![]() It is by now quite well-known in the informed circles that Bangladesh is on its way to come out successfully in the next assessment in March, 2021, to be conducted by the Centre for Development Policy (CDP) of the United Nations social and economic council. This is expected to be the second consecutive success of the country to pass the three criteria set up by the CDP to be eligible to come out of the category of the Least Developed Countries (LDCs) and placed in the group of 'Developing countries'. The reason for the country's confidence to come out successfully in the 'assessment' is that Bangladesh, in the last assessment in 2018, passed all the three hurdles of Gross National Income (GNI), Human Asset Index (HAI) and the Vulnerability Index (VAI) with some margins in each case and continues to forge ahead with development in all the three categories. Although these criteria are often re-set by the CDP, and are sometimes called 'the moving goal posts' by many, Bangladesh has comfortably been going ahead with its progress in all the three areas. It is therefore strongly felt in the concerned circles and the others interested in our graduation to the 'Developing Country' status that it is only a matter of time when we will graduate. The rules are that if and when an LDC, like Bangladesh, comes out successfully in two consecutive triennial assessments by the CDP, it has to follow certain formalities under the supervision of the UN economic and social council for another three years to be finally taken note of by the UN General Assembly, and that is 'graduation' to the 'Developing Country' status. For us, that important year is going to be 2024. I do not elaborate on the formalities for our country to go through between 2021 and 2024 because the focus of this article is on another aspect of what has to be done by us after we are declared a 'Developing Country' by 2024.

It is by now quite well-known in the informed circles that Bangladesh is on its way to come out successfully in the next assessment in March, 2021, to be conducted by the Centre for Development Policy (CDP) of the United Nations social and economic council. This is expected to be the second consecutive success of the country to pass the three criteria set up by the CDP to be eligible to come out of the category of the Least Developed Countries (LDCs) and placed in the group of 'Developing countries'. The reason for the country's confidence to come out successfully in the 'assessment' is that Bangladesh, in the last assessment in 2018, passed all the three hurdles of Gross National Income (GNI), Human Asset Index (HAI) and the Vulnerability Index (VAI) with some margins in each case and continues to forge ahead with development in all the three categories. Although these criteria are often re-set by the CDP, and are sometimes called 'the moving goal posts' by many, Bangladesh has comfortably been going ahead with its progress in all the three areas. It is therefore strongly felt in the concerned circles and the others interested in our graduation to the 'Developing Country' status that it is only a matter of time when we will graduate. The rules are that if and when an LDC, like Bangladesh, comes out successfully in two consecutive triennial assessments by the CDP, it has to follow certain formalities under the supervision of the UN economic and social council for another three years to be finally taken note of by the UN General Assembly, and that is 'graduation' to the 'Developing Country' status. For us, that important year is going to be 2024. I do not elaborate on the formalities for our country to go through between 2021 and 2024 because the focus of this article is on another aspect of what has to be done by us after we are declared a 'Developing Country' by 2024.

