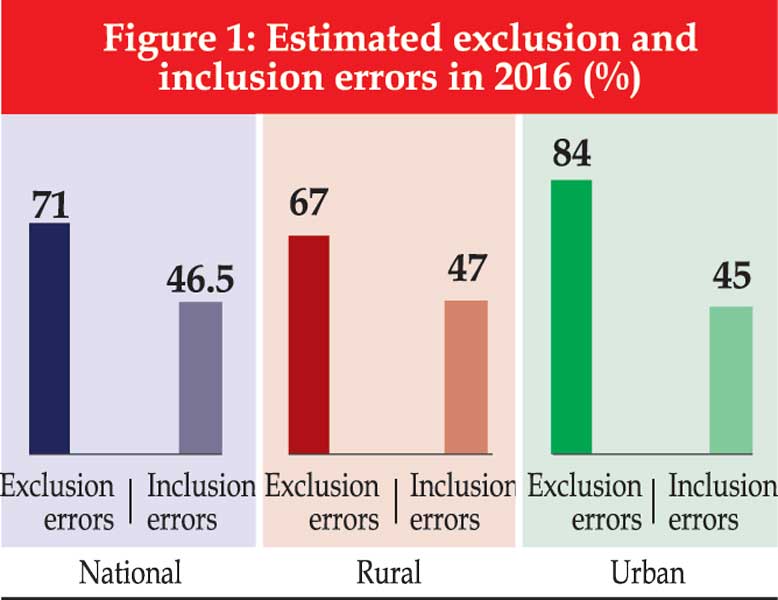

![]() Each year Bangladesh spends about of 2.2 per cent of its GDP on various social security programmes, predominantly targeting the poor. Assessments of selection issue using Household Income and Expenditure Survey Data (i.e. various HIESs - namely HIES 2016 and HIES 2010) suggest that the selection methods adopted in Bangladesh to target the poor has been inefficient resulting in high level of under coverage of poor and leakage. Under coverage, which is also known as 'exclusion error', denotes the sum of actual poor wrongly classified as non-poor as a proportion of the total poor. On the other hand, leakage known as 'inclusion error', is the sum of actual non-poor incorrectly classified as the impoverished as a proportion of the total poor (Johannsen, 2006). According to HIES (BBS, 2016) data, the incidence of under coverage was 71 per cent and leakage was 47 per cent in 2016. Due to these high levels of under coverage and leakage, social security spending has failed to attain the desired impacts on poverty and inequality. Against this background, the government has undertaken a project to develop a comprehensive database of all households (known as the National Household Database - NHD) and use 'Proxy Means Test (PMT)' model to improve the selection of poor and thereby reduce the high level of exclusion and inclusion errors. The key objectives of the model as stated in the NHD project (2019) are:

Each year Bangladesh spends about of 2.2 per cent of its GDP on various social security programmes, predominantly targeting the poor. Assessments of selection issue using Household Income and Expenditure Survey Data (i.e. various HIESs - namely HIES 2016 and HIES 2010) suggest that the selection methods adopted in Bangladesh to target the poor has been inefficient resulting in high level of under coverage of poor and leakage. Under coverage, which is also known as 'exclusion error', denotes the sum of actual poor wrongly classified as non-poor as a proportion of the total poor. On the other hand, leakage known as 'inclusion error', is the sum of actual non-poor incorrectly classified as the impoverished as a proportion of the total poor (Johannsen, 2006). According to HIES (BBS, 2016) data, the incidence of under coverage was 71 per cent and leakage was 47 per cent in 2016. Due to these high levels of under coverage and leakage, social security spending has failed to attain the desired impacts on poverty and inequality. Against this background, the government has undertaken a project to develop a comprehensive database of all households (known as the National Household Database - NHD) and use 'Proxy Means Test (PMT)' model to improve the selection of poor and thereby reduce the high level of exclusion and inclusion errors. The key objectives of the model as stated in the NHD project (2019) are:

(i) to maximise coverage of the poor and vulnerable population given the limited budget;

(ii) to make the system fully consistent with the goal of universal coverage of the poor; and

(iii) to address the key challenge for building a cost-effective system to identify the poor.

Extent of exclusion and inclusion errors in Bangladesh

It may be concluded from both the administrative and HIES (BBS 2016) data that social security beneficiary coverage (30 per cent and 27.8 per cent according to ministry of finance and HIES) in recent years is higher than the poverty incidence (i.e. 24.3 per cent in 2016). The effective coverage for the poor may be substantially lower when the exclusion errors and inclusion errors are considered.

