be to acknowledge the need for change and collaboration, and be smarter in implementing the changes.

.......................................................

Ayesha Sabrina is an investment banker by profession. The views expressed here are of her own.

© 2026 - All Rights with The Financial Express