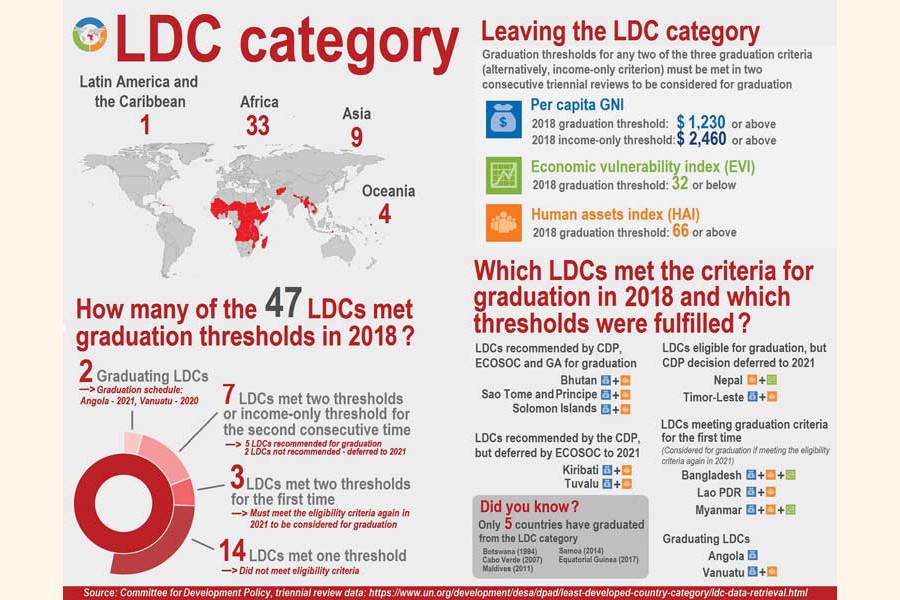

Our readers are, no doubt, aware that as an LDC, like all other 46 LDCs, we enjoy certain privileges in the areas of exports and credits and loans under the World Trade Organisation (WTO) agreements and facilities provided by the donor and lending agencies like the World Bank, the Asian Development Bank, International Monetary Fund (IMF), Japan International Cooperation Agency (JICA) and the likes of them. We are thus privileged to export, duty-free and quota-free (DFQF), to all developed countries, except the US, and to those developing countries, who are able and willing to allow us the facility. China, India and Korea are countries that fall under this category, who allow us the privilege. This duty-free and quota-free export is allowed under a scheme called Generalised System of Preferences (GSP). The World Bank, The IMF and other lending agencies provide us loans at concessional rates for our development projects. But since in the assessment of the UN, we are already a 'Lower Middle Income' country since 2015, the economy of Bangladesh is now called a 'blend economy', and at this stage we are granted loans at both soft and hard terms. But the sources for our loans, including loans for the credible private sector borrowers, are available from both the traditional multilateral agencies, the IBRD and other international banking institutions.

After our expected graduation in 2024, we would cease to be an LDC, and will no longer be entitled to export of our goods and services duty-and quota-free. Providing loans to us at concessional rates of interests by the multilateral agencies would be replaced by their normal chargeable rates. The European Union (EU), by a notification in 2012, amended in 2016, has extended duty-free-quota-free access to the European Union countries under what is called EBA (Everything but Arms) scheme for another period of three years after graduation of a country. It would be until 2027 in the case of Bangladesh. After that year, Bangladesh would not be entitled to the DFQF export facilities either under GSP or EBA. Nor would it be getting the privilege of borrowing from international sources, including the multilateral donor agencies, at concessional rates of interest.

The European Union, of course, does not completely shut all the doors and windows to exports from the new 'developing countries'. It keeps a couple of them open to these countries, but the DFQF facilities provided under the EBA scheme do not remain as such. The European Union, under a scheme known as GSP+, allows these countries to export some, but not all, of their goods and services to the EU countries on fulfilment of certain conditions. First, a country, after graduating out of the LDC status, has to apply to the European Commission for getting the facilities under GSP+ and state that it has come out of the LDC status. Secondly, the country so applying has to provide the proof that-- (a) not more than 7(seven) of its export items constitute 75% of total exports to the EU; (b) it has acceded to, and ratified, all the 27 conventions of the UN earmarked by the European Union; and (c) all the exports of the applicant country to the EU under EBA do not exceed 6.5% of the total imports of the EU, including those from the applicant country, under the EBA scheme from all the LDCs. On receipt of an application and being satisfied that all the conditions stated above have really been met, the European Union may allow duty-free export to its member-countries from the applicant country, but not all the products of the applicant country. They may cover only 66% of the tariff lines, or H.S. code, items of the European Union. And, upon allowing such conditional imports as stated above, the EU keeps on closely monitoring the compliance of the country with all of the those conditions. It should be clearly noted that all the conditions, without any exception, have to be met.

We may now begin an examination to see whether or not we will meet the conditions to qualify to get the benefits provided under the GSP+ scheme of the EU. Since our Readymade Garments constitute 84% of our total exports, and the EU is our largest export destination taking 62% of our RMG as their imports, we would fulfil the first condition, viz., that not more than seven of our export items account for 75% of our total exports under EBA to the European Union. I think, the remaining 10% would be filled in by the other six export items to the EU. Of the 27 conventions of the UN, we already have signed 26. The only one remaining is related to the abolition of child labour. We may sign this convention very easily and fulfil this condition as well. The remaining condition mentioned at © above calls for a closer look. The last time, quite some months earlier, we noticed in the records that our exports under EBA to the EU constituted more than 9%, instead of not more than 6.5%, of the EU's total imports under EBA. We have recently learned from reliable sources, though not actually seen yet on EU records, that our exports to the EU under the EBA scheme now constitute more than 14% of the EU's total imports under that scheme. May we again remind our readers that an applicant-country is required to fulfil all the conditions discussed above?