It may be concluded from both the administrative and HIES (BBS 2016) data that social security beneficiary coverage (30 per cent and 27.8 per cent according to ministry of finance and HIES) in recent years is higher than the poverty incidence (i.e. 24.3 per cent in 2016). The effective coverage for the poor may be substantially lower when the exclusion errors and inclusion errors are considered.

Exclusion errors are measured as the number of eligible individuals (defined by various indicators such as poverty, age, location, and other programme specific attributes) are not covered in the social safety net system as proportion of total eligible individuals. Inclusion errors can be defined as the number of ineligible beneficiaries as proportion of total such system beneficiaries. Using these definitions, the estimated exclusion and  inclusion errors in 2016 were 71 per cent and 46.5 per cent respectively. Exclusion errors were lower in the rural location (i.e. 67 per cent) compared to the urban areas (i.e. 84 per cent). Relatively, high exclusion errors in the urban area are perhaps due to the lower coverage of the system. Inclusion errors were slightly higher in rural Bangladesh compared to the urban location. The existence of high exclusion and inclusion errors mirror an inefficient social security system.

inclusion errors in 2016 were 71 per cent and 46.5 per cent respectively. Exclusion errors were lower in the rural location (i.e. 67 per cent) compared to the urban areas (i.e. 84 per cent). Relatively, high exclusion errors in the urban area are perhaps due to the lower coverage of the system. Inclusion errors were slightly higher in rural Bangladesh compared to the urban location. The existence of high exclusion and inclusion errors mirror an inefficient social security system.

Implication of inefficient selection in Bangladesh

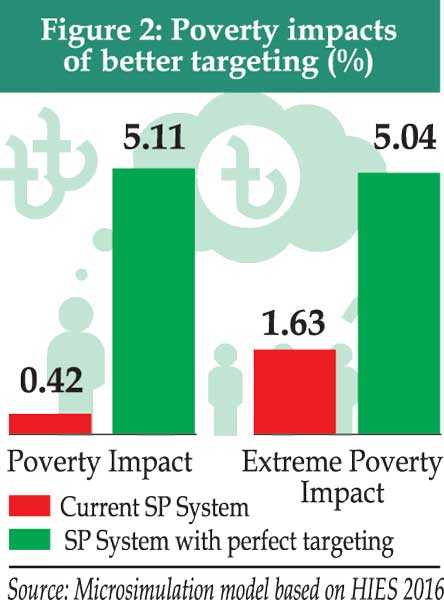

Poor selection of the poor is turned out to be costly in Bangladesh's pursuit of reducing poverty. Under the current system, additional poverty impacts of 2.2 per cent GDP spending is only 0.42 per cent (i.e. the difference between poverty rate of 24.3 per cent with social security and 24.81 per cent without it). However, improve (or perfect) targeting of deserving beneficiaries may have higher impact on poverty reduction in Bangladesh.

Micro-simulation using HIES 2016 suggests that if the resources saved from complete removal of exclusion and errors were spent on poor households -- the head count poverty measured by the upper poverty line declined by 5.11 percentage points (i.e. from 24.3 per cent to 19.7 per cent). This implies that with no or minimum extra programme cost, additional 7.4 million can be lifted out of poverty.  In case of lower poverty line, the percentage point decline was 5.1 -- implying that with no or small added programme cost, an additional 8.1 million can be pulled out of extreme poverty. Thus, due to large exclusion and inclusion errors, current social safety net programme is ineffective in Bangladesh -- measured by their impacts on poverty and extreme poverty. It is also concluded that there are high returns if targeting can be improved.

In case of lower poverty line, the percentage point decline was 5.1 -- implying that with no or small added programme cost, an additional 8.1 million can be pulled out of extreme poverty. Thus, due to large exclusion and inclusion errors, current social safety net programme is ineffective in Bangladesh -- measured by their impacts on poverty and extreme poverty. It is also concluded that there are high returns if targeting can be improved.

Selection methods

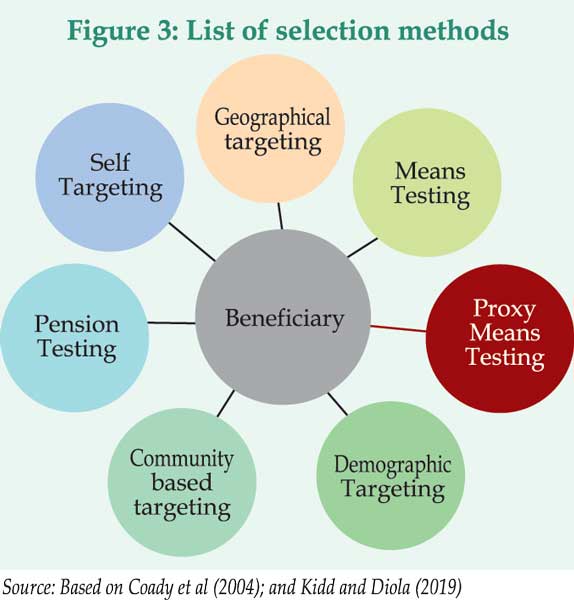

Targeting of deserving beneficiaries accurately has always been difficult. Given this difficulty, various targeting methods have been adopted in different countries and for different types of intervention programmes. Among them, one method -- 'Proxy Means Test (PMT)' has gained popularity thanks to the World Bank.

Since income (means test) is not easily measurable in low income countries, this testing has been promoted as an alternative to targeting the poor. It tries to predict a household's -- rather than an individual's -- level of welfare using an algorithm that is commonly derived from statistical models. Proxies for income are usually  determined through an analysis of national household survey datasets and are meant to be easily observable and measurable indicators that have some correlation with consumption or income. Usually, the proxies include: demographics; human capital; type of housing; durable goods; and productive assets. Surveys of all households (desired method) are conducted to generate data. Once the survey is undertaken, the data is fed into a computer and the algorithm is applied. Scores are allocated to households which are ranked from the poorest to the richest. A threshold is determined or is agreed upon for eligibility. Households with PMT score below the threshold are considered to be eligible.

determined through an analysis of national household survey datasets and are meant to be easily observable and measurable indicators that have some correlation with consumption or income. Usually, the proxies include: demographics; human capital; type of housing; durable goods; and productive assets. Surveys of all households (desired method) are conducted to generate data. Once the survey is undertaken, the data is fed into a computer and the algorithm is applied. Scores are allocated to households which are ranked from the poorest to the richest. A threshold is determined or is agreed upon for eligibility. Households with PMT score below the threshold are considered to be eligible.

But the implementation of PMT model is expensive. In Pakistan, the 2009 survey cost US$60 million. In Indonesia, it cost US$100 million in 2015. In Tanzania, each PMT survey cost US$12 per household implying that for the entire nation, the total cost would be around US$140 million. Kenya's HSNP programme required around US$10 million to survey only 380,000 households, or around US$26 per household. In Bangladesh, it is been costing about $ 80 million (Kidd et al, 2019).

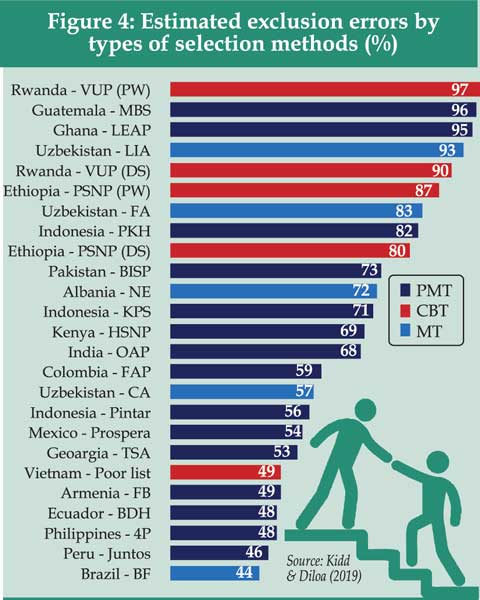

Attaining the intended goals of the social security system (for instance reducing poverty of extreme or poverty among bottom 25 per cent of the population) through adopting one of the seven targeting approaches is not always satisfactory due to inherent identification problem of targeting methods. In a recent study, Kidd et al (2019) assess the targeting efficiency of three targeting methods (such as PMT; community-based testing - CBT; and means testing (MT) of 25 selected social protection schemes of low- and middle-income countries. More specifically, they wanted to 'assess whether is it possible to effectively reach those living in extreme poverty using poverty targeting. accordingly, they examined the targeting effectiveness of those programmes aiming to reach the poorest 25 per cent.