We may now begin an examination to see whether or not we will meet the conditions to qualify to get the benefits provided under the GSP+ scheme of the EU. Since our Readymade Garments constitute 84% of our total exports, and the EU is our largest export destination taking 62% of our RMG as their imports, we would fulfil the first condition, viz., that not more than seven of our export items account for 75% of our total exports under EBA to the European Union. I think, the remaining 10% would be filled in by the other six export items to the EU. Of the 27 conventions of the UN, we already have signed 26. The only one remaining is related to the abolition of child labour. We may sign this convention very easily and fulfil this condition as well. The remaining condition mentioned at © above calls for a closer look. The last time, quite some months earlier, we noticed in the records that our exports under EBA to the EU constituted more than 9%, instead of not more than 6.5%, of the EU's total imports under EBA. We have recently learned from reliable sources, though not actually seen yet on EU records, that our exports to the EU under the EBA scheme now constitute more than 14% of the EU's total imports under that scheme. May we again remind our readers that an applicant-country is required to fulfil all the conditions discussed above?

The European Union is going to review the entire EBA scheme sometime in 2023, just a year ahead of our projected graduation out of the LDC status in 2024. The EU is on record to have made upward revision of this condition of limit on the exports of an LDC not exceeding a certain percentage (6.5% at present) of the total import into the EU under the EBA scheme. They started with 2% and now stand at 6.5%. We already have noted that they are going to review this scheme in 2023. If they go for an upward revision, and if our expected larger volume of exports under the scheme after graduation in 2024 still remain within a hoped-for enhancement of this percentage limit, we may be granted the privileges of a GSP+ country's exports to the EU. But as it now appears to the present writer, even if the EU makes an enhancement of this upper limit for exports, it is unlikely to cover our hoped-for larger volume of exports at that time. It therefore appears more likely that we, as a country, have to face a tariff regime for our exports to countries where we now enjoy duty- and quota-free export benefits. It simply means, the competitiveness of our exportable goods and services will be reduced to the extent that is the rate of tariffs on different items of our exports to different countries.

How to face the challenges of the tariff walls raised against our exports: First of all, coming out of the rather unenviable status of the membership of the group of the poorest countries of the world, and getting into another of relatively well-off countries, should, in itself, be a matter of pride rather than one of fear and apprehension. Secondly, since the creation of this group of LDCs in 1971 and our getting bracketed into it in 1975, many other countries have got into, and come out of, it. The first point to consider is how and why a country, after graduating out of the LDC status, may again relapse into that old status. This may happen for the simple reason that, after graduation to the status of a developing country, it may experience a fall in at least two of the three criteria of graduation and thus revert to the old status of an LDC. This once happened to the Maldives, although it again came out of the LDC status, and is now a developing country, again. But there is also a condition here. A country having a population of 75 million or more is not allowed to, officially, revert to the status of an LDC once it comes out of that status, although it might actually have fallen to that status when it comes to considering its position with regard to the hurdles of fulfilling the three conditions discussed earlier. Bangladesh, with its population size, would therefore not be allowed such a highly unwelcome reversion, should the situations of Bangladesh ever come to such an undesirable pass. So the only way open before us is to go ahead and face the realities of a world of trade regime with tariffs imposed on our goods and services by all other countries of the world, like the rest of the world of developed and developing countries, partially after our graduation in 2024, and fully after 2027, once the extended period of three more concessionary years allowed by the EU expires.

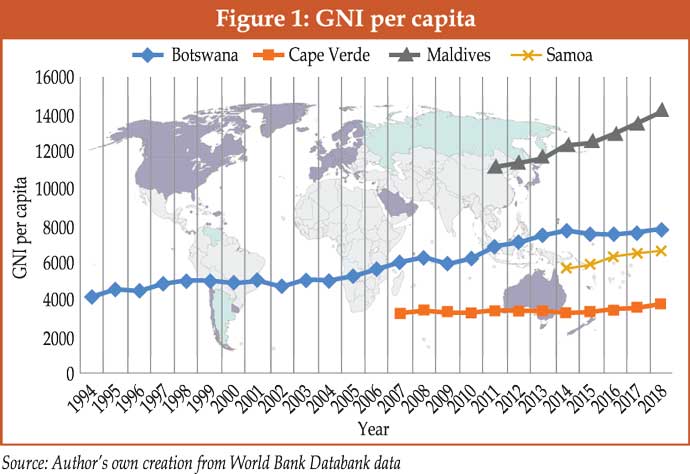

We may now venture out to take a look at what might happen after graduation of a country out of the LDC status. We know only 5(five) countries have till now, since introduction of this LDC status in 1971, come out of the bracket and are now 'developing countries'. The names of those countries are shown below with their respective year of graduation within brackets against each. We show the position of four out of five graduated countries because the latest one, namely Equatorial Guinea, having graduated only in 2017, would not present a picture depicting any clear trend in any direction. The first country is Botswana, graduating in 1994, and the other three are Cape Verde graduating in 2007, The Maldives in 2011 and Samoa in 2014.

Figure 1 shows, in different colours, the trend of growth of GNI per capita of each of those four countries beginning from their respective year of graduation till 2018, the figures for 2019 cannot yet be shown as the year is yet to come to an end. It perhaps needs no explanation that the vertical axis in graph 1 shows the amount in dollars per head while the horizontal one shows the years, beginning from the graduation of each and ending in 2018. We thus find that Botswana, graduating in 1994, and shown in blue, dotted line in the graph, started with a GNI of US $ 4,128.1/ and has a secular upward trend with slight ups and downs on the way reaching, finally, nearly US $ 7,751.17/- in 2018. Cape Verde, a rather small country starting with US $ 3,211.74/- or so in 2007, and represented by the line in orange, has gone slightly higher than the beginning, reaching $ 3703.89 in 2018. Samoa, comprising mainly two islands in the south Pacific, graduated in 2014 with a GNI per capita of US $ 5,620/- registering a growth of $ 6,620/- in 2018. And, finally, the Maldives, graduating with a per capita GNI of $ 11, 160/- in 2011 reached $14,120/- in 2018.

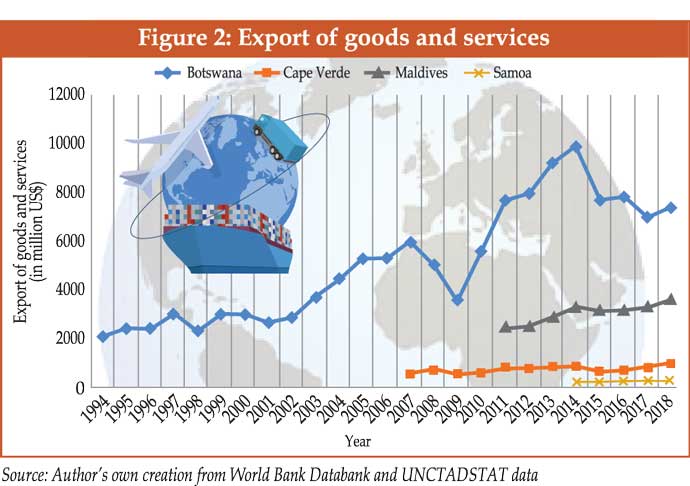

The growth of exports of goods and services of those countries, beginning from their respective years of graduation till 2018, likewise, shows an upward trend with some degrees of variation from one country to another. It is shown in Figure 2 (Page-11).

For Botswana, it rose from $ 2060 million to $7,326 million, for Cape Verde, from $ 565.70 mn to $970.80 mn in 2018, and for the Maldives, it is 2444.77 million in 2011 to $ 3629.05 mn in 2018.

What is very remarkable about all these four countries graduating from their LDC status in different years to the status of developing countries and, thus, being constrained to forego the facilities of DFQF exports and concessional loans, is they all have developed with their respective GNIs per capita and export of goods and services generally steadily growing, except in the case of Cape Verde, which either remains at the same level or rising very slightly in 2018-19. This empirical study unequivocally shows that graduating out of the status of an LDC, as Bangladesh is on its way to do so in 2024, holds out a prospect of assured growth and development instead of the unfounded fear and apprehension of stagnation, or even decline, as some might tend to think. But we have to adopt certain national policies to do that, and I am going to touch upon them very briefly in the following paragraphs.

But this fact should not make us complacent at all. The relatively newly-graduated countries we have discussed are either small island countries, like Samoa, with very small population or, like Botswana, as if, ensconced in the lap of a larger country like the Republic of South Africa. Their economies, population, GNI, international trade with two or three exportable items are all very small.

The case of Bangladesh is going to be very different and vastly difficult, once it graduates out of the LDC status. It is already a $300 billion economy with a trade volume of nearly 40% of the GDP and export earning accounting for nearly $46 bn, all growing under the protective shade of GSP and EBA with some contribution of SAFTA, APTA, etc. While saying this, I do not, in the least, forget the enterprise, innovation and extremely hard work of our entrepreneurial class, who have helped make Bangladesh a country we all do now rightfully feel proud of. But with graduation in 2024 with partial closure of the gateway to the opportunity of duty-free exports and with EU's withdrawal of EBA under GSP after their extended period in 2027, we are going to face the full blast of imposition of duties and other charges on our exports to all countries of the world. That simply means our competitiveness in international trade will substantially shrink and our economy would risk sliding back to a poorer state. But there are ways to re-adjust to new realities and keep our development momentum going. We may now touch upon those well-known ways to face these post-graduation challenges.

There are now talks about FTA (Free Trade Agreement), PTA (Preferential Trade Agreement), CEPA (Comprehensive Economic Partnership Agreement) all around. There is also a muted blame game on why the competent authorities so far have not signed any of those with any country when we all were aware the post-graduation tariff regime was fast approaching. Let us now refresh our memories of what is going to be the international trade scenario for Bangladesh after our graduation in 2024 with the rest of the world other than EU, which will join the rest after 2027. We have said before in this article and say it again that the competitiveness we now enjoy in the case of our exports to the rest of the world will be eroded after 2024 to the extent that would be their import duty and other charges. The case would be the same for EU also after 2027, unless, of course, the EU and/or the rest of the world make any change in their tariff structure by that time. It is now time to take a cursory look at what are going to be the conditions of our 'competing' countries, i.e., the countries, irrespective of their present economic status, export the same or similar types of goods and services to the same destinations.

There are now talks about FTA (Free Trade Agreement), PTA (Preferential Trade Agreement), CEPA (Comprehensive Economic Partnership Agreement) all around. There is also a muted blame game on why the competent authorities so far have not signed any of those with any country when we all were aware the post-graduation tariff regime was fast approaching. Let us now refresh our memories of what is going to be the international trade scenario for Bangladesh after our graduation in 2024 with the rest of the world other than EU, which will join the rest after 2027. We have said before in this article and say it again that the competitiveness we now enjoy in the case of our exports to the rest of the world will be eroded after 2024 to the extent that would be their import duty and other charges. The case would be the same for EU also after 2027, unless, of course, the EU and/or the rest of the world make any change in their tariff structure by that time. It is now time to take a cursory look at what are going to be the conditions of our 'competing' countries, i.e., the countries, irrespective of their present economic status, export the same or similar types of goods and services to the same destinations.

If we take into consideration our single largest export product, that is, Readymade Garments, now accounting for 82% of our exports, we often boast that we are the second largest exporter of this item in the world, China being the first, the gap between the two is frighteningly wide. Countries like Vietnam, Indonesia, Cambodia, India, Pakistan, Turkey, Sri Lanka and many others are exporters of this item. We are now neck and neck with Vietnam and not very far ahead of India and a few others. Vietnam has very recently entered a free trade agreement with the EU, and will soon start exporting to the EU market goods and services duty-free. So our RMG and all other exportable items will start losing place to Vietnamese goods and services, and EU is the largest destination for our RMG and many other items. India is far advanced in its negotiations for an FTA with the ASEAN. We may cite many examples of our 'competing' countries reaching FTAs, PTAs or other kinds of trading arrangements threatening our exports. We have therefore to follow the suit if we want to honourably survive in the unkind world of cut-throat competition.

The informed circle is, no doubt, aware that China has offered to sign an FTA with Bangladesh. Not to be outdone, India has taken a longer stride, and offered to sign a Comprehensive Economic Partnership Agreement (CEPA) with Bangladesh. Bangladesh responded positively to the offers of both the countries and preliminary discussions started some time ago, although both of them now seem to be slowing down their speed. Now, China and India are our two largest trading partners. But these agreements with both the countries are bound to come in order for us to remain competitive in their markets. But at what cost to our revenue from imports from those two countries? In the year 2018-19, duties and taxes collected at the import stage on goods imported from China stood at Tk 14,148.38 crore while the same for India stood at Tk 12,495.59 crore. The total revenue collected on imports from these two countries for the above period stood at Tk 26,643.91 crore. It is 10.10% of our total revenue collected at the import stage from these two countries.

The stakes on our revenue collection from imports are very high if we go for CEPAs, FTAs, PTAs, etc with more and more countries. The question may arise as to why should we, then, go for those kinds of agreements with other countries? The answer to this question is not very difficult to provide. With our graduation to the status of a 'developing country', our exports to the countries all over the world would be charged duties and taxes at the rates prevalent in each country on individual items. In order therefore to keep our duty-free access to as many of those countries as possible, we must enter one or the other of the agreements mentioned above just not to be shut out from those markets and outdone by our competing countries, many of whom have already concluded a sizeable number of such agreements. Hence we must open negotiations in right earnest with our trading partners, especially with those, first, where our exports are high. In practical terms, that would mean opening FTA or some such negotiations with the EU, China, India, Japan, Australia, USA, Canada, and other countries falling under that category. Many of those countries may not show much interest to open negotiations with us at this stage of our economy and other social conditions. But we should open it with those who agree to do so now. It must be kept in mind that concluding an agreement of those kinds generally takes years; so even if we may be able to make some of them agree to open negotiations now, it may be concluded sometime after our graduation.

I always felt frustrated, and do so still, as to why our country does not apply to join the RCEP, an upcoming trading bloc comprising the ASEAN+6 countries. It means all the countries of ASEAN like Myanmar, Thailand, Singapore, Vietnam, Laos, Cambodia, The Philippines, Malaysia, Indonesia and China, India, Australia, Japan, etc. The EU is also in negotiations with the ASEAN for an FTA. If we do not join RCEP, we will be outbid by countries like Vietnam, Indonesia, Cambodia, Myanmar, etc. in the markets of China, India, Malaysia, Indonesia, etc. This November, 2019, is probably the last month to apply for membership of RCEP. I think, Bangladesh should make up its mind and apply to join this group. As things now stand with regard to RCEP, it may still take quite a few years for the agreement to conclude, but the time to apply for it is running out fast.

I am aware, there are differences among the policy makers as to whether or not we should join RCEP, a grouping of countries. Those who hesitate, offer the argument that our national budget being so heavily dependent on customs, the related revenues may get an unmanageable jolt if and when this grouping comes into effect and we are a member of it. But we should keep in mind that if this grouping really comes into effect and we are not a member of it, we will be nowhere with our exports. Although there are a few undercurrents of tensions, like the existing politico-economic rivalry between China and India, standing in the way of its early conclusion, it might be too late for us to apply for membership if and when those undercurrents are somehow or other patched up.

The fear that we would lose Customs revenue is very real and is not easy to address. But it is also very real that the two-phased withdrawal of duty-free export of the country in 2024 and 2027 are also rushing towards us and we must be prepared to face it. One way to tackle our heavy dependence on Customs and the related import charges may be to gradually reduce them in tolerable doses through each year's budget before 2024 so we may not get an intolerable jolt when the severe reduction comes with graduation. As explained earlier, the withdrawal of our import duties and charges is not accompanied by graduation; nor is it a pre-condition for that. It is our own necessity for retaining our export markets for continued economic development through retention of duty-free market access by other means. And it is possible by entering into FTAs CEPAs, PTAs, etc. Side by side with gradual annual reduction of import duties and charges, our tax efforts must be strengthened manifold. FDIs will come if we enter FTAs. This will actually mean a fundamental economic re-structuring. We must undertake it in order to realise our dreams of becoming a developed country. The alternative of not taking these steps in time will mean stagnation, or even decline. That is a state of affairs nobody in his right mind will ever want to happen to his country.

Besides expanding the areas of our duty-free market access through FTAs, CEPA, etc. we should, at the same time diversify our range of products for exports. Moreover, we must improve our overall productivity, whether of labour, machinery, transportation or of organisation. We have a host of other areas where we need to pay closer attention to improve our productivity. We do not go into details of those areas in order not to make the discussion too unwieldy.

.............................................................

Ali Ahmed, a former Member (Customs) of the National Board of Revenue, now works as the Chief Executive Officer, Bangladesh Foreign Trade

Institute (BFTI). aahmed48@gmail.com

© 2026 - All Rights with The Financial Express