The outcomes (i.e. exclusion errors) of the 25 schemes are provided in figure 4. The report argued that findings are not satisfactory, with coverage under 25 per cent of their target population, 12 have exclusion errors above 70 per cent, 8 have errors above 80 per cent and 5 have errors above 90 per cent. Only six schemes have been able to reach over half their intended recipients.

On the basis of the findings, it is concluded that "overall, the results demonstrate a mass failure of poverty targeting across low- and middle-income countries. In programme after programme, the majority of both the intended recipients and the poorest members of society are excluded. Therefore, if the aim of governments and international agencies is to reach those living in poverty and ensure 'leave no one behind,' the use of poverty targeting will result in failure."

Bangladesh model uses HIES 2018 data. It is an updated version of the 2010 PMT model. From 10 different PMT models, the best model has been selected. It is selected on the basis of key indicators such as under-coverage, leakages and targeting efficiency when a 20 per cent cut off point is considered.

Bangladesh model uses HIES 2018 data. It is an updated version of the 2010 PMT model. From 10 different PMT models, the best model has been selected. It is selected on the basis of key indicators such as under-coverage, leakages and targeting efficiency when a 20 per cent cut off point is considered.

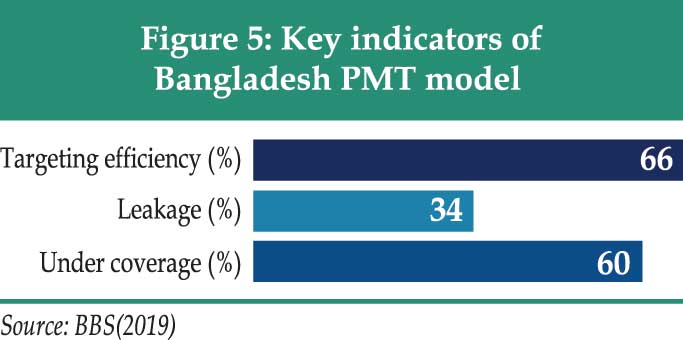

According to the best fit Bangladesh PMT model (2016), under coverage is 60 per cent which means 40 per cent of the poor are left out of the safety net. This  is the theoretical error. If we add 5.0 per cent more implementation error -- the level of exclusion error is close to current exclusion error of 70 per cent. The inclusion error is also not small at 34 per cent. Again, if a 5.0 per cent implementation error is added the inclusion error (i.e. 39 per cent) is close to current exclusion error of 47 per cent.

is the theoretical error. If we add 5.0 per cent more implementation error -- the level of exclusion error is close to current exclusion error of 70 per cent. The inclusion error is also not small at 34 per cent. Again, if a 5.0 per cent implementation error is added the inclusion error (i.e. 39 per cent) is close to current exclusion error of 47 per cent.

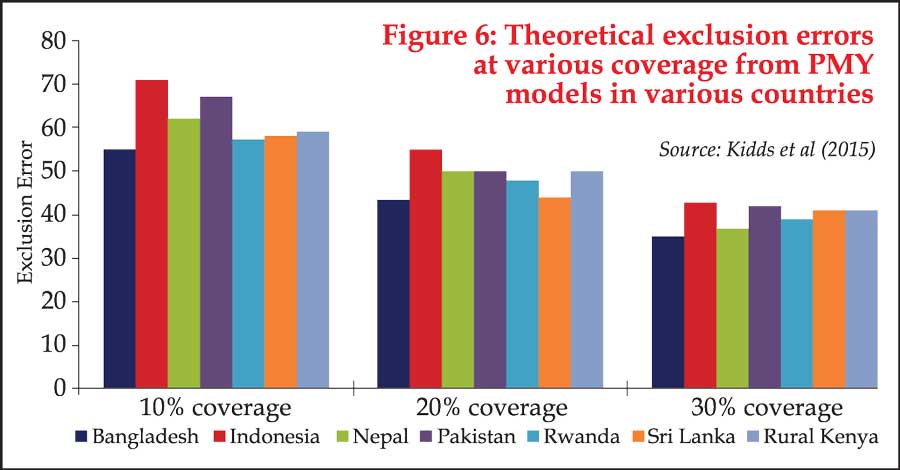

But these results are not surprising. It is well known and accepted that at a lower level of coverage (e.g. 20 per cent), the exclusion and inclusion errors will be high. Exclusion and inclusion errors at lower level of coverage has also reported high theoretical errors for various comparable countries (Please see figure 6).

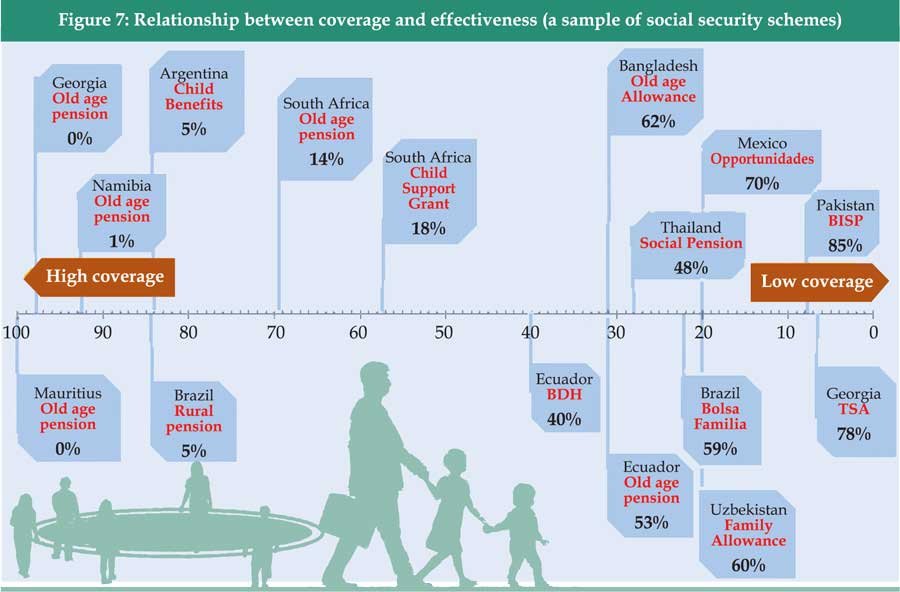

The level of errors comes down with the expanded coverage. It is also important to note that when universal selection on the basis of poverty situation is compared, it is evident that coverage is more important in determining the inclusion of poor people than any particular mechanism for identifying or selecting them (i.e. as discussed above). Figure below illustrates this point by mapping a range of social security schemes in developing countries along a scale indicating the coverage of the intended category of recipients. On the right-hand side of the scale, 0 indicates zero coverage while, on the left, 100 indicates universal coverage. The number within the boxes indicates the proportion of the poorest 20 per cent of the selected category who are excluded from the scheme (with the poorest 20 per cent used as a proxy for the extreme poor).

The level of errors comes down with the expanded coverage. It is also important to note that when universal selection on the basis of poverty situation is compared, it is evident that coverage is more important in determining the inclusion of poor people than any particular mechanism for identifying or selecting them (i.e. as discussed above). Figure below illustrates this point by mapping a range of social security schemes in developing countries along a scale indicating the coverage of the intended category of recipients. On the right-hand side of the scale, 0 indicates zero coverage while, on the left, 100 indicates universal coverage. The number within the boxes indicates the proportion of the poorest 20 per cent of the selected category who are excluded from the scheme (with the poorest 20 per cent used as a proxy for the extreme poor).

It is clear that universal coverage of poor will not be possible using the PMT model. However, following steps may be considered for better coverage of the poor.

* The implementation of the National Household Database will help the authority create a single registry system with important information of potential beneficiaries of different types of public intervention programmes. This will also help establish a comprehensive MIS system for monitoring and evaluation.

* As the above results suggest, adoption of a PMT model with low coverage will not provide a universal coverage of the poor. Evidence also suggested that community targeting is not effective. Given that almost all households in Bangladesh have one child and one elderly member, a universal child grant (100 per cent coverage) and Old Age Allowance (social pension) covering 70 per cent with an inflation indexed transfer amount equivalent to the upper poverty line along with the provision of application for entry into the system and self-exclusion may be adopted. That is, to access these benefits, all households must apply for it. Such a condition will surely discourage well off households and as a result the effective child grant coverage may drop to 70 per cent and elderly allowance coverage to 50 per cent. In this way, a better coverage (near universal) of poor with reasonable transfer amount may be ensured. For all other safety net programmes, a PMT model may be used.

* The approach outlined above should also be supported by a strong grievance system and monitoring mechanism.

In conclusion, we can say that while universal coverage of poor will not be possible by using the PMT model, the condition of applying can result in better coverage of the needy.

Bazlul Haque Khondker is Professor, Department of Economics, Dhaka University and Director, Policy Research Institute of Bangladesh (PRI).

bazlul.khondker@gmail.com

© 2026 - All Rights with The Financial